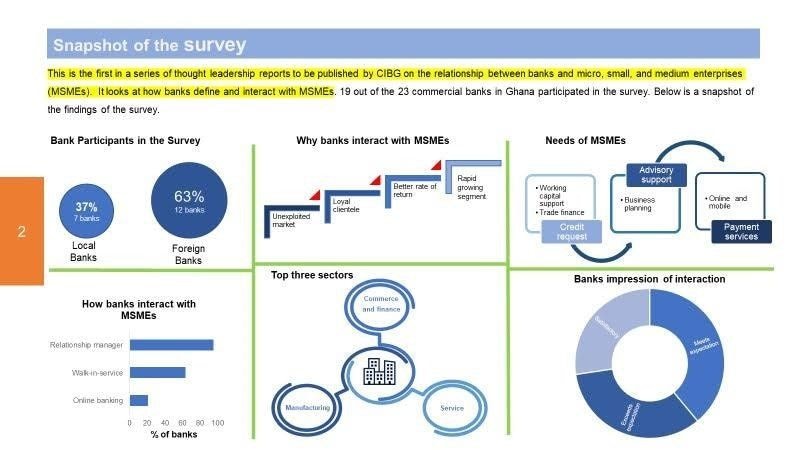

Banks eager to fund MSMEs – CIB survey

0 views

Related Coverage: SMEs

Features

From Madina Old Road to the marketing boardroom: This is Dinah Asabea Darko

Long before she became one of Ghana’s applauded marketing professionals, Dinah Asabea Darko was the outspoken child who rarely wanted the day to end.

Africa

Africa’s future depends on moving people, skills and ideas across borders — Dr Ishmael Yamson

Africa’s economic transformation will depend not only on the movement of goods and capital but also on the ability of people, skills and ideas to move freely across borders, Dr Ishmael Yamson, a member of Ghana’s Presidential Advisory Group on the Economy, has said.

Economy

Gov’t to halve fiscal anchor to 0.5% of GDP from 2027

Government will amend the Public Financial Management (Amendment) Act, 2025 (Act 1136) to reduce the statutory primary balance floor from 1.5 percent of Gross Domestic Product (GDP) to 0.5 percent from 2027, Finance Minister Dr. Cassiel Ato Forson told parliament yesterday in the 2026 Mid-Year Fiscal Policy Review.

Business

Private sector credit hits GH¢119.6bn

Credit to the private sector expanded 41.2 percent year-on-year in June 2026 to GH¢119.6billion, one of the fastest paces on record, according to data published by the Bank of Ghana (BoG).

Oil and Gas

US$3.5Bn upstream investment push aims to reverse oil decline

The country has secured more than US$3.5billion of fresh investment commitments from partners in its flagship Jubilee and Offshore Cape Three Points (OCTP) oil fields as government moves to reverse years of declining crude production and restore confidence in the upstream petroleum sector, Finance Minister Dr. Cassiel Ato Forson has said.

Business

AGI urges strategic industrialisation

The Association of Ghana Industries (AGI) has called for a renewed national commitment to strategic industrialisation.

Telecom

MTN positions fibre broadband as backbone of digital economy

MTN Ghana has identified fibre broadband connectivity as a critical infrastructure for accelerating Ghana’s digital transformation, as the telecom operator seeks to expand home internet adoption across the country.

Health

Africa mobilises US$110m for Ebola response as health sovereignty agenda gains momentum

Africa has mobilised approximately US$110 million from domestic sources to support responses to Ebola and other disease outbreaks, marking a significant step towards strengthening the continent's health security and reducing dependence on external funding.

Comment guidelines

Please keep comments respectful. Use plain English for our global readership and avoid using phrasing that could be misinterpreted as offensive. By commenting, you agree to abide by our community guidelines and these terms and conditions. We encourage you to report inappropriate comments.

No comments yet. Be the first to share your thoughts.