Remittances have seen significant digital advances over the past decade, but the industry is still in the midst of a generation-long shift.

If you live in a major city, there’s a good chance that you are starting to see cash use as a thing of the past. The rise of card and mobile wallet-based payments, as well as the rejection of cash during the pandemic, has increasingly seen digital payments take the lead in numerous parts of the world. Many people now go weeks or months without handling cash at all. However, in the world of consumer remittances, the digital payments story is quite different.

For customers sending remittances to friends and family around the world, the range of options is significant for many corridors – the term used to describe the pair of countries a payment is initiated between. Customers can now pay money directly into a recipient’s bank account; their preferred mobile wallet; or even their card, using just the 16-digit number. They can do this with a variety of app and web-based services, as well as traditional outlets such as retail stores. And they have similarly broad options to initiate payments, which in many cases will be delivered near-instantly or within a few hours.

Much of this modern payments experience can feel immensely futuristic, but it sits alongside pay-in and pay-out methods that are decades-old. Many customers send or receive remittances using cash, checks or money orders – or even send money home by handing physical cash to a third party who will take it to the recipient when they travel to the destination country. On the same corridor, you can have remittances sent with a digital ease and speed that would have seemed unthinkable a few years ago, while others involve days or weeks-long paper-based processes or even cash carried across borders in suitcases.

This is happening on an enormous scale. According to market sizing data from my own company FXC Intelligence, total consumer remittances globally reached US$848 billion in 2022, and are expected to pass US$1 trillion by 2025. The size of the market if you include larger consumer transfers, such as overseas house purchases, is even bigger than this.

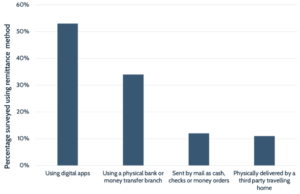

However, according to research published today by VisaV, only slightly over half of those are likely to be sent digitally. The report, which is based on a survey of over 14,000 consumers across 10 countries around the world, found that 53percent of consumers are using digital means, compared to 34percent using a physical bank or money transfer branch. 12percent, meanwhile, are sending cash, checks or money orders in the post, while 11percent are relying on friends or acquaintances to take money home with them when they travel.

The opportunity for increased digitization is therefore immense for the remittance industry, but there is a very long road ahead.

“We are just halfway in the digitization journey, and the opportunity for digital channels is still pretty large,” Ruben Salazar, Global Head of Visa Direct, tells me in an interview.

“The intention is there, the capabilities are there and there is still significant headroom for us to continue to push for innovation, for digital, as an industry.”

Popularity of different remittance methods

The digital versus retail split

Much of the past digital adoption in remittances has focused on low-hanging fruit, and those with more developed digital payments systems have far more readily been converted into digital remittance customers. In North America, for example, Visa found 60-70percent of customers had used an app-based payment method, while in Singapore 61percent of survey respondents had used digital methods to send remittances.

For some players, the shift to digital is accelerating, with Remitly, which offers digital-only services on the send side, reporting seeing this trend unfold.

“It varies depending on the country and the corridor, but overall, that macro theme of shifting to digital is definitely occurring at an even more rapid pace,” said Matt Oppenheimer, CEO, Remitly, when I spoke to him earlier this month.

“People forget that a huge percentage of remittances are originated via physical cash locations, and that is digitizing first. On the receive side, it varies depending on the market.”

However, others report that customers who are using retail outlets are largely not changing their sending habits. “Most consumers that are retail are only retail. Most consumers that are digital are only digital. There’s an overlap, but a very small one,” said Bob Lisy, CEO, Intermex, when I spoke to him in November.

Critically, much of the digital-physical divide in remittances is generational, even when it comes to receive, which remains more cash-based for many corridors.

“If you have an embedded behavior to go into the branch, and that’s your preferred way of receiving that transaction, you will have a larger resistance to change,” says Salazar.

“But as a new generation of migrant workers and receivers emerge, the utilization of digital channels is more logical because they have grown using mobile wallets, debit cards or bank accounts in a different way. Their relationship to money is different than previous generations.”

Drivers and challenges of the digital switch

While there is often a base assumption in fintech that digital equals better, it is worth considering the genuine benefits that switching to digital can bring for customers.

“Security, transparency and convenience are the three main leading adoption factors,” says Salazar, adding that security is “becoming the leading factor.”

“They trust the payment method they are using. The debit cards they use to fund the transaction, either Visa, MastercardMA or American ExpressAXP, are a known activity for them. There is a standard of security and quality expected from this type of card-based network.”

This is echoed by other players in the space.

“The trust, the peace of mind and the reliability of our service is what our customers care about the most and what is often lacking with a lot of remittance companies out there,” said Oppenheimer.

Beyond this, there is a greater level of certainty about the precise amount that the recipient will receive than with some physical methods, while the simplicity of using a phone to initiate a transaction whenever and wherever a customer wants is also key.

However, cost remains a significant driver, both for consumers and the providers of remittance services.

“It’s very expensive to manage cash,” says Salazar, pointing to the infrastructure and security required to support the service. “The cost to serve that transaction is more efficient when you are in a digital environment.”

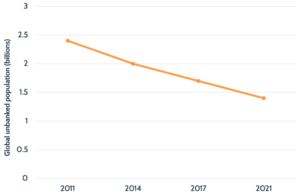

However, while there are reasons to switch to digital, there are also barriers to access, not least among those who have little or no access to formal financial services. According to the World Bank, 1.4 billion people – 18percent of the global population – were unbanked in 2021, and many live in some of the largest recipient countries for remittances.

“It’s not like you’re going to be converting people that don’t have bank accounts to digital. They’re going to be at retail,” said Lisy.

However, there are moves to find solutions to this challenge, including the provision of digital wallets or virtual cards, which can be accessed on smartphones.

“The consumer may not have a bank account, they may not have a debit card but they may have a digital wallet where the transaction can land,” says Salazar.

Global unbanked population over time

Partnership strategies among remittance players

As the industry continues to grapple with this shift, it is increasingly making use of partnerships to broaden its offerings and better serve customers. This is seeing players that in other corridors may be rivals working together in key markets. Among those taking this approach, Visa Direct is particularly known for its partnership-led strategy.

“Our focus is to become an enabler, partner and collaborator with the industry to accelerate this migration to digital, especially in card-based transactions where we have a significant installed capacity around the world,” says Salazar.

“Our aspiration is that all players will see us as an operating system and they don’t need to duplicate efforts in creating additional networks or additional capabilities that we can offer to the market.”

He argues that this approach will ultimately help to streamline cross-border payments and reduce friction for customers – as opposed to multi-infrastructure scenarios where “seven to ten different parties” are involved in a transaction.

“If all players build their own infrastructure and their own connectivity, we will reach a point of diminishing returns or we will collectively destroy value and the consumer will not be winning,” he explains.

“We are a network, we provide technology support and we provide connectivity and that’s the play we want to play. And over time we believe we can become a formidable alternative for cross-border, offering the network and the platform to our partners.”

A Generational Shift

The shift to digital has been many years in the making, but for many it will be a generation before it is complete.

“We don’t expect this to happen in the next three years. It will take some time to accelerate this adoption and education is key; transparency is key,” says Salazar.

This will take time, but industry consensus for the most part is that the shift is ultimately inevitable.

“There’s obviously a shift happening to digital and specifically digital origination. The industry continues to be at a tipping point, with more and more customers shifting to digital devices to send money back home – that’s the biggest macro shift,” said Oppenheimer.

However, as time goes on, the industry will need to build on its efforts to reach more non-digital customers. Some of this will simply be a matter of infrastructure, while improvements in user interface and user experience will also help lower the barrier of entry for some customers.

Nevertheless, the rise of digital-only players such as Remitly and Wise speaks to the ongoing potential of digital, and is reflected in the increasingly digital strategies of established remittance giants such as Western Union and MoneyGram.

“Having new players who are end-to-end digital and having legacy players reinventing themselves as digital platforms is helping to accelerate the transformation,” says Salazar.

“But it will take time. Collectively the industry has just started its journey in digital.”

Disclosure: Both Visa and Remitly are clients of the author’s company, FXC Intelligence.

>>>the writer is Founder and CEO of FXC Intelligence, a financial data company specializing in the cross-border payments, cards and ecommerce industries. Daniel is a leading influencer in the cross-border payments space globally. He is frequently invited to speak at industry conferences and provide insights and data on the sector. His weekly industry newsletter is the most widely read in the international payments market.