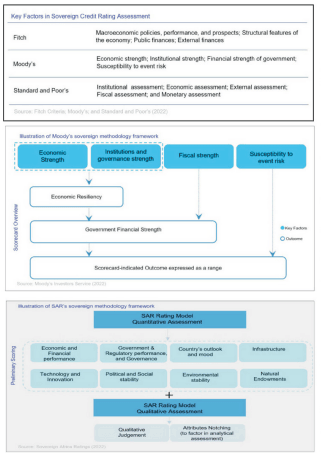

Africa and the credit rating biases – what is the way forward?

Juliet Etefe

0 views

Related Coverage: Features

Features

The equilibrium nobody wants in the civil service: Political survival, professional neutrality, and the coordination problem

There is a pattern familiar to almost every Ghanaian who has worked in or around government.

Features

IPO governance and the new GSE disclosure landscape: What boards and sponsors must get right before, during, and after a public listing in Ghana

Ghana's Capital Markets at an inflection point After seven years of primary market inactivity following MTN Ghana's 2018 listing,

Features

Ghana just won the AI infrastructure lottery. Now comes the harder part

Seven days in July told us almost everything we need to know about where global AI is heading and where Ghana still has work to do.

Features

Africa’s savings paradox: we save, but are we building wealth?

A market woman puts a little money into a susu every week. A salaried worker keeps part of each month’s salary in a mobile-money wallet.

Features

The forgotten sons: 'ewiase tan barimah': When empowerment becomes exclusion

The Ghanaian conscience has long been anchored on the profound principle of communal fairness - the idea that “Obaatan” (the nurturing mother) and the village lift every child together.

Features

Restoring confidence: Building a financial sector that customers can trust at every stage of their journey

Ghana’s financial sector faces a fraud challenge that touches every phase of the customer lifecycle.

Features

Think your business is too small to be targeted? Think again

The dangerous misconception Many small business owners operate under a dangerous misconception: cyberattacks target large corporations, government agencies, and high profile organizations.

Features

Beyond Degrees: Are we producing graduates or building a future-ready workforce?

Every year, thousands of Ghanaian students graduate from universities with dreams of building successful careers and contributing to national development.

Comment guidelines

Please keep comments respectful. Use plain English for our global readership and avoid using phrasing that could be misinterpreted as offensive. By commenting, you agree to abide by our community guidelines and these terms and conditions. We encourage you to report inappropriate comments.

No comments yet. Be the first to share your thoughts.