The market is still struggling with a great deal of uncertainty surrounding probable restructuring, as well as elevated price pressures, a weaker cedi and tighter liquidity. The outcome of the debt sustainability analysis and a choice about future debt treatment have to a significant extent put investors on edge.

As illustrated in investors’ demand for Treasury bills, auctions have been undersubscribed for the second time in 18 weeks amid tightened cedi liquidity conditions on the money market, while the secondary market remains net-offered across the yield curve.

On the money market – involving trading in short-term debt securities such as 91-day T-bills – liquidity constraints, as well as growing concerns of potential domestic debt restructuring, led to a 10.43 percent under-subscription of the sale. Total bids of approximately GH¢974million were tendered and allotted between the 91 to 364-day tenors, against a target of about GH¢1.09billion.

Accordingly, money market yields climbed higher at the latest auction – largely influenced by red-hot inflation, which stands at 37.2 percent for September 2022. The average yield on 91-day bills was 31.39 percent (+43 basis points (bps) week-on-week (w/w)). Similarly, the 182-day and the 364-day bills cleared around 32.24 percent (+30bpsw/w) and 32.07 percent (+52bps), respectively.

Market-watcher Constant Capital, in its weekly monitoring of the market, anticipates a further upside to yields at the next auction on Friday, October 21, 2022 in order to induce demand. “We think bids around the upper 31 percent levels will be successful for the 91-day tenor and mid-32 percent for the 182-day bills.”

The Treasury is facing a sizeable refinancing obligation in the week ahead, with an aggregate face value worth GH¢1.45billion maturing on October 24, 2022; thus, targetting a gross issuance of GH¢1.56billion across the 91-day and 182-day bills to refinance upcoming maturities.

An analyst with GCB Capital, Courage Boti, in his analysis also stated that with the tightening cedi liquidity levels amid the prevailing market uncertainty and relentless inflationary run, demand for T-bills could be depressed… sustaining the upward pressure on yields.

“The market remains uncertain, with investors on edge awaiting the Debt Sustainability Report’s outcome and a decision on a potential debt treatment. However, we believe notes and bonds with residual maturities of less than a year potentially hold value as the deep discounts on offer could compensate for any potential haircut,” Mr. Boti said.

Secondary Market

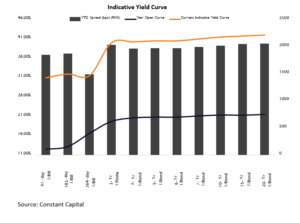

Yields increased all across the local currency (LCY) curve, as the secondary market continued to be heavily net-offered.

“The cumulative face value traded for last week increased by about a quarter from the previous week – signalling a strengthening of the selling pressure as demand for T-bills could be depressed, sustaining the upward pressure on yields,” Constant Capital observed.

Commenting on trading dynamics at play on the Ghana fixed-income market (GFIM), Mr. Boti with GCB Capital noted that, generally, the market is net-offered across the curve; with the selling interest emanating from domestic and offshore investors.

The aggregate volume of GoG bonds traded on the GFIM increased to GH¢2.76billion. Investors traded an aggregate volume of 2.43 billion on the secondary bonds market last week, 13.43 percent w/w.

He indicated that the medium-term maturities are now offered firmly above the 40 percent level, with the 2022 and early 2023 tenors trading a touch below 40 percent at close of the week.

“The 2022-2027 tenors accounted for about 55 percent of aggregate turnover, with the remaining 45 percent spread across the mid portions and back end of the LCY curve.”