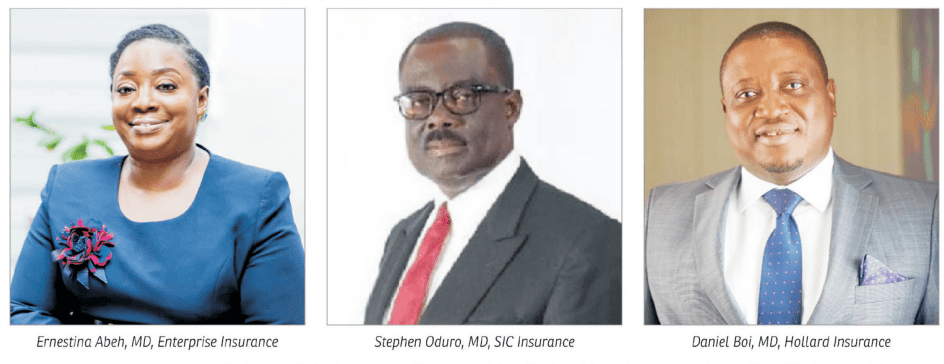

#2022BFTInsuranceSurvey: the insurers who manage the most risks

0 views

Topics in this article

InsuranceNon-Life Insurance Companies#2022BFTInsuranceSurvey

Related Coverage: Insurance

Features

Konahene enstools Dr Maxwell Ampong as inaugural Aboafuohene of Kona

The Konahene of Kona, Nana Konadu Yiadom Kumanin IV, has enstooled accomplished entrepreneur and investment executive Dr Maxwell Ampong as the inaugural Aboafuohene of the Traditional Council of Kona, within the Dumankwa-Nifa Kyidom Division under Otumfuo Osei Tutu II.

Breaking News

Mahama directs GH¢2 cut in diesel regulatory margin to ease fuel costs

President John Dramani Mahama has directed a temporary GH¢2 reduction in the regulatory margin on diesel as part of government's efforts to cushion consumers against rising fuel prices and ease inflationary pressures.

Editorial

Stronger staples domestic production needed to meet growing demand

The latest Annual International Merchandise Trade Statistics Report by Ghana Statistical Service shows that more than GH¢36.5billion went on importing food products in 2025.

Editorial

Pre-export verification of used cars comes into force soon

Ghana Standards Authority (GSA) has announced October 1 this year (2026) as the commencement date for enforcing new automotive safety and conformity requirements for imported used vehicles.

Oil and Gas

TOR revival shows value of strategic partnerships - President Mahama

President John Dramani Mahama has described the revival of the Tema Oil Refinery (TOR) as evidence that strategic partnerships, strong leadership and effective management can restore struggling state-owned enterprises without direct government funding.

Banking & Finance

Access Bank Partners Points Africa to expand benefits under its Rewards by Access Loyalty Programme

Access Bank (Ghana) Plc has partnered with Points Africa, a mobile-first rewards platform, to enhance the Rewards by Access loyalty programme by expanding the network of locations where customers can earn and redeem loyalty points.

Banking & Finance

CalBank launches "Abakade Promo" to reward customers with cash prizes

CalBank PLC has officially launched the “CalBank Abakade Promo”, a three-month savings promotion designed to reward customers for cultivating a savings habit while giving them the opportunity to win life-changing cash prizes.

Features

HR Frontiers with Senyo M. ADABENG: Being disabled in a typical workplace

For the over two million citizens living with a disability in. Ghana, representing about a significant 8.6 per cent of our population, the pursuit of a dignified livelihood is a daily battle against a system that is often structurally and attitudinally hostile. This statistic does not include non Ghanaians disabled persons living in the country.

Comment guidelines

Please keep comments respectful. Use plain English for our global readership and avoid using phrasing that could be misinterpreted as offensive. By commenting, you agree to abide by our community guidelines and these terms and conditions. We encourage you to report inappropriate comments.

No comments yet. Be the first to share your thoughts.