I refer to the above-mentioned subject published in the Business and Financial Times dated Thursday, May 5, 2022 (p.5) both online and in print, where I made a comprehensive analysis on the performance of the Banking Sector based on the 2021 audited financial statement. In the article, some figures on the profitability and Earnings subsection should have read as Billions (Bn) instead of Millions (Mn) and hence being corrected as below;

Profitability and Earnings (Correction)

To measure the performance of a bank, every manager, shareholder or investor would be interested in profitability indicators since profits are the ultimate goal of banks. The profit a bank makes is also a matter of key interest for managers and investors when making strategic decisions. All strategies designed and the activities implemented are aimed at realising this great goal.

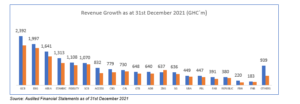

The Banking industry headline revenue for the year ending 2021 grew to GH¢17.43bn (2020: GH¢15.2bn), representing a 14.6% growth year on year. GCB Bank maintained the top position with a revenue of GH¢2.39bn (2020: GH¢1.94bn), with an increased market share of 13.7%. GCB’s performance was up by 23.4% year on year. The second position was closely held by Ecobank, who closed the year at GH¢1.99bn, with marginally declined market share of 11.5% (2020:11.9%). With the exception of Zenith Bank Ghana Limited that declined in year-on-year growth by 13%, thus, from GH¢732m in 2020 to GH¢637m in 2021, the rest of the banks saw an increase in revenue.

Interestingly, the top 6 banks (GCB, Ecobank, Absa Bank, Stanbic, Fidelity and Standard Chartered) crossed the GH¢1m revenue mark and contributed 55% of the overall industry revenue. From a Net Interest Income (NII) and Non-Funded Income (NFI) perspective, while Republic Bank was growing its NII by over 50% to GH¢299m year on year, Stanbic Bank managed to increase transactional fees by 42% to GH¢857m; the highest NFI growth on the market since 2019. It was obvious that while other banks were given waivers and reduction on pricing to clients, some banks increased their volume of activities to drive its fee income.

In view of the ongoing pandemic, the industry’s Profit Before Tax (PBT) increased to GH¢7.42bn (2020: GH¢6.08bn). Despite the various challenges, growth in operating profit remained impressive across the industry, averaging c. 22% (2020: 27%). However, this double-digit growth could not match the 2020 performance when COVID-19 was at its peak. Banks like Zenith and UBA saw a dip in PBT by 28.4% and 2.3%, respectively. Though Ecobank was impressive on its revenue performance, Absa maintained the top position as the most profitable bank, closing the year at GH¢1.06bn (2020: GH¢883m) with a market share of 14.3%. It is important to mention that following the decoupling of Barclays from the Barclays Africa Group Limited’s business few years ago, Financial Analysts were of the view that this move could have impacted on the bottom line. However, the bank continues to demonstrate strong performance both in revenue and balance sheet. This also reaffirms the need to strengthen Regional and Local Banks to stand the test of time.

Ecobank, GCB and Standard Chartered were ranked 2nd 3rd and 4th, respectively. It’s therefore an established fact that while some industries and sectors were struggling to stay afloat amidst the pandemic season, commercial banks were generally profitable.

| Banks | ABSA | ECOBANK | GCB | STANBIC | SCB | |||||

| Key Profitability Ratios | 2021 | 2020 | 2021 | 2020 | 2021 | 2020 | 2021 | 2020 | 2021 | 2020 |

| Return on equity | 30% | 24% | 22% | 22% | 22% | 21% | 21% | 19% | 27% | 33% |

| Return on assets | 4% | 4% | 3% | 3% | 3% | 3% | 3% | 3% | 4% | 6% |

| Return on earning assets | 6% | 5% | 4% | 5% | 4% | 3% | 4% | 4% | 7% | 11% |

| Net Profit Margin (PAT to Revenue) | 42% | 34% | 29% | 30% | 23% | 23% | 31% | 30% | 41% | 47% |

| EVA | 312 | 140 | 139 | 132 | 135 | 91 | 82 | 41 | 165 | 229 |

| NII to total income | 66% | 69% | 75% | 74% | 79% | 77% | 50% | 57% | 60% | 63% |

| NFI to total income | 34% | 31% | 25% | 26% | 21% | 23% | 50% | 43% | 40% | 37% |

| Ave. cost on interest bearing liabilities | 3% | 4% | 1% | 2% | 3% | 3% | 2% | 2% | 2% | 3% |

| Gross yield on ave. earning assets | 12% | 13% | 13% | 15% | 16% | 15% | 9% | 10% | 13% | 18% |

| Net interest spread (NIM) | 9% | 9% | 11% | 13% | 13% | 12% | 7% | 8% | 11% | 15% |

| Earnings per share (GH₵ per share) | 7.7 | 5.24 | 1.8 | 1.69 | 2.1 | 1.66 | n.a. | n.a. | 3.23 | 3.54 |

Source: Audited Financial Statements as of 31st December, 2021

My Sincere apologies to cherished readers, institutions mentioned in the article and anyone who might have used the previous information for any decision-making.

Disclaimer: The views expressed are personal views and doesn’t represent that of the media house or institution the writer works.

Carl Odame-Gyenti, PhD is a Banking, Finance, and Investment professional. Director, Banks & Broker Dealers with an International Bank in Ghana. Contact: [email protected], Cell: +233 200301110