By Kumi Owusu-Ansah

“OFF with their heads” – is the sentence that the Queen of Hearts, the incarnation of monarchical caprice in Alice’s Adventures in Wonderland, adores pronouncing. She might be entertaining.

But the reality, however, is not. Throughout history, absolute rulers have brought misery upon their people and even their families. Their courts are hotbeds of sycophancy, favouritism and corruption. This is the price of arbitrary despotism.

The story of English-speaking people, including the US, at its best, has been one of taming such arbitrary power.

It was a lengthy and hard struggle, from Magna Carter in 1215 to the exile of James II and the declaration of the Bill of Rights in 1689, via the civil war of the early 17th century and execution of Charles I in 1649.

Those who condemned the dethroned monarch to execution rightly found him guilty of seeking “an unlimited and tyrannical power to rule according to his will”.

The Declaration of Independence and ratification of the US Constitution were further steps in this war on absolutism. So, too, was the US civil war, which established the principle that nobody should be allowed to hold absolute power over another person.

What is happening today in the US is of historic and also global significance, because it is about whether constraints on the arbitrary exercise of power will endure. Nobody with any knowledge of the catastrophes of the 20th century can be unaware of the significance of this issue.

Replacing tyranny with the rule of law, the role of courts in determining that law and that of the legislature in making it serves both moral and practical goals. Only in such a state can people feel safe against despotism.

A government that ignores the constraints is a tyranny. As commentator Andrew Sulivan observes: “America is about legal authority. Trump is about raw power. America was founded on a faith in reason. Trump embraces his own instinct alone.” We are witnessing a long-planned assault on the Republic itself.

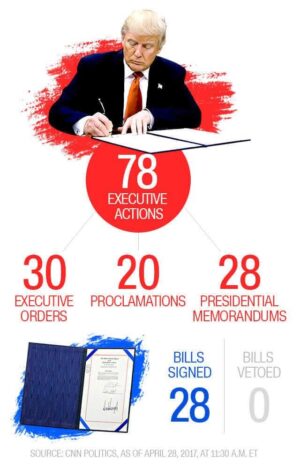

Trump’s first 100 days back in the White House are an unravelled example of how rapidly a manic leader who surrounds himself with fools and fanatics can recklessly unravel a mighty country’s greatest strength.

His acts so far have given us an object lesson in the economic costs. Not only trade wars Trump has launched are signs of his folly but his recent soprano-like attacks on Jerome Powell, the chairman of the US central bank, the Federal Reserve, are a demonstration of the dangers.

The US Federal Reserve was established for one purpose only: to manage, look after and stabilize the Treasury bond market. The bond market is the foundation of the current economic and financial system.

If anything goes wrong – the recent yields spike, for instance – it’s the Fed’s duty to intervene. It’s rare to see an open conflict between a president and the US central bank, but Trump has gone hard on its chairman.

So what’s behind this conflict? Trump’s Treasury Secretary, Scott Bessent, made it clear months ago that keeping bond yields low – not boosting the stock market – is the top priority of the administration. This stems from the fact that, in the next four years, the Trump administration will need to refinance around $28 trillion of maturing debt.

Currently, the monetary base – the core money the US has, both in circulation plus commercial bank reserves held at the Fed – is $6 trillion, but there is $100 trillion of debt denominated in dollars.

This includes $36 trillion US government debt, $50 trillion in U.S. private debt and $13 trillion in the Eurodollar market. Every president before Trump refinanced in a falling rate environment. Trump is the only president in 40 years who must roll over debt in a rising environment.

To achieve this, the administration must impose heavy tariffs, crash the stock market, push the economy into recession and enforce the Fed to cut rates – lowering interest rates across the board.

Yes, the market dropped nearly 20 per cent, but bond yield went up – a rare event. But the Fed didn’t cut rates or respond to the correction. Adding to the challenge, China – America’s largest trading partner – ignored Trump’s tariff pressure, making markets even more volatile.

The president needed a stable market to win leverage over China and strike a deal. The reality is, Trump lacks the cards – but Powell holds them. As the top figure in the financial world, Powell could cut rates, ease money flow, lift asset prices and stabilize the bond market.

But Powell, who is the person ultimately responsible for managing and monitoring the US dollar – and by extension, the global financial system, had refused to cut the Fed rate – the short-term base rate set by the Fed on which all other lending rates are built.

The Fed chair has maintained that the Fed is independent. Powell, who intends to server his full term as chair of the Fed, which runs until May 2026, has said the US central bank’s independence to set interest rates as it fit was “a matter of law”. Trump was ‘irked’ by this.

Trump’s claim, On Thursday 17th April, that he has the right to fire Jay Powell has thrust a precedent that protected independent government agencies for the past nine decades into the spotlight. The president attacked the Fed chair, saying “he’s always too late, a little slow. And I’m not happy with him.” When asked by a reporter in the Oval Office whether he would sack the US top central banker, Trump said: “If I want him out, he’ll be out real fast, believe me.”

Trump’s offensive has left investors and economists focused on a case now winding its way through the US courts, which involves his earlier firing of board members at another two independent agencies.

The two officials are far lower profile than Powell, but they were protected by the same 1935 Supreme Court precedent known as Humphrey’s Executor. Powell said on Wednesday that the Fed was “monitoring” the case, which centres on Trump’s dismissal of Gwynne Wilcox of the National Labour Relations Board and Cathy Harris, Merit Systems Protection Board chair, “carefully”.

Beside the tariffs-on, tariffs-off chaos in the White House, Trump is also draining the credibility of his country’s currency. The mighty US dollar fell 5.44 per cent after he expressed his desire to fire the “Dollar Master.”

The DXY Index, which simply measures the strength of the US dollar against six major currencies, also fell to 98 from a high of 104 – a 5.4 per cent decline. The higher the index value, the stronger the dollar becomes – and the more it can buy from the rest of the world. When the index value is lower, the opposite is true.

It’s very unusual for a president to pressure the chairman of the Federal Reserve to cut rates. But the huge pile of debt is giving Trump sleepless nights. When government debt becomes too high, conventional monetary policy stops working.

At that point, suppressing interest rates becomes the only path forward. In simple terms, Rate Suppression means keeping borrowing rates low. If borrowing stay low, then the government can pay less interest and can afford to take on more debt due to the reduced cost of borrowing. So cutting rates is the first step in rate suppression, and yield curve control (YCC) is the final step.

According to Trump, energy prices are low, most consumer goods – including egg prices – are low, and inflation is under control. Yet, the Fed isn’t cutting rates. For that matter, Trump therefore thinks, Powell must go.

But there’s a problem that the president failed to understand. Money is actually a network. It has value because the users of the monetary network believe in it. When people see that someone is trying to manipulate the network, they begin to withdraw from it. And when users start leaving the network, the value of the money collapses. This is what’s happening to the Dollar Value Index since January.

First, is Trump’s “America first” doctrine and his direct intervention in the economy through tariffs policy. Then his ad hominem attacks on the Fed chair – these two moves are alarming the users of the dollar network.

His quest to sack the Fed chair will also test a Supreme Court decision, Humphrey’s Executor vs United States, made 90 years ago, which saw the top US court rule in favour of William Humphrey, a formal head of the Federal Trade Commission, over President Franklin D Roosevelt’s decision to remove him in 1933 due to New Deal Policy.

When Humphrey died, his executor pursued the case to recoup the wages due to his estate, with the Supreme Court deciding that Roosevelt had acted illegally by firing the commissioner without “cause” – a term widely interpreted to cover illegal activities or gross incompetence. The ruling has allowed independent agencies – including the Federal Reserve – to deflect political pressure when making policy decisions.

As the weeks of Trump-induced turmoil rack up, users of the dollar are shifting to hard assets like gold. That’s why the US dollar is collapsing and gold is rising. Always remember: Facebook or Myspace weren’t the first social networks in the world.

Gold was the first global social network – people from around the world used it to save and make payments. Since money is truly a network and its value comes from its users, you must never force or manipulate them. If you do, people will leave that monetary network and migrate to a newer, more transparent one.

In the 1970s, Congress unwisely granted the president the power to impose taxes at will, in response to an “emergency” however imaginary. This is classic despotism. Now, unsurprisingly, Trump is exploiting this power to create chaos. Nobody can sensibly believe this will reindustrialise the US. It will rather paralyse business, raise prices and slow the economy – it will lacerate the US more grievously than it will hurt either China or Europe.

Avoiding such chaos was one of the benefits of ending arbitrary power. By the end of the 17th century, the British state became able to borrow vast sums long term and cheaply. That was the fruit of trust. It was one of the foundations of the flourishing of finance in the 18th and 19th centuries. That in turn was a powerful stimulus to the industrial revolution and subsequent rise in prosperity.

The way Trump is operating his trade war raises even bigger concerns than the economics of protectionism itself. Yes, tariffs are bad policy instruments: they impose a strong home-market bias on production of tradeable goods and high taxation – indirect (via appreciation of the real exchange rate) and direct (via higher prices of inputs) – on exports; forgetting that America has only 4 per cent of the world’s population but consumes 25 per cent of global production.

As Martin Wolf noted last June, “Biden may be old. But trump is crazy, and, alas, he is not amusingly crazy: he is dangerously crazy. Trump’s instincts are also those of a dictator.”

Since this tariffs craze was announced on April 2, the reactions from nations around the world have been one of dissentient. Canada’s Mark Carney has picked up the gauntlet after his election victory.

Britain’s Kier Starmer prefers to look the other way, but the UK premier must bring a long spoon when he sups with Trump on his second state visit to Britain.

Japan and South Korea lead the queue to strike a bilateral deal. Atlanticist Germany declares Europe must go it alone. As much as America’s old friends are appalled by Donald Trump’s trashing of the liberal international order, they differ on how best to respond.

We should beware of taking sides – the pugilists and pacifists both have a point. But kudos generally goes to those willing to stand up to “the bully”.