The Naira depreciated against the dollar, sliding to 741 from 731 at last week’s close as FX demand increased and the central bank allowed old 500- and 1000-Naira notes to recirculate. Nigeria’s annual inflation edged higher in February, with prices rising 21.91% compared to 21.82% a month earlier. That prompted the central bank to raise interest rates by 50bps to 18%. The cash scarcity in recent weeks forced Nigerians to turn to e-payment channels, where transactions in February jumped 121.6% compared to a year earlier. We expect the Naira to continue weakening against the dollar in the near term as FX demand gathers steam.

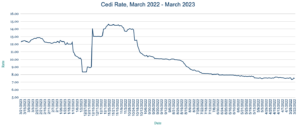

Cedi climbs as lower oil price eases dollar demand

The Cedi gained against the dollar, climbing to 12.25 from 12.41 at last week’s close as FX demand eased amid a decline in oil prices. Ghanaian Finance Minister Ken Ofori-Atta said that talks are continuing with China about restructuring its debt following a successful domestic debt exchange programme. China is Ghana’s biggest bilateral lender, with about $1.7bn in loans outstanding. Ghana needs to reach a deal with all its creditors to unlock a $3bn bailout from the IMF. We expect the Cedi to continue trading around current levels in the short term, absent further progress in the restructuring talks.

Rand edges towards 17 handle amid Fed pause signal

The Rand strengthened against the dollar, trading at 18.15 from 18.40 at last week’s close, after the US Federal Reserve signaled a pause in interest rate hikes to allow the banking system to recover. South Africa had its first full day in 141 days without a rotational power cut this week. An opposition-led march caused little disruption after the government deployed the army to avoid a repeat of the unrest that erupted in July 2021 protests. We expect the Rand to continue edging towards the 18 level, potentially trading with a 17 handle if recent positive international momentum is maintained.

Egypt Pound weakens as imports drive dollar shortage

The Pound declined against the dollar, trading at 30.89 from 30.48 at last week’s close. Egypt agreed to a new framework with the World Bank this week that will enable access to as much as $7bn in financing between now and 2027 to support economic reforms, including privatisation, job growth, and the development of sustainable projects. The Suez Canal Authority reported a 40% increase in first-quarter revenue compared with the same period a year ago due to increased transit rates and shipping traffic, providing much-needed FX inflows. Overall, we expect the Pound to continue weakening in the short-to-medium term as the economy remains largely reliant on imports and faces a net dollar shortage.

Kenyan Shilling hits new low after 5% decline this year

The Shilling slumped to a fresh low against the dollar, trading at 130.80/131.00 from 127.10/127.30 at last week’s close due to sustained FX demand from energy importers and manufacturers. The Shilling has lost more than 5% of its value against the dollar since the start of this year. Kenya held its first meeting with the UK as part of a bilateral Economic Partnership Agreement signed in 2021. The agreement saves Kenyan businesses KES1.5bn a year in duties on popular exports such as cut flowers and green beans. We expect the Shilling to continue weakening towards month-end as importers close transactions, with support from central bank FX reserves dwindling at $6.56bn, sufficient for only 3.66 months of import cover.

Ugandan Shilling under pressure from imports

The Shilling weakened against the dollar, trading at 3763 from 3733 at last week’s close, adding to losses of more than 4% over the past year. Imports have been rising, with Uganda fulfilling less than 30% of domestic demand for oilseeds for cooking, despite efforts to increase the production of palm oil, including the Kalangala project. Dollar demand for imports will continue to weigh on the Shilling in the near term.

Inflows steady Tanzania Shilling amid Marburg virus outbreak

The Shilling advanced from a four-year low against the dollar, strengthening to 2338 from a close last week at 2341, the weakest level since March 2019. Tanzania confirmed its first deaths from the deadly and highly virulent Marburg virus. Public health authorities are working with the World Health Organization to limit the spread of the virus, which has so far claimed five lives in the country. Investment into Tanzania has grown to $8.64bn from $3.16bn over the past two years, according to the Tanzania Investment Centre. That investor confidence should help support the Shilling from any dramatic declines as markets react to the Marburg outbreak. While we expect the currency will slip back to the 2341 level, it is unlikely to weaken beyond 2343.

West African banks urged to ensure capital cushions

The West African central bank warned commercial banks in the region to be prudent about dividend distributions for the 2022 financial year, given the recent weakness in the global banking system. It encouraged banks to ensure mandatory regulatory capital levels that have been in place since the start of the year. The call to scale back dividends is likely to impact the share prices of listed banks.

Bank of Central African States FX reserves jump

The Bank of Central African States said the region’s FX reserves reached XAF7bn at the end of last year, up from XAF4.6bn at the end of 2021. The reserves, sufficient for 4½ months of import cover, increased due to regulations that force oil and mining companies to retrocede 35% of FX earned to the central bank. With the rate expected to gradually increase to 75%, this should help to sustain higher reserve levels in coming years.

Issued by AZA. This Newsletter is produced as a service to our clients. It is prepared by our dealing professionals and is based on their understanding and interpretation of market events. AZA cannot be held responsible for any losses of whatever nature sustained as a result of action taken based on comments contained in this publication.

For more information, high-resolution charts or interviews, please contact:

Gavin Serkin

[email protected]

+44 20 3478 9710