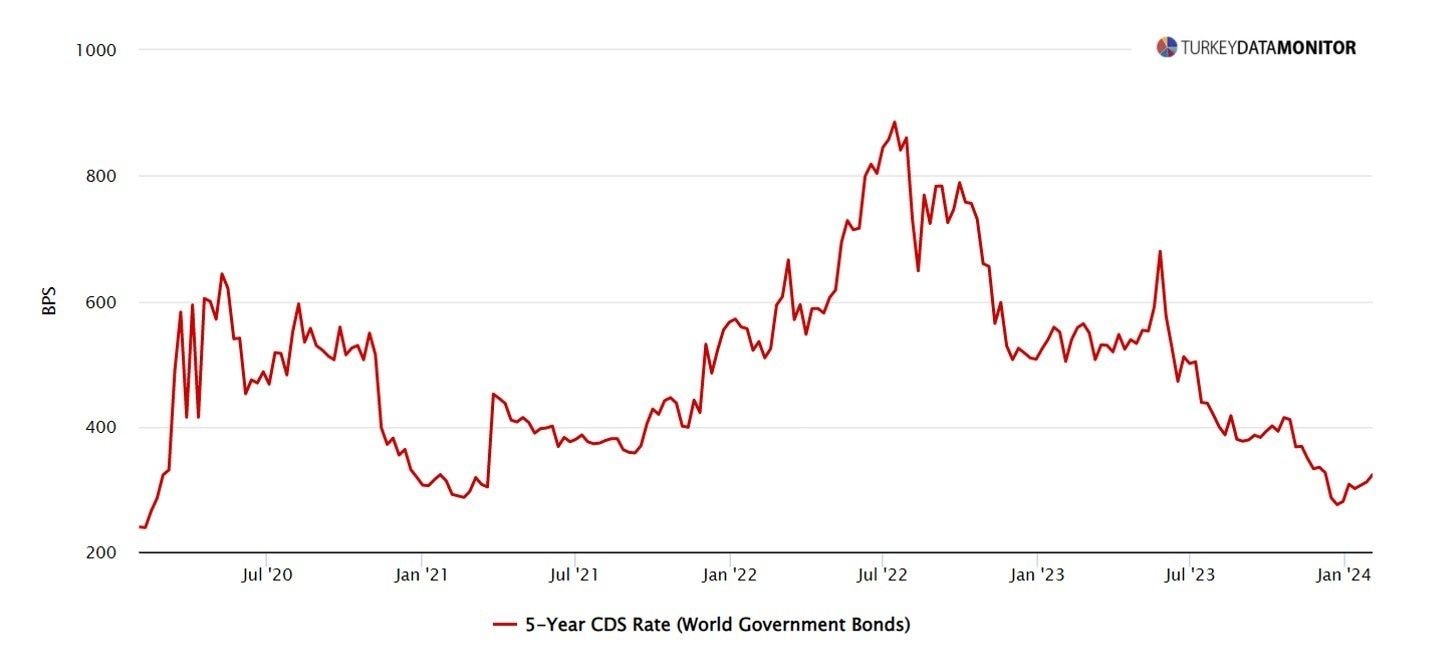

Will Turkey remain committed to economic reform?

0 views

Topics in this article

Will Turkey remain committed to economic reform?

Related Coverage: Editors' picks

Features

Is Wontumi a Political Prisoner? Why Ghana's Justice System and Its Critics Are Both Right—and Wrong

The High Court's 20-year sentence against NPP Chairman Wontumi exposes a fundamental tension in Ghana's rule of law: the difference between judicial independence and democratic accountability. The conviction rests on solid legal grounds. So does the NPP's complaint.

Transport

GSA sets October 1 for enforcement of new used vehicle import standards

The Ghana Standards Authority (GSA) has announced October 1 2026, as the commencement of enforcement for the nation’s new automotive safety and conformity requirements for imported used vehicles.

Top Headlines

VALCO not for sale, gov't seeks strategic investor - Lands Minister

The government has no plans to sell the Volta Aluminium Company (VALCO) but is instead seeking a strategic investor to inject more than US$700 million needed to revive the state-owned aluminium smelter, the Minister for Lands and Natural Resources, Emmanuel Armah-Kofi Buah, has said.

News

Hubtel leadership visit Amazon's Global HQ to deepen data, AI collaboration

Hubtel's full Board of Directors and executive leadership spent two days at the Amazon Web Services (AWS) Executive Briefing Center in Seattle on 9 and 10 July,

Features

The choice for change: Mundubile’s vision for a united and renewed Zambia

As the 13 August election approaches, Zambia must decide which leadership approach can translate economic reform into jobs, lower living costs, reliable electricity, stronger institutions and renewed national unity.

Trade

Trade surplus triples to GH¢148bn on gold export boom

The country’s merchandise trade surplus more than tripled to a record GH¢148.3 billion in 2025 as export earnings surged on the back of strong performances in gold, cocoa and petroleum products, according to the Ghana Statistical Service's (GSS) 2025 Annual International Merchandise Trade Statistics Report.

Economy

Economy insulated, but exposed to gold price swings – Fitch

Ghana’s economy has largely recovered and is expected to maintain its growth momentum, with strong gold exports and improving fiscal management shielding it from external shocks

News

GIPA targets middle belt with US$383.65m investment drive

The Ghana Investment Promotion Authority (GIPA) has launched a major regional investment roadshow across Bono, Bono East and Ahafo as it seeks to unlock fresh investment opportunities and strengthen the pipeline of bankable projects in the country’s middle belt.

Comment guidelines

Please keep comments respectful. Use plain English for our global readership and avoid using phrasing that could be misinterpreted as offensive. By commenting, you agree to abide by our community guidelines and these terms and conditions. We encourage you to report inappropriate comments.

No comments yet. Be the first to share your thoughts.