Nigeria: Global economic contractions affect Nigerian exporters.

Ghana: Inflation eases in Ghana in April.

South Africa: Weaker rand as electricity cuts continue.

Egypt: Egypt’s inflation rate eases.

Kenya: Kenya to receive financing from IMF after review.

Uganda: The Stanbic Bank Uganda PMI rose in April.

Tanzania: Major exports move to USD 758.4 million in March year-on-year.

XOF Region: Ivory Coast, Mali, Benin and Togo raised XOF 135 billion on the securities market.

XAF Region: Cameroon will pay XAF 14.6 billion on its 2022 bond.

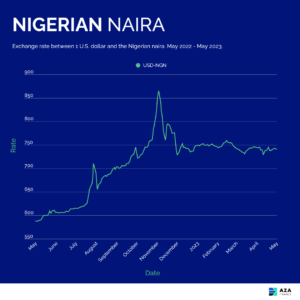

Nigerian Naira (₦)

Compiled by Ikenga Kalu

The Nigeria naira traded at 745 USD/NGN levels this week slightly weaker at 740 USD/NGN compared to last week’s trading session in the open market. On the importers and exporters window, foreign exchange inflows dropped to a two-year low by 58.9% in the month of April compared to March at $1.49 billion U.S. dollars. With the global economy experiencing contractions, the International Monetary Fund signaled that Nigeria should expect a reduction in foreign loans with borrowing costs, high interest rates, and a surge in dollar price continuing to put strain on the country’s economy as well as its counterparts in Africa. With supply of forex not meeting demand, we project sustained pressure on the currency.

Further reading:

Abokifx.com – Foreign Loans Will Shrink, IMF Warns Nigeria – PUNCH

Abokifx.com – Forex Inflow On Investors’ & Exporters’ Window Drops To 2-Year Low – LEADERSHIP

Ghanaian Cedi (GH¢)

Compiled by Murega Mungai

The Ghanaian cedi traded at 11.80 against the U.S. dollar at close of last week to a slightly stronger level of 11.75 USD/GHS this week due to eased demand in the market. Inflation rates improved to 41.20 in the month of April, 2023 compared to 45% in the month of March, 2023 for the 4th consecutive month. The Bank of Ghana has urged commercial banks to cut lending rates to foster more growth in the economy by lending more to the private sector. The country is still in the process of debt restructuring in order to secure the $3 billion U.S. dollars loan from the International Monetary Fund. In the coming days we project the rate to remain fairly unchanged.

Further reading:

Reuters.com — Ghana inflation slows to 41.2% y/y in April: stats office

Myjoyonline.com — Falling inflation: BoG appeals to banks to cut lending rates

South African Rand (R)

Compiled by Alex Barmuta

The rand began the new week trading at 18.3570 — marginally stronger against the U.S. dollar in comparison to last week’s close (18.3811).

The 18.00-18.50 USD/ZAR range that has largely stayed intact since 21 February, finally gave way as news that South Africa’s rotational power cuts would remain at elevated levels indefinitely spooked investors, as they weighed the economic implications of this. This means that the rand is currently trading at levels last seen in the height of the COVID-19 pandemic.

From a global perspective, the U.S. dollar index continues to trade in the 100-102 range, indicating that the rand’s break above the 18.50 resistance level is indeed driven by reduced ZAR demand, rather than increased USD demand.

Looking ahead, we can expect the rand to treat the 18.50 and 18.80 areas as support levels. Further moves to the upside (beyond the USD/ZAR 19.00 level) remains a possibility, which would likely be driven by any increase in U.S. dollar demand.

Financial Post – Blackouts Fuel Pandemic-Like Rout in South African Markets

Egyptian Pound (EGP)

Compiled by Mitchell Diedrick

The Egyptian pound opened the new week trading at 30.9552 against the U.S. dollar and above last week’s opening at 30.9000.

Fitch Ratings downgraded Egypt’s sovereign credit rating by one notch to B from B+ and kept a negative outlook. They noted the increase in external financing risks due to high financing needs and tightening of external financing conditions. Moody’s credit rating for Egypt was last set at B3 with a stable outlook while Standard & Poor’s credit rating stands at B with a negative outlook.

The annual urban inflation rate in Egypt eased to 30.6% in April 2023, below market forecasts of 31%. Costs slowed for housing and utilities as well as transport. Consumer prices rose 1.7%, the lowest in seven months, after a 2.7% hike in the previous month. Our forecast is for the Egyptian pound to surpass the 31.00 (USD/EGP) level in the short to medium term.

Further reading:

Bloomberg – Egypt Gets First Fitch Downgrade Since 2013 as Economy Stumbles

The Guardian — Inflation, IMF austerity and grandiose military plans edge more Egyptians into poverty

Kenyan Shilling (KSh)

Compiled by Terry Karanja

The Kenyan shilling dropped this week to the levels of 136.65/85 USD/KES from last week’s 136.20/136.40 USD/KES as a result of increased forex demand from importers in the energy and manufacturing sectors against slower supply of hard currency in the country. Kenya is seeking an agreement to get the Resilience and Sustainability Facility from the International Monetary Fund. IMF staff will visit the country to review and thereafter, the plan is to disburse $300 million U.S. dollars which is to provide long-term financing to cushion economic resilience. This week the shilling is expected to remain stable with the support of interbank trades and the Foreign Exchange Reserves that currently stand at 6,492 million U.S. dollars. A drop from USD 6,508 million in the previous week.

Further reading:

Bloomberg — IMF to Disburse $300 Million to Kenya After Review Completed

Ugandan Shilling (USh)

Compiled by Yadhav Panday

This Wednesday, May 10, the USD/USh traded at 3,712.00, down 0.35% from the previous trading session. The Stanbic Bank Uganda PMI rose to 55.4 in April 2023, up from 53.2 the previous month, indicating the fastest expansion in private sector activity in 14 months amid improving demand conditions. Business activity increased for the ninth month in a row as new orders increased. Additionally, output increased in agriculture, construction, industry, services, and wholesale and retail. Employment increased in April, ending a two-month decline. Furthermore, purchasing activity increased for the sixth time in a row, while inventories continued to rise. In terms of prices, input costs increased further, owing to rising fuel and utility prices, sustained purchase price inflation, and increased staff costs.

Finally, sentiment was generally positive about the outlook for the next 12 months, with hopes for continued output growth. Looking ahead, we expect the U.S. dollar Ugandan shilling to be worth 3,773.10 by the end of this quarter and 3,889.63 in a year.

Further reading:

The Independent – Private sector output in continued expansion as PMI crosses 55.0

Tanzanian Shilling (TSh)

Compiled by Kristin Van Helsdingen

The Tanzanian shilling has been weakening steadily for roughly a month and has hit its weakest level against the U.S. dollar since March 2019, trading at 2,355. Bid and offer rates for USD/TZS are currently at 2,352 and 2,362.

Provisional data released by the Bank of Tanzania indicates that major exports have increased to USD 758.4 million for the year ending in March from USD 697.5 million in the previous year. The main contributing factor to this bump is the increase in prices. However, as the government works with each export industry to overcome hurdles and increase production, exports are expected to increase further in the year ahead.

With little economic data being released from Tanzania this week, we expect the Tanzanian shilling to continue its trend and weaken further against the U.S. dollar in the week ahead. The weakening of the Tanzanian shilling should be steady, and USD/TZS is expected to trade between 2,351 and 2,360.

Further reading:

IPP MEDIA – Cash crop farmers’ earnings gain exports hit 7584mn

West African CFA Franc Region (XOF)

Compiled by Jean Cédric Nando KOUA

Ivory Coast, Mali, Benin and Togo raised XOF 135 billion on the securities market in the week of May 2, 2023.

Investors showed great interest in these operations with an average subscription rate of 157%. Out of an initial amount of XOF 125 billion sought, XOF 196 billion were offered by investors, and it is finally XOF 135 billion that were retained by the states.

The securities market seems to have regained its dynamism after the various increases in the central bank’s key rate, thus favoring the states, which can continue to finance development.

Further reading:

Sika finance — UMOA-Titres / Week of May 2: A surplus of 71 billion FCFA proposed to the States

Central African CFA Franc Region (XAF)

Compiled by Jean Cédric Nando KOUA

Cameroon has announced that it will pay XAF 14.6 billion on the “ECMR 6.25% NET 2022-2029” bond. This amount consists solely of interest payments, with principal repayments scheduled to begin in 2025.

This operation is mainly aimed at reinforcing investors’ confidence in order to increase their interest in the next issue of Cameroonian securities, estimated at XAF 200 billion and scheduled to be held in May 2023.

Further reading:

Investir au Cameroun — Cameroon begins the repayment of its 2022 bond loan with a payment of XAF14.6 billion

Final graph/chart image from Infogram here (pulls from this data). |