Nigeria: Easing cash crunch boosts manufacturing activity.

Ghana: Rice importation and cool market sentiments place downward pressure on the cedi.

South Africa: Weak U.S jobs data creates rand demand.

Egypt: Return of the current account surplus.

Kenya: World Bank to provide Sh40.8 billion to Kenya Power.

Uganda: Uganda has announced a new tourism initiative.

Tanzania: Expected increase in inflation as fuel subsidy removed.

XOF Region: Inflation remained at 5.7% in March 2023.

XAF Region: Prices of agricultural exports up 7.3% in Q1 2023.

Note: AZA Finance is reprising its sponsorship of Ghana’s industry-leading The Money Summit (TMS) 2023, organised by the Business and Financial Times (B&FT). Let us know if you will be attending the event on May 9 – we will be sharing our latest brief on Ghana and arranging background conversations with our Ghana country manager, Nana Yaw Owusu Banahene.

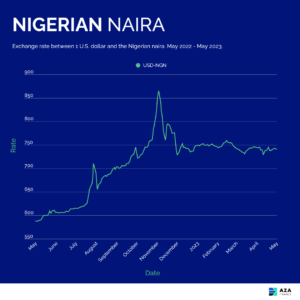

Nigerian Naira (₦)

Compiled by Ikenga Kalu

The naira remained relatively stable against the U.S. dollar, oscillating between USD/NGN 741 and USD/NGN 743 over the previous week. Nigeria’s manufacturing sector experienced a rebound in April after the federal government reneged on its decision to phase out the three largest naira denominations. The ease in the cash shortage caused a boost in both manufacturing output and customer demand which in turn led to an increase in the purchasing manager’s index to 53.8 in April from 42.3 in March. At present, cash is still king in the market as business owners defer to e-payment channels despite having physical cash for fear of a reenactment of the central bank cashless policy. As confidence in physical cash spending returns to the market, we expect a gradual increase in FX demand to push the USD/NGN rate beyond the current psychological level of 750 in the coming months.

Further reading:

Premium Times — Nigeria’s manufacturing activity rebounds in April as cash crisis eases

Ghanaian Cedi (GH¢)

Compiled by Murega Mungai

The cedi depreciated marginally against the greenback depreciated from USD/GHS 11.80 to USD/GHS 11.84 in the course of the week. High cost of machinery importation and import duties have put significant strain on rice producers in Ghana who struggle to meet the pent-up demand for the produce. Ghana also happens to be a heavy importer of rice which has been known to adversely affect local production, the local currency unit, and the general economy. As such, rice producers have called on the government to help assuage the situation so as to ensure local production begins to meet demand in the country. The cedi has been supported by positive sentiments related to the $3 billion IMF bailout package. However, with the next tranche of payments expected in the third quarter, there is room for further cedi depreciation in the coming months.

Further reading:

B & FT — High labor costs, import duties thwarting local rice production

Myjoy online — Earliest Ghana can secure IMF deal is 3rd quarter – Dr Ato Forson

South African Rand (R)

Compiled by Alex Barmuta

The rand opened the new week at 18.2636, as it continues its trend from last week — trading above the 18.00 support and under the 18.50 resistance level.

On Tuesday, the USD/ZAR rate briefly touched 18.50, before rejecting it to the downside. On Wednesday, we saw the rand continue moving further away from the 18.50 resistance level, as weak U.S. jobs data created some demand for the rand.

From a local perspective, data released showed that South African manufacturing activity remained in contractive territory in April (49.8 points), albeit less than March (48.1 points) and February (48.8 points) according to the Absa Purchasing Managers’ Index (PMI). Subdued growth projections in the economy (largely caused by continued rotational power cuts) also continue to weigh heavy on the rand.

Looking ahead, we can expect the rand to continue to trade between the 18.00–18.50 levels against the U.S. dollar — a range that has remained largely intact since the first week of April.

Further reading:

Businesstech — Rand on the back foot as markets hold their breath

Egyptian Pound (EGP)

Compiled by Mitchell Diedrick

The Egyptian pound remained relatively stable over the past week against the U.S. dollar and briefly breached the USD/EGP 31 level on May 1, 2023.

Data released by the Egyptian central bank revealed a current account surplus of 1.4 billion dollars for the quarter October, 2022 to December, 2022. The surplus can largely be attributed to a rise in exports, increased tourism and increased revenue from the Suez Canal, accompanied by a decrease in imports.

Pressure remains on the Egyptian pound to depreciate further in the latter part of 2023 in light of current conditions and requests by the International Monetary Fund (IMF) as part of the current loan facility.

In the week ahead the Egyptian pound should remain around the levels we have observed in recent weeks and gradually approach the USD/EGP 31.10 level.

Further reading:

Reuters — Egypt’s current account moves into surplus Oct-Dec

Kenyan Shilling (KSh)

Compiled by Terry Karanja

Kenyan shilling remained under pressure this week to a historic low of 136.02 against the U.S. dollar due to a shortage of dollars in the local market. Elevated forex demand from energy importers and rising U.S. interest rates in efforts to curb inflation has caused more pressure to the shilling. This has consequently pushed the costs of living high, especially food, electricity, and fuel prices and also caused distress to the government with regard to foreign debt repayment obligations. Kenya’s national electric utility company Kenya Power and Lighting Company (KPLC), will be provided with a Sh40.8 billion ($300 million) interest-free loan by the World Bank. The funds will be released through the treasury under a seven-year programme and will be used to help pay debts, renovate old transmission networks and expand the national grid. In the week ahead, we foresee more pressure on the shilling with increased forex demand with sustainable support from reserves that stood at USD 6,508 million a drop from USD 6,539 million the previous week.

Further reading:

Business Daily – World Bank lines up Sh40bn soft loan for Kenya Power

Ugandan Shilling (USh)

Compiled by Yadhav Panday

This Wednesday, May 3, the USD/USH traded at 3,725, down 0.27% from the previous trading session. Uganda, has announced a new tourism initiative. The country has stated that it will expand airfields at its national wildlife parks so that planes can land next to wild animals. People can also disembark there rather than at Entebbe’s National Airport. The announcement was made at an African tourism expo and is part of Uganda’s overall tourism strategy. In addition, Uganda’s parliament has watered down an anti-homosexuality bill that would have criminalized people for simply identifying as LGBTQ+. Human rights activists were outraged when the proposed legislation was first approved in March. Looking ahead, we expect the USD/USh to be worth 3,770.07 by the end of this quarter and 3,886.50 in a year.

Further reading:

Travel Pulse – Uganda Announces New Tourism Initiative

Tanzanian Shilling (TSh)

Compiled by Kristin Van Helsdingen

The Tanzanian Shilling remained trading within a narrow bracket against U.S. dollar this past week with its weakest level touching on 2,351, which is its weakest level since March 2019, and its strongest level of 2,347. Bid and offer rates for the Tanzanian shilling against the U.S. dollar are currently at 2,345 and 2,355 respectively.

On Wednesday, May 3, 2023, fuel subsidies that were implemented by the government in June 2022 to reduce the effects of inflation were removed. As a result, prices for petrol in the Northern Region increased by 90 Tanzanian shillings per liter, however, the prices in the southern regions remained stable as no new imports were needed.

In other news, Tanzania is talking about the prospects of joining forces with a Chinese company to build a 50 km bridge to connect the mainland to Zanzibar. Discussions of this bridge began this March.

As citizens start feeling the effects of rising fuel costs, we can expect the Tanzanian shilling to weaken slowly over the next few months. However, in the week ahead, we expect the Tanzanian shilling to remain relatively stable and trade around its weaker levels of USD/TZS 2,350.

Further reading:

THE CITIZEN — Fuel prices go up after removal of subsidies

THE CITIZEN — Tanzania to build bridge between Dar es Salaam and Zanzibar

West African CFA Franc Region (XOF)

Compiled by Jean Cédric Nando KOUA

The central bank’s tightening of monetary policy since the beginning of 2023 seems to be paying off. After falling in January, inflation stood at 5.7% at the end of March, the same level as the previous month.

In detail, inflation is mainly driven by the cost of food, housing, and transportation, which account for 4.6 percentage points of overall inflation.

Although declining, the level of inflation is still high compared to the economic union standard of 3%.

Further reading:

Sika finance — WAEMU: Inflation remains at 5.7% in March 2023

Central African CFA Franc Region (XAF)

Compiled by Jean Cédric Nando KOUA

Prices of agricultural exports from the XAF region increased by 7.3% in the first quarter of 2023.

The region benefited from increased global demand for bananas, cocoa, and rice, which saw their export prices rise by 11.7%, 10.9%, and 9.8% respectively. As for palm oil and rubber, which were down in the last quarter, the recovery in demand from China — the world’s largest importer — has had a strong impact on prices, with increases of 3.2% and 8.2% respectively.

This international situation is favorable for increasing government budget revenues and for strengthening the central bank’s foreign exchange reserves.

Further reading:

Investir au Cameroun — Prices of agricultural products exported from CEMAC up 7.3% in the 1st quarter of 2023

| Final graph/chart image from Infogram here (pulls from this data). |