The LMI for the second quarter 2022 increased by 1.2 to 65.9 from last quarter’s 64.7. There are indications of growth in the areas of inventory costs, warehousing prices and transportation prices.

However, inventory levels, warehousing capacity, warehousing utilization, transportation capacity and transportation utilization all have decreased. Although there is growth in the logistics industry, the rate of growth has slowed.

This slow growth rate may be attributed to high inventory cost and the associated cost of warehousing and transporting inventory. On the other hand, inventory level decreased to a record low level.

Warehousing capacity and utilization as well as transportation capacity and utilization all decreased, with lower rates recorded in the second quarter compared to the first quarter.

With the substantial decrease in inventory levels, the question that remains is whether inventory levels will show signs of increase anytime soon or if this downward trend of decreasing inventory levels will continue into the third quarter.

Researchers at the Centre for Applied Research and Innovation in Supply Chain – Africa (CARISCA) issued this report recently.

The Logistics Managers Index (LMI) is a new tool developed by CARISCA, based at Kwame Nkrumah University of Science and Technology, for Ghanaian businesses and policymakers.

The calculated LMI for Ghana, along with the accompanying analysis of its components, provides useful insights for the government of Ghana, business decision-makers, market analysts and investors, as it offers a predictive indication of overall economic activity in the country which is made available every quarter.

| The LMI measures the growth or decline of Ghana’s logistics industry based on eight key logistics components: | |

|

|

The LMI for Ghana study utilizes eight metrics to capture logistics activities in Ghana (as indicated above). The index measures combinations of inventory, warehouse and transportation activities and tracks the relationship between these variables to make inferences about their effects on the broader Ghanaian economy.

An index score is calculated for each of these components, and an overall index score (i.e., an LMI value) is then evaluated as a composite of these sub-indicators. This LMI value is expressed as a percentage with a mid-value/threshold of 50%.

An LMI value above 50% indicates a growing logistics industry, while a value less than 50% indicates a contracting logistics industry. This approach is an effective and reliable way to identify prevailing trends in logistics activities in Ghana. Due to its predictive nature, the LMI is also an effective tool for forecasting future trends in Ghana’s economy

IMPORTANT TAKEAWAYS FROM THE SECOND QUARTER LOGISTICS MANAGERS INDEX FOR GHANA

❖ This second-quarter study indicates that the overall Logistics Managers Index (LMI) for Ghana for the second quarter of 2022 stands at 65.9, up by +1.2 from first quarter’s reading of 64.7. This increase reflects a modest growth in Ghana’s logistics activities despite stresses from the COVID-19 pandemic, Russia-Ukraine war, cedi to dollar exchange rate depreciation and high inflation rates.

❖ Similar to the first quarter results, the values of all key indicators were above the threshold mark of 50%. Logistics cost is still high, with the three cost-related indicators (i.e., warehouse prices, inventory cost and transport prices) recording the highest values of the eight metrics in the second quarter of 2022 (85.1, 88.8 and 96.6, respectively). It seems there has been a carry-over of high cost of logistics operations from the first quarter into the second quarte

Obviously, the national currency depreciation against the U.S. dollar, which is currently trading at 12.45 cedis to one dollar, 1 has contributed immensely to this situation. Most warehouse rental rates as well as most imported inventory are priced in U.S. dollars. Transportation prices are also indirectly linked to the U.S. dollar because of rising petroleum prices on the international market. These cost drivers coupled with the constant constrained transport capacity, increasing demand for limited warehousing space, and increasing cost of supply of goods has contributed to the high cost of logistics operations in Ghana in the second quarter.

❖ The demand for warehousing continues to outstrip supply, and for the second time in a row warehouse capacity registered the lowest value among all the indicators. There is a real need for more warehouses and customer fulfillment facilities, especially in the industrial zones of Accra and Tema as well as in Kumasi. It is, therefore, not surprising that warehouse prices are high. As a result, companies are putting in maximum efforts to efficiently utilize limited available warehousing spaces.

❖ Current inventory levels have decreased substantially from the first quarter levels. Even though there is still a high demand for goods and services in Ghana’s economy, the current rate of cedi depreciation against the U.S. dollar has slowed down consumer spending, resulting in businesses stocking fewer inventories to minimize risks of obsolescence. This is a clear reversal from what was observed in the first quarter survey where Ghanaian businesses increased stock levels in anticipation of post-COVID-19 recovery of the economy. That enthusiasm was curtailed by the downgrading of Ghana’s credit rating by Fitch (CC), 2 S&P (CCC+/C) 3 and Moody (Caa2) 4 and the spiraling loss of the cedi’s value against the U.S. dollar.

❖ According to Moody’s, the downgrade is due to the “increasingly difficult task government faces in addressing the intertwined liquidity and debt challenges, pandemic induced revenue underperformance, tight funding conditions on international markets, materially decreasing governance and institutional strength and inflexibilities in the government budget.” 5 In a recent news item, it was reported that several supermarkets have voluntarily shut down operations due to the ongoing economic difficulties. The Food and Beverage Association of Ghana (FABAG) reports that the depreciation of the cedi, high tax rates, high interest rates and rising cost of doing business have led to an inability of businesses to re-stock goods, the resultant downsizing of workforce, shut down of businesses and in some cases the total folding up of businesses.

- Altogether, the economic situation is worrying because it seems to be having ripple effects on multiple sectors of Ghana’s economy. Continuation of this dire economic condition may have severe repercussions, including potential food shortages and the resultant hiking of food prices.

- Interestingly, predictions by respondents indicate optimism for an improved future growth in logistics activities in Ghana in the next quarter. However, the World Bank in its October 2022 Africa Pulse report revised Ghana’s growth rate to 3.5%, below the initial estimate of 5.5% for the first quarter of 2022.[1] The World Bank estimates that Ghana’s economy has been struggling with various setbacks, including rising public debt (104.6% of Gross Domestic Product), elevated inflation (33.9% in August 2022), and a depreciating currency. The direct implication is a weakening of private sector business activities. Despite the headwinds facing Ghana’s economy, the logistics managers seem to be optimistic about future improvement in growth of logistics activities in Ghana.

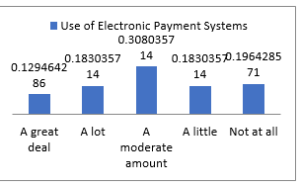

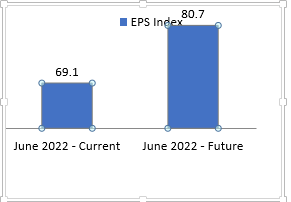

- An interesting new metric in this second quarter report is the Electronic Payment System metric, which gives an indication of the usage level of electronic payment systems, including mobile money transfers, electronic/bank transfers, electronic card payments and other cashless monetary transactions by logistics companies and their customers. The current value for this metric is 69.1%, which is above the threshold of 50% and indicates a growing use of electronic payment systems by Ghanaian businesses for logistics activities. The implication of this for managers and investors is that Ghana’s economy supports e-transactions and payments with usage at a high level that is likely to increase in the future. Moreover, Ghana’s logistics industry is driven by financial technology with great promise for future innovations in the form of new fintech products and services such as block chain technologies.

RESULTS OVERVIEW

The second quarter results of the LMI summarize the responses of logistics and supply chain professionals obtained from multiple industries in Ghana between June and July 2022. Overall, the LMI for Ghana is up by +1.2 from first quarter’s reading of 64.7 to 65.9. There is an indication of growth in areas of inventory costs, warehousing prices and transportation prices. However, inventory levels, warehousing capacity, warehousing utilization, transportation capacity and transportation utilization have decreased. We are seeing sustained growth in the Ghanaian logistics industry albeit at a slow rate. The increase in growth observed is a result of the increasing cost metrics, namely: inventory cost, warehousing cost and transportation cost. However, capacity and utilization metrics have decreased.

While this second quarter LMI score of 65.9 does not reflect significant increase in logistics activity growth, it is slightly higher than that for the first quarter LMI score of 64.7. It is important to note that this growth is coming at a time when Ghana’s economy is facing major headwinds with the World Bank GDP growth rate projections revised downward to 3.5%, below the initial estimate of 5.5% for the first quarter.

Consumer spending is at an all-time low, with several labor unions agitating for increment in wages to be at par with the rising cost of living in Ghana.

Comments from the Africa Region Director of the International Monetary Fund (IMF), Abebe Selassie, indicate that Ghana’s inflation had risen to 37.2% and had been on the upward trajectory from the beginning of the year.

While the Government of Ghana has highlighted external factors as key contributors to Ghana’s declining economic condition, including the aftershocks of the COVID-19 pandemic, the Russia-Ukraine war (Ghana imports 40 percent of its fertilizers from Russia), the IMF raises concerns that internal factors have largely contributed to this scenario.

Similar to the United Kingdom (with a current inflation rate of 14.6%), soaring food prices seem to be the largest contributor to the rising inflation rate in Ghana. On the basis of the current unfavorable business environment, businesses seem to be less optimistic about growth prospects in the second quarter of 2022.

The Bank of Ghana’s business confidence survey in June 2022 revealed a drop in the level of optimism among businesses from 85.9 in April, 2022 to 79.7. This is the lowest business sentiment recorded since February 2017.

The report indicates that businesses were concerned about the cost of inventory (raw materials), rising labor costs, exchange rate volatility and weak consumer demand. According to Ernest Addison, the governor and chairman of the Monetary Policy Committee (MPC) of the Bank of Ghana, “these conditions have adversely impacted business optimism and prospects.”

It seems these macro-economic challenges have contributed to a drop in inventory levels from 65.5 to 56.9 (-8.6). This downward trend of decreasing inventory levels is an indication that businesses may not be thriving well as predicted in the first quarter.

Many retail unions like the Food and Beverage Association of Ghana (FABAG)[2] and the Ghana Union of Traders Association (GUTA) have indicated that some of their members have closed shops due to the increasing cost of doing business in Ghana. Large retailers and supermarkets like CityDia Supermarket chain and Spar Supermarket have also been closed. The GAME supermarket, is currently experiencing the lowest inventory levels in the history of its operation in Ghana.

The major trade associations cite several factors that have contributed to the current situation, including the rapid depreciation of the cedi, high interest rates, and high taxes, unnecessary levies on import duties, high petroleum prices and challenges with the recently introduced Electronic Transfer Levy (i.e., e-levy of 1.5%). The S&P Global Purchasing Managers Index (PMI)[3] for Ghana reported a slight increase in June 2022 (48.5) from May 2022 (47.4). This is worrying because the values for the last two months have both been below the 50-point threshold.

Altogether, the economic situation is worrying because it seems to be having ripple effects on multiple sectors of Ghana’s economy. Continuation of this dire economic condition may have severe repercussions, including potential food shortages and the resultant hiking of food prices. The emerging picture is that the first-quarter high inventory levels could have been artificial in the sense that part of that inventory was due to late-arriving goods as a result of supply chain congestion in the later part of 2021.

Considering the drop in inventory levels, it is interesting that respondents reported only a slight increase in the cost of inventory from 88.7 in the first quarter to 88.8 (+0.1) in the second quarter. Inventory costs appear to be steady for now, and we are keenly observing how this plays out in the next quarter. Without a major intervention, it is likely that inventory cost is going to shoot up in the next quarter.

Warehousing prices and transportation prices both registered increases from the first quarter. Warehouse prices went up by 6.7 points from 78.4 in the first quarter to 85.1 in this quarter (Q2). Transportation prices increased by 2.7 points from 93.9 in the first quarter to 96.6 in this quarter (Q2). The transport price metric sets the record for the highest metric of the index so far at 96.6 in the second quarter. The increase in warehousing and transportation prices is largely accounted for by macro-economic factors that have influenced the cost of doing business in general. A substantial demand for warehousing space and a lack of capacity contribute to the rate of growth in warehousing prices.

Transportation prices as usual were affected by the global surge in fuel prices. As of January 2022, the price of gasoline in Ghana has increased by approximately 67 percent. Currently, the price of gasoline in Ghana stands at 12.32 Ghana cedis (GHS) per liter (equivalent of 0.98 U.S.dollars per liter).[4] Figure 2.0 shows monthly gasoline price changes in Ghana between October 2020 and October 2022. Although the chart only shows prices for gasoline, historically diesel and retail gasoline prices often move together.

To hedge against price increases and take advantage of quantity discounts, large carriers have often made wholesale purchases; however, this has become increasingly expensive because of Ghana’s currency depreciation against the dollar. In rare cases where some large carriers have funds to make such purchases, they find themselves often constrained by the lack of storage capacity.

Use of Electronic Payment Systems

A new feature in the second quarter LMI report is the evaluation of the use of electronic payment systems by logistics companies. Our study gauged the views of respondents (supply chain and logistics managers) on the extent of usage of electronic payment systems when transacting business with suppliers and customers.

logistics companies

We define electronic payment systems as a collective phrase for many different kinds of methods used to facilitate commerce transactions electronically. These include, electronic cash (E-cash)/electronic banking(e-banking), mobile payment (popularly called MoMo in Ghana), debit/credit and smart cards, cyber cash, electronic cheques, electronic funds transfer and digital wallets (electronic wallets). These electronic payment systems and methods make purchasing and procurement easier, more cost-effective and time saving. Oftentimes these systems help improve the management of supply chain financing as a result of improved financial data visibility.

PREDICTED FUTURE LMI VALUES FOR GHANA

Table 2.0 also shows the predicted future values for all eight metrics from the second quarter survey (June 2022). To generate the predicted future LMI values for Ghana, we asked respondents to predict movements in the individual metrics for the next 12 months. Results show that the respondents are optimistic about the potential for increased logistics activities over the coming year.

They predicted continued growth in all metrics except for the cost metrics (inventory costs, warehousing prices and transportation prices), which were predicted to decrease. Inventory cost was predicted to drop by a margin of -5.1; warehouse prices by a margin of -2.2 and transportation prices by a margin of -7.7. This observation indicates a high level of optimism on the part of respondents that improvements in the general economy in the near future will reduce the cost of doing business and as a result bring down these cost metrics.

Table 2.0: Predicted Future Values of the LMI – June 2022

| LOGISTICS AT A GLANCE | ||

| Index | June 2022—current | June 2022—predicted future |

| LMI | 65.9 | 67.3 |

| Inventory Levels | 56.9 | 75.8 |

| Inventory Costs | 88.8 | 83.7 |

| Warehousing Capacity | 56.6 | 72.7 |

| Warehousing Utilization | 62.8 | 79.3 |

SECOND QUARTER OBSERVATIONS

The overall LMI in the second quarter (65.9) is slightly higher than what we saw in the first quarter (64.7) with a delta of 1.2. This increase is largely due to growth in the areas of inventory costs (0.1), warehousing prices (6.7) and transportation prices (2.7).

However, there were significant drops in the rate of growth for inventory levels (-8.6), warehousing capacity (-5.0), warehousing utilization (-6.4), transportation capacity (-4) and transportation utilization (-9.8). Nevertheless, all eight metrics registered values above the threshold of 50%. We are seeing a gradual sustained growth in the Ghanaian logistics industry. Logistics growth in Ghana has not been as high as predicted in March (66.5).

This may be attributable to the beginnings of a sharp slump in the Ghanaian economy brought on by increasing interest rates, high inflation and a depreciating local currency value against the dollar which has negatively affected demand. Though it is impossible to tell at this moment how things will turn out, it is clear that the rate of growth in the logistics industry is slowing down at a time when things should have been picking up.

Comparing the LMI in Ghana with the U.S. LMI, it can be seen that, in general, growth in the logistics sector is slowing down, possibly as a result of global economic and geopolitical factors (e.g., inflation, increasing fuel prices, Russia-Ukraine war). The LMI value for the USA (an economy with a GDP of $25 trillion compared to Ghana’s $74 billion) in June 2022 was 65.0; a drop of 2.1 from the previous month’s value of 67.1.[5]

Respondents are, however, positive that growth observed in the logistics sector in the second quarter of 2022 will increase in the future and predicted a future LMI value of 67.3. It will be interesting to continue monitoring these rates of growth through Q3 to observe whether or not economic activity picks up, especially with the pending bailout by the IMF.

Predicted future LMI values for Ghana

Table 2.0 also shows the predicted future values for all eight metrics from the second quarter survey (June 2022). To generate the predicted future LMI values for Ghana, we asked respondents to predict movements in the individual metrics for the next 12 months. Results show that the respondents are optimistic about the potential for increased logistics activities over the coming year.

They predicted continued growth in all metrics except for the cost metrics (inventory costs, warehousing prices and transportation prices), which were predicted to decrease. Inventory cost was predicted to drop by a margin of -5.1; warehouse prices by a margin of -2.2 and transportation prices by a margin of -7.7. This observation indicates a high level of optimism on the part of respondents that improvements in the general economy in the near future will reduce the cost of doing business and as a result bring down these cost metrics.

Table 2.0: Predicted Future Values of the LMI – June 2022

| LOGISTICS AT A GLANCE | ||

| Index | June 2022—current | June 2022—predicted future |

| LMI | 65.9 | 67.3 |

| Inventory Levels | 56.9 | 75.8 |

| Inventory Costs | 88.8 | 83.7 |

| Warehousing Capacity | 56.6 | 72.7 |

| Warehousing Utilization | 62.8 | 79.3 |

ABOUT THE LOGISTICS MANAGERS INDEX FOR GHANA

The Logistics Managers Index (LMI) for Ghana is a study by the Center for Applied Research and Innovation in Supply Chain – Africa (CARISCA) at the School of Business at Kwame Nkrumah University of Science and Technology (KNUST) in Kumasi, Ghana.

This project is a collaboration between KNUST in Ghana and Arizona State University (ASU) in the United States, with support from the United States Agency for International Development (USAID).

This study was led by Emmanuel Kweku Quansah (Ph.D.), Nathaniel Boso (Ph.D.) and Abdul Samed Muntaka (Ph.D.) of KNUST.

The Logistics Managers Index (LMI) for Ghana makes no representation other than that stated in this release regarding the individual company data-collection procedures. The data should be compared to all other economic data sources when used in decision-making.

Logistics Managers Index for Ghana – Request for Permissions

Requests for permission to reproduce or distribute the contents of the Logistics Managers Index for Ghana should be sent (in writing) to Professor Nathaniel Boso, CARISCA-KNUST Secretariat, PMB, KNUST School of Business, Kumasi, Ghana. Alternatively, requests for permission can be made by sending an email to [email protected].

The authors of the Logistics Managers Index for Ghana report shall not have any liability, duty or obligation for or relating to the content of the Logistics Managers Index for Ghana or other information contained herein, any errors, inaccuracies, omissions or delays in providing any Logistics Managers Index content, or for any actions taken in reliance thereon. Under no circumstances shall the authors of the Logistics Managers Index for Ghana be liable for any special, incidental or consequential damages arising out of the use of the Logistics Managers Index for Ghana.