")

Access to affordable housing remains one of the critical socio-economic challenges facing many developing countries. A huge gap between housing demand and supply of affordable housing units persists, compounded further by ever-increasing home prices beyond the reach of workers’ wages.

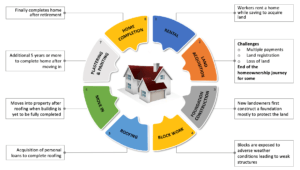

The homeownership journey for many is long, complicated, and sometimes overwhelming with many resulting to unconventional means of securing housing. Land acquisition, finding the right professionals for construction, and obtaining financing often present huge challenges. The myriad of activities involved in the traditional home acquisition process can be confusing and opaque, sometimes leading to financial loss. Due to these difficulties, many low- and middle-income earners retire without achieving their homeownership dream.

Financing Ghana’s Housing Deficit

Ghana’s 2021 population and housing census puts the national housing deficit at 1.8 million units. Estimates indicate that the annual housing demand is between 70,000 to 120,000 housing units with only about 30% of the annual demand supplied. With average cost of constructing a two-bedroom house in the urban areas estimated at about GHS 267,000, affordability remains at the core of the housing challenge, as majority of working-class Ghanaians would not be able to afford a home due to low-income levels.

With average interest rates on cedi-denominated mortgages from commercial banks ranging between 19.00% and 31.7%, majority of people within the low- and middle-income bracket would not qualify for a mortgage. This creates a situation where potential homeowners are left with the choice of building their homes incrementally which, in most cases, can take anywhere from 10 to 20 years or, in some cases, one’s entire working life.

The Ghanaian Worker’s Pathway to Homeownership

The average Ghanaian worker has three main pathway options in the homeownership journey: self-build, outright purchase, and mortgage acquisition. The homeownership journey for many starts when they receive their first pay cheques. Bank-financed options to achieve homeownership remain limited due to low incomes and high mortgage costs. Mortgages from commercial banks are sometimes priced in US Dollars, completely unaffordable for low- and middle-income workers earning Ghana Cedis. Similarly, houses offered by developers for outright purchase are often priced in US Dollars.

Therefore, for a segment of workers who cannot afford to access mortgage from the commercial banks, they start saving towards buying land to build their future homes as soon as they start to earn an income. Many prospective homeowners make initial down payments for land and pay the outstanding balance over time, while some secure loans to pay for the land and repay the loan over time. Owing to the challenges associated with land acquisition especially in the urban areas with its attendant litigations and loss of investments, some would-be homeowners are forced to end their homeownership journey when they fail to acquire a piece of land.

For prospective homeowners who overcome the land acquisition challenges, the remaining journey can extend for many years characterized by difficulties with finding qualified artisans, raising needed financing, loss of building materials to theft, and long exposure of uncompleted buildings to adverse weather conditions resulting in compromised structural integrity, before they finally get to occupy the homes. In many instances, people move into their uncompleted homes after retirement due to reduced income. In the interim, most live in rented accommodation and may pay rent for their entire working Lives.

The Rent-to-Own Model

In urban areas, data from the Ghana Statistical Service suggests that majority of occupants in residential properties are non-owners and are typically involved in some form of rental arrangement.

In most instances in Ghana, a first-time tenant is required to pay two- or three-years’ rent in advance, and subsequently one year’s rent advance upon each renewal of tenancy. The huge financial burden that rent payment places on tenants for many years in the traditional rental arrangement does not in any way provide for ownership opportunities, regardless of how long they rent the home.

A significant shift from the traditional rental arrangement is the concept of rent-to-own. Imagine a rental arrangement where the tenant can eventually own the home at the end of a defined period; a rent-to-own arrangement offers tenants this opportunity. A rent-to-own arrangement allows tenants to rent a home with an option to buy the home at the end of a defined rental period. In the rent-to-own model, the tenant pays an additional deposit with each monthly rent payment which goes towards the purchase price of the home at the end of the rental period.

Types of Rent-to-Own Schemes

There are two main types of rent-to-own arrangements: the lease-option and lease-purchase arrangements. In lease-option arrangement, the tenant pays an upfront fee of about 5% of the value of the home. The upfront payment gives the tenant an option to buy the home at the end of the rental period at a value to be agreed on by the buyer and the seller. The upfront fee paid by the tenant is applied to the final cost of the home. The tenant agrees to make monthly payments a little above the market rent rate for the property. The excess payments above market rent goes towards the down payment for the purchase of the property. On the option exercise date, the rent credit serves as down payment to enable the tenant purchase the home. The tenant retains the right to opt out of the agreement if s/he decides not to buy the property.

On the other hand, the lease-purchase is a type of rent-to-own arrangement where the tenant and property owner agree on the price of the property upfront. The tenant makes monthly payments above market rent rate and the excess goes towards down payment of the home. In a lease-purchase agreement, the tenant is obliged to purchase the home at the end of the lease period and loses the down payment if tenant fails to provide funding to purchase the home. Furthermore, the property owner can sue for breach of contract if the tenant fails to purchase the home at the end of the lease period.

While the lease-option agreement gives the tenant more flexibility in the home acquisition process, this arrangement presents uncertainty in the final home price as the price is determined at the end of the lease period and may be above the tenant’s budget. The lease-purchase, on the other hand, lacks flexibility for the tenant in cases where tenants decide to change their mind, but the risk of property price increasing above tenant’s income is minimized.

Home Maintenance and Insurance

In a rent-to-own arrangement, the prospective homeowner is both a tenant and a buyer. Prospective homeowners therefore have more responsibilities in a rent-to-own scheme than they would in a traditional rental arrangement. Unless the agreement states otherwise, the tenant is responsible for some maintenance works in the home. Some rent-to-own agreements make major maintenance such as changing of roofing and other structural works the responsibility of the seller. However, maintenance works such as house painting, replacement of sinks and landscaping are usually the responsibility of the prospective homeowner under rent-to-own arrangement.

There are different types of home insurance available to protect residential properties and contents. A renter’s insurance is meant to protect the personal belongings of the tenant; a landlord insurance offers homeowners protection for rented properties; and homeowners’ insurance which is taken by the owner of the property. Since tenants build up equity in a home over a period of time albeit on paper, it is important to ensure that the property has an insurance cover to protect the tenant’s investment under a rent-to-own arrangement. Because the seller owns the property during the rent-to-own tenor, the seller usually carries homeowner’s insurance while the parties agree on how to share the insurance cost. The tenant on the other hand may acquire a renter’s insurance to protect belongings in the home.

The Ideal Rent-to-Own Candidate

Rent-to-own arrangements could offer an ideal solution for both tenants and landlords. Rent-to-own is a good choice for tenants who would like to buy a home but do not have the initial down payment or qualify for a mortgage. Tenants get the opportunity to move into a home and start enjoying the benefits of a homeowner while building up equity over time.

The Benefits

In addition to giving tenants the opportunity to build equity in the home over a period, tenants have the flexibility to walk away from the arrangement if their financial situations change or if they lose interest in purchasing the home. The rent-to-own arrangements also increase the chances of property owners, who are experiencing difficulties in selling their properties, to find buyers while gaining rental income in the interim. Additionally, property owners enjoy a long-term reliable tenants and lower home maintenance cost.

Increasing Homeownership Rate Through Rent -to-Own Scheme

As previously indicated, affordability remains a major hindrance to housing delivery in Ghana as a huge mismatch persists between the cost of houses and mortgages on the one hand, and the income levels of potential homeowners on the other hand.

Due to the relative flexibility offered, rent-to-own schemes have the potential to move many potential homeowners up the property ladder, thereby increasing the homeownership rate substantially.

Creating the Enabling Environment for Effective Rent-to-Own Schemes

A fundamental logic behind rent-to-own is to provide a cheaper, more affordable alternative path to homeownership for persons who cannot afford conventional mortgages from banks.

However, the high cost of housing units – even those labelled ‘affordable’ – presents a strong challenge to the rollout of rent-to-own schemes, as the property costs impact the rental charges. Higher house prices translate into high monthly rent-to-own payments, pricing out target candidates.

Currently, at the typical prices of ‘affordable’ houses, the difference between monthly rent-to-own rates and typical monthly mortgage obligations tends to be quite narrow. In effect, many low-income potential homeowners for whom the rent-to-own path should have been beneficial, i.e., a cheaper alternative to mortgages, end up unable to afford this alternative route as well.

For rent-to-own schemes to achieve the intended purpose of increasing the homeownership rate especially among low- and middle-income earners, a supportive cost and regulatory environment must exist, to underpin affordability and sustainability of house prices. Invariably, government intervention is necessary for the creation of this supportive environment.

The specific government interventions below are sine qua non to ensure stable, affordable house prices, and by extension, affordable rent-to-own rates:

- provision of low-cost land banks, eliminating the excessive costs of private land acquisition and the associated costs of multiple payments for same piece of land, the menace of ‘land guards’, etc.;

- provision of communal infrastructure (access roads, drainage, electricity, water), the costs of which are presently borne by private estate developers and thus built into house prices;

- provision of construction financing at concessionary rates, as the burden of expensive bank loans also adds to the unsustainable cost build-up of even the houses that are intended to be affordable.

Additionally, rent laws and regulations must be updated to accommodate the rent-to-own concept. This is essential to protect both rent-to-own providers and subscribers. The rights and responsibilities of parties under rent-to-own schemes must be duly covered in the regulations to prevent scheme providers from taking advantage of vulnerable subscribers and vice versa, as well as providing a regulatory framework for transfer of title and dispute resolution.

Beyond government intervention, estate developers also ought to explore lower cost construction technologies and materials, without compromising quality, of course.

Conclusion

With majority of residents in urban areas engaged in some form of rental arrangement, a scheme that will enable tenants transition into homeowners will have a positive impact on homeownership rates in Ghana.

The rent-to-own model presents a huge potential not only to increase homeownership but also the delivery of affordable housing to meet increasing demand as the scheme holds the potential to move people who would otherwise not qualify, onto the homeownership ladder. The resultant increased demand for affordable housing will spur developments to satisfy the demand.

Governments and non-governmental organizations have initiated several interventions to increase the delivery of housing and uptake of same especially among middle- and lower-income earners. For these interventions to achieve the intended impact, challenges surrounding housing affordability must be addressed critically, especially in the current environment where a huge disparity exists between income levels and home prices.

Successful implementation of rent-to-own schemes would hinge on supportive inputs of stakeholders, especially government. Government must facilitate the enabling environment through regulation, provision of affordable landbanks, provision of necessary infrastructure as well as funding for research into the use of local materials for development of high-quality low-cost affordable houses. Proper implementation of the rent-to-own model will fill a very critical gap in the housing market, facilitating ownership access for the segment of the market that cannot afford traditional mortgages.