When I started my banking career around 2008 right from the University of Ghana, Legon with a certain global bank, I was privileged and honoured to join their Transaction Banking (TB) team and in fact, that team was the product development and sales specialist supporting the Client Coverage unit within its Corporate and Institutional Banking.

I can confidently say those moments were the turning point of my career, I was so much exposed to Cash Management, International Trade Finance and Securities Services products. While I could close my eyes and deal with Cash Management products with no high temperature, Trade Finance was the reverse at the time. Trade Finance appeared so technical and broad.

Thankfully, with years of experience, it was actually less daunting than imagined. This was also because, the products in Trade Finance range from Flow and Financial Institutions (FI) Trade, Open Account Trade (OAT), Structured Solutions, Trade Distributions etc. Having worked in TB, I realised that, very few people knew the importance of opening Letters of Credit (LCs) as a means of payment to clients. This article will focus on a few aspects of LCs. This piece is very important because LCs are major products and services commercial banks deliver to their customers.

As of 2019, the global Letter of Credit confirmation market size was valued at US$4.30bn and even projected to reach US$4.99bn by 2027, growing at a CAGR of 3.18% from 2020 to 2027. This is according to a report published by Global Opportunity Analysis and Industry Forecast, 2021-2027. Major factors driving the growth of Letter of Credit Confirmation Market size are the rise in demand for customised trade finance solutions and regulatory support in the growth of strict regulations for a secured letter of credit confirmation services.

Interestingly, the increased risk of non-payments is driving the growth of the letter of credit market size. As global trade grows, both importers and exporters are largely taking security steps against their trade documents in order to avoid the risk of payments in the market. Moreover, the seemly lack of confidence between the exporter and the issuing bank located in countries of high political or economic instability, confirmation of the letter of credit document is considered safe for global trading. Thus, traders today prefer LC confirmation services, thereby increasing the market size.

Furthermore, increased business operations and foreign trade between SMEs and large enterprises offer lucrative opportunities for confirming banks to expand their business in the letter of credit confirmation services in the market.

Importantly, with the emergence of Fintechs, new technological developments are expected to increase the LC market size. Advancements in technologies such as blockchain and Distributed Ledger Technology (DLT) are all expected to create lucrative opportunities for the LC confirmation industry. As a result of these technological advances, credit confirmation providers can create a digitised letter of credit contract in real-time, warn auto alerts to trades, and improve business efficiency in the marketplace.

In addition, in order to ease the conventional & lengthy process of reviewing trade documents by banks and clients, traders are expected to introduce the letter of credit confirmation services, which in turn is expected to provide lucrative growth opportunities. The untapped potential of emerging economies is expected to provide lucrative growth opportunities for the letter of credit confirmation market.

Developing economies, such as Ghana, provide substantial opportunities for confirming banks to increase their business by improving their product offerings and promoting the growth of trade operations. In this piece of article, the focus is to demystify the overall concept of LCs and how businesses can leverage on it to expand their business growth.

Why use Letter of Credit

In simple terms, a letter of credit is the situation whereby a bank undertakes to make a payment, separated from the sales or other contracts on which it is based. As already mentioned, it is just a way of reducing the payment risks associated with the movement of goods.

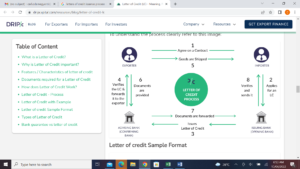

Expressed more fully, it is a written undertaking by a bank (issuing bank) given to the seller (beneficiary) at the request, and in accordance with the buyer’s (applicant) instructions to effect payment – that is by making a payment, or by accepting or negotiating bills of exchange (drafts) – up to a stated amount, against stipulated documents and within a prescribed time limit.

An LC is essential when a buyer and seller have to consider the mode of payment in the course of negotiating the transaction. Generally, payment can be made in several different ways: by the buyer remitting cash with his order; by opening an account whereby the buyer remits payment at an agreed time after receiving the goods; or by documentary collection through a bank in which case the buyer pays the collecting bank for the account of the seller in exchange for shipping documents which would include, in most cases, the document of title to the goods.

In the aforementioned methods of payment, the seller relies entirely on the willingness and ability of the buyer to effect payment which I see to be quite risky. Even though the open account option of payment is largely used, the buyer is forced to source for immediate forex to pay the seller. This is not so considerable, on the basis that in the event of dollar liquidity squeeze on the market, a buyer may end up breaching trust with business partner when payments are not made.

Importantly, I have seen that when a seller has doubts about the credit-worthiness of the buyer and wishes to ensure prompt payment, the seller/supplier can insist that the sales contract provides for payment by irrevocable letter of credit.

Furthermore, if the bank issuing the letter of credit (issuing bank) is unknown to the seller based in another country or if the seller is shipping to a foreign country and is uncertain of the issuing bank’s ability to honour its obligation, the seller can, with the approval of the issuing bank, request its own bank – or a bank of international repute such as Standard Chartered Bank – to assume the risk of the issuing bank by confirming the letter of credit. When the seller has doubts about the credit-worthiness of the buyer and wishes to ensure prompt payment, the seller can insist that the sales contract provides for payment by irrevocable letter of credit.

Some basic types of LCs

There are three basic features of letters of credit, each of which has two options. Each letter of credit has a combination of each of the three features. In addition to these basic types, there are various specialised formats which meet particular sets of circumstances such as Red Clause Letter of Credit, Transferable Letter of Credit, Back-to-Back Letter of Credit, Deferred Payment Letter of Credit and Standby Letters of Credit.

Key Features of LCs

-

Being Sight/Usance.