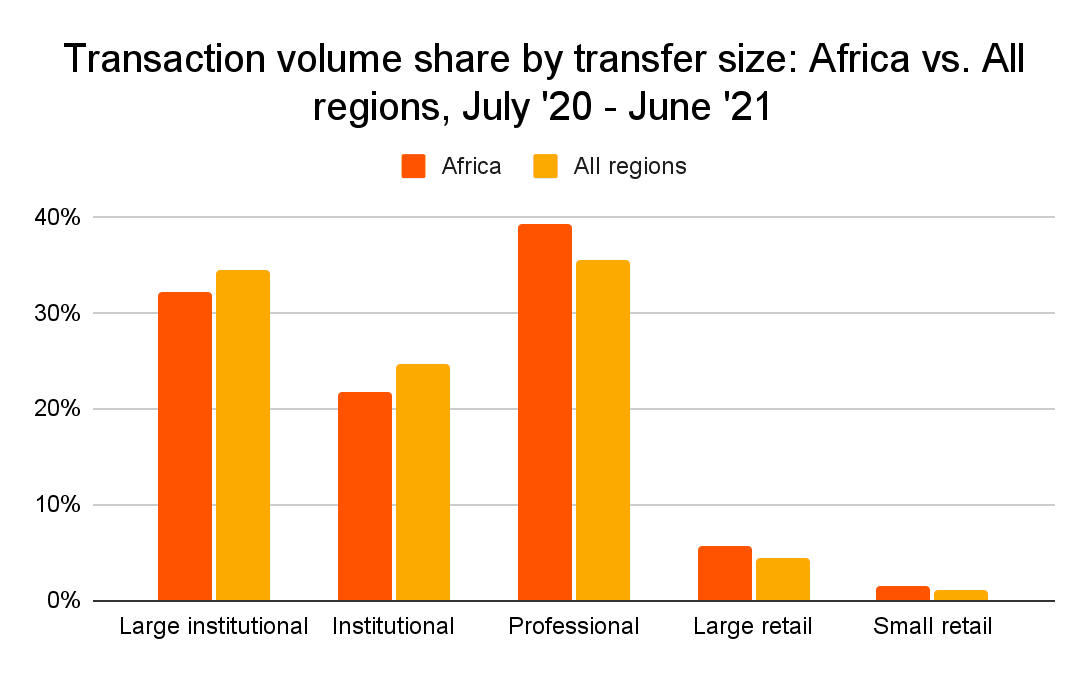

Africa’s emerging Crypto economy

0 views

Topics in this article

cryptocurrencyAfrica’s emerging Crypto economy

Related Coverage: Features

Features

Stress in disasters: Providing mental health first aid

The recent floods in Accra reminded me of a personal experience on June 3, 2015, when I was affected by a similar disaster at Kaneshie.

Features

The Inconvenient Truth with Ing. Professor Douglas K. Boateng: Are we governing a future we have already decided not to visit?

The question history is quietly asking History does not rush. It rarely applauds a government, a boardroom or a generation on the day a decision is made. It waits to see whether today's celebrated choice becomes tomorrow's triumph or tomorrow's regret, asking a question no election result or quarterly report can answer honestly.

Features

MIIF’s most valuable assets: Resilience

A couple of weeks ago, the Minerals Income Investment Fund (MIIF), the state entity set up by the Government of Ghana to manage the country’s mineral wealth through royalty collection and investment, published its audited financial performance for 2025, and the results are nothing but impressive demonstration of financial resilience by a state institution in recent times.

Features

Ghana and the IMF: The relapsing patient syndrome

Ghana has once again completed an International Monetary Fund (IMF) programme – its seventeenth engagement with the Bretton Woods institution since independence.

Features

The Attitude Lounge with Kodwo Brumpon: Long and short straws

“The pigeon sleeps above, the ram below.” – Akan proverb

Features

Beyond the budget: How 2026 mid-year review could transform wealth management, financial inclusion and the digital economy

National budgets are often evaluated by how much governments collect in revenue or spend on infrastructure, education and healthcare. Yet their true influence extends much further.

Features

Realising an economy of 'milk and honey'

The biblical phrase "milk and honey" symbolises ultimate ecological productivity, self-sufficiency, and shared prosperity.

Features

Why geology conference could shape Africa's next mining boom

As the global race for gold, lithium and other critical minerals intensifies,

Comment guidelines

Please keep comments respectful. Use plain English for our global readership and avoid using phrasing that could be misinterpreted as offensive. By commenting, you agree to abide by our community guidelines and these terms and conditions. We encourage you to report inappropriate comments.

No comments yet. Be the first to share your thoughts.