…yields trending high ahead of US Fed taper

The cost of government financing on the secondary bond market has been on the rise since the third quarter of 2021, with yields rising more broadly across the curve ahead of the start of the US Fed taper timeline which begins next month.

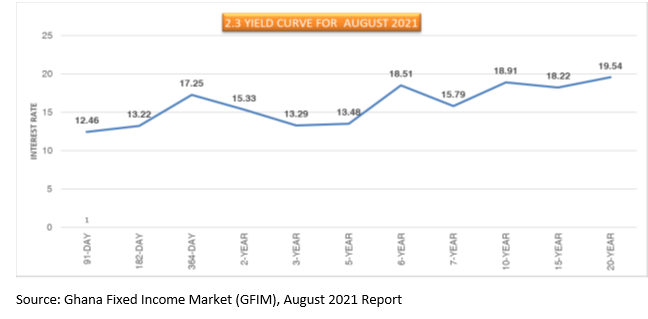

On the Ghana Fixed Income Market, yields are on the ascendency – with the two-year Treasury note rising from 15.33 percent in August 2021 to 17.5 percent in September 2021. Medium-term maturities: the three-year, five-year, as well as six-year, and seven-year, also rose from 13.29 percent, 13.48 percent, 18.51 percent, and 17.6 percent in August to 13.71 percent, 15.49 percent, and 19.4 percent respectively in September 2021.

Long-term bonds: 10-year, 15-year similarly increased to 19.02 percent and 19.63 percent in September 2021 from 18.91 percent and 18.22 percent in August respectively. However, the 20-year bond remained unchanged during the period at 19.54 percent.

From a borrowing requirement perspective, there will be a sharp tightening of financing conditions, resulting in a significant premium on the cost of government borrowing as well as other borrowers on the market.

Senior Economist with Databank – an assets management company, Courage Kingsley Martey, said yields have been under upward pressure since the late third quarter, especially beginning September 2021; largely due to the cedi-liquidity crunch as well as the US Fed Taper, which is set to be next month.

Mr. Martey said: “There are two main reasons for this upward pressure on yields. First, cedi-liquidity is quite tight on the market since September. This is fuelling selling pressure on the bond market across maturities and exerting upward pressure on yields.

“Secondly, the US Fed announced its taper timeline in September, expecting to start reducing the size of its bond purchase programme from November this year into mid-2022. This announcement has expectedly heightened non-resident aversion to securities of emerging and frontier markets. These dampened appetites have also created some selling pressure and increasing bond yields,” he stated.

Ever since the US Fed signalled a ‘fast’ taper at its September meeting, with tapering likely to start next month and quantitative easing (QE) concluding by mid-2022, globally, longer-term bond yields have risen, in a repeat of the sell-off earlier in 2021 according to the Institute of International Finance (IIF).

“One way government could deal with this is by building buffers, right now, to enable the fiscal authorities navigate the tight conditions without undermining their fiscal consolidation and growth revitalisation plans.

“For the monetary policy authorities, it might be appropriate to stand ready to use the interest rate channels as a means to sustain the appeal of domestic financial securities in order to reduce the shock of foreign portfolio outflows,” he said.

For the rest of this year, the market anticipates continued upward pressure on domestic yields as liquidity remains tight and offshore investors continue to prefer dollar-denominated securities against cedi-denominated securities.

The current uptrend in yields also reflects the increased FX and inflation risks for the second half of 2021, largely the pricing of increased risk of FX and depreciation. However, for Treasury-bills yields seem to have bottomed out and now stabilised between the mid-12 percent to the low-13 percent levels, as the market balances government’s yield compression against the elevated inflation risks.

A market analyst with Fincap Securities Limited, John Nani said: “With the uptick of inflation over the third quarter, it’s only usual to expect increases in yield and the market has responded accordingly. Yields have been on an uptrend since the beginning of the Q3 until now. Moreover, the recent liquidity strain in the capital market has not helped the situation as yields increase in order increase investors’ appetite for securities”.