Given the latest rise in consumer inflation, any further rise in inflation could sustain upward pressure on domestic debt yields, Courage Kingsley Martey, Senior Economist with investment bank Databank has said.

Data from the Statistical Service showed that the consumer price index inched up to 7.8 percent year-on-year in June 2021 from the 7.5 percent recorded previously in May. “The rise in inflation – if sustained into the second half as expected – could sustain the upward pressure on domestic debt or bond yields,” Mr. Martey said in an interview with B&FT.

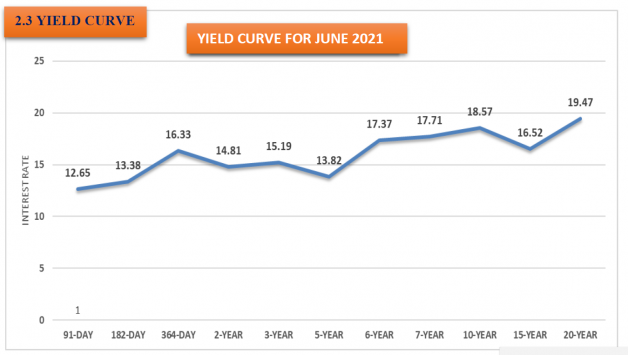

“We have seen a modest upward pressure on domestic debt or bond yields in the past couple of weeks, arising from non-resident investors selling off their Ghana cedi positions. This has also caused a modest weakening of the Ghana cedi, sustaining the upward pressure on yields.”

He added: “We expect investors to start pricing the potentially higher inflation into market valuations. However, with general expectations of still single-digit inflation by year-end, we don’t expect yields to rise sharply”.

Inflation

“Overall, the upward drift in headline inflation appears in line with market expectations, with more increases expected in the second half of the year. However, we still expect to close the year below 10 percent, as the prevailing weak demand will avert the persistence of inflationary pressures,” the economist said.

Other market analysts indicate that the uptick in headline inflation, driven by higher food inflation, confirmed that the favourable base effect experienced in the second quarter has fully worn out. In this light, the market is anticipating that inflation will likely be driven largely by structural and cost-push factors – which signals some upside risk to inflation in the second half of the year.

It is expected that food harvests in the third quarter could cap the upward pressure with a potential decline in the August/September inflation data. However, the unfavourable weather patterns this year could restrain the size of the harvest, thereby preventing a bigger fall in inflation [food inflation] in August or September 2021.

“We are seeing rising production costs, which could be passed on the consumers. Higher fuel costs, transport fares, higher material costs, rising rental costs are all sources of upward pressure to headline inflation. These costs could reverse the decline in non-food inflation and pose an upside risk to headline inflation,” Mr. Martey stated.