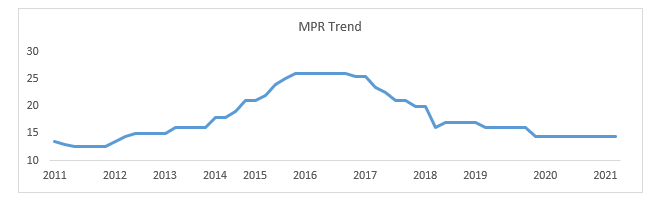

At its recent meeting, the Monetary Policy Committee (MPC) of the Bank of Ghana decided to keep the policy rate at 14.50% for the sixth consecutive time.

The decision normally is a reflection of the Central Bank’s assessment of inflationary pressures, liquidity and growth prospect of the economy. In taking the recent decision, the Committee had another factor to consider; that is the 2021 budget.

This was crucial because government will not expect any decision from the MPC which will dent the “hope” and expected boost to business confidence driven by the budget. It is this sort of thinking that will largely define monetary policy in 2021.

The need for monetary policy to be accommodating especially given the times we are in and the need to implement measures that will revive the economy will be the platform on which this expected relationship will thrive.

Since Ghana recorded its first COVID–19 case in March last year, the Bank of Ghana has implemented many measures to ensure that the financial sector remains sound and in position to support the economy.

Some of these measures include the reduction in the monetary policy rate to 8-year low from 16% to 14.5%, reduction of the reserve requirements from 10% to 8% in order to provide liquidity support to critical sectors; and the reduction in the conservation buffer from 3% to 1.5%, which cuts the capital-adequacy ratio from 13% to 11.5%.

The Bank of Ghana and many analysts believe these measures and others have contributed significantly to provide reliefs during the pandemic hit.

Aided by these containment efforts to mitigate the impact of the COVID-19 pandemic last year, the Ghanaian economy is projected to grow by about 5 percent in 2021.This in many ways indicates that the country has moved on from “saving the situation” policy phase to “stabilization and recovery” phase with different demands on policy makers. The big question from the monetary side will be how Bank of Ghana will play its part in this phase.

A key mandate of Bank of Ghana is “to maintain stability in the general level of prices.” It is also required to “support the general economic policy of Government, promote economic growth and development, and ensure effective and efficient operation of the banking and credit system; and contribute to the promotion and maintenance of financial stability.” In other words, high and sustainable economic growth and low inflation are the two main objectives of monetary policy in Ghana.

This is however not unique to Ghana although the debate about the exact nature of the relationship between inflation and economic growth remains open. Different schools of thought give varying evidence on this relationship. For instance, structuralists believe that inflation is necessary for economic growth, but according to monetarists’ view, inflation is harmful to economic growth.

While the monetarists believe that inflation occur as a result of increases in money supply, structuralists argue that inflation occurs due to institutional or structural impediments or both, which are encountered during phases of rapid growth and development.

In other words, structuralists see inflation as arising from the pressure of economic growth on an underdeveloped social and economic structure, mostly sighting agriculture, foreign trade, and government sectors as suffering from institutional rigidities that cause prices to rise with economic development.

Regardless of the belief or school of thought the MPC members belong to, there will be the need at all times to access the risk to inflation and growth of any policy decision.

The indication so far is that given the fiscal dominance situation in the country, the Bank of Ghana’s policy measures this year may largely be reactionary to fiscal conditions to allow a smooth recovery process.

To this end, it may concern itself with the liquidity requirement of the economy to drive growth. This does not mean that price stability will not be important, but the economy is believed to be operating below capacity.

Therefore, excess liquidity resulting from monetary policy decision should be expected to go into investment to increase output (growth) instead of consumption which will increase demand and drive prices up.

However, a major source of concern to both Bank of Ghana and the Government is the level of the country’s debt stock. Since 2016, the country’s debt stock has increased by about 139% to GHS291.6 billion (76.1% of GDP) at the end of 2020.

In a situation where a large portion of this debt is foreign currency denominated, there is the need to ensure currency market stability to control the debt servicing cost.

This is why it is important for government to continue to create the necessary conditions to improve investment climate.

This will ensure that liquidity due to monetary policy stance does not go into consumption to drive inflation which will have implications for exchange rate, interest rate and limiting monetary policy’s capacity to remain accommodating.

The writer is the Treasurer, FBNBank Ghana Limited