In July 2019, a major policy change in the payments environment was announced by the Namibian central bank. The bank announced after a period of preparation that it had abolished cheques as acceptable payment instruments in Namibia.

In doing so, the bank listed the weaknesses and risks that cheques posed in the Namibian environment and the need to promote more non-paper-based instruments such as payment cards and Electronic Funds Transfer (EFT) (also called Automated Clearing House (ACH) payments.

In December 2020, the South Africa Reserve Bank (SARB) together with the Financial Sector Conduct Authority, the Payments Association of South Africa (PASA) and Banking Association of South Africa followed the Namibian policy and abolished cheques as an acceptable payment instrument in South Africa effective January 1st, 2021. In a consultation paper issued in October 2020, the National Payment System Department of the South African Reserve Bank listed a number of problems with cheque payments as the rationale for the policy, which included the following:

- Prevalence of scams and fraudulent activities such as counterfeiting, forgeries, cheque washing, cheque alterations and closed-account issued cheques

- Increasing cost of cheque processing, as paying by cheque was not only lengthy but also risky due to the multiple stages involved from presentment to clearing

- Lack of innovation in the cheque environment

- Increasing restrictions on the acceptance of cheques within South Africa

- Aging interbank cheque infrastructure

- The effects of COVID-19 in reducing the usage of cheques

Namibia & South Africa have followed a growing number of countries where the usage of cheques as payment instruments have come under scrutiny and/or been abolished altogether. The United Kingdom, for example, considered the phasing-out of cheques in 2018 after a nine-year preparatory period without success.

However, cheques have generally seen gradual death in EU countries such as Germany, Poland, Belgium, the Netherlands, Denmark and the Scandinavian countries. In these countries, the decline and eventual death in cheque usage was facilitated by the availability and promotion of digital alternatives such as Payment Cards and EFTs.

These were considered more efficient, convenient, less risky and faster means of transferring value for both retail and commercial payments. With most businesses publishing their account details on invoices in some of those countries, it became even easier to pay directly into bank accounts electronically rather than by cheque instruments.

This is certainly a major step in the continuous evolution of payments that should engage the thoughts and actions of other countries, especially where the risks and difficulties that informed the Namibian and South African policies are prevalent.

In Ghana, cheques as payment instruments – governed by the Bills of Exchange Act, 1961 (Act 55) – have been around for many years. They have certainly played a major role in the movement toward cashless payments and continue to be the preferred means of non-cash payment for the commercial sector.

Like many systems, cheque processing at the banks and Ghana Clearing House has evolved in sophistication from the introduction of the Magnetic Ink Character Recognition (MICR) characters in 1997 and the image-based processing in 2009. While it is not relatively popular with individual payments, businesses and corporate entities as well as governmental institutions have been the major users of cheques for commercial payments.

The acceptance of cheques was greatly boosted after introduction of the Cheque Codeline Clearing (CCC) system in 2009. This system, which facilitates the clearing of cheques without movement of the physical paper between the presenting and drawer banks, ensured faster clearing of cheques.

The clearing periods essentially reduced to 2 days (t+ 1), and in some cases within the same day (express sessions). Comparatively, this was a great departure from the pre-CCC days when cheques were cleared through the exchange of the paper instruments, and consequently took longer days (between 3 to 9 days depending on the region or clearing zone where the cheque was presented) for value to be given.

However, the risks that necessitated abolishing cheques as acceptable payment instruments in Namibia and South Africa are as applicable to Ghana as they were to the two countries – and indeed all jurisdictions where cheques are still accepted.

In ‘THE 2019 BANKING INDUSTRY FRAUD REPORT’, the Bank of Ghana listed Cheque fraud together with ‘Suppression of Cash/Deposit’ and ‘Forgery and Manipulation of Documentation’ as the only types out of the seven (7) fraud types monitored to have seen increases in volume between 2018 and 2019. The other fraud types, namely Cyber/Email, ATM/POS, Other and Remittance Fraud, decreased in volume over the same period.

As captured in section 3.2 of the report:

“The number of cheque fraud cases increased marginally by 2.56 percent from 39 cases in 2018 to 40 cases in 2019. This includes fraud incurred as a result of cloned cheques, stolen cheque leaflets and cheque alteration. Notable, however, is the increase in number of cases reported as cheque cloning – which originates from the operation of syndicates involving staff of financial institutions, telecommunications companies and cheque-printing houses.”

The case of cheque cloning fraud in particular has been aided by improvements in retail technology that enables fraudsters to reproduce cloned leaflets and forged signatures to near-perfection.

In order to mitigate such fraudulent practices, some banks have had to implement call-back measures for account holders to authenticate cheque payments, thereby incurring additional costs. Even then, this call-back measure has not been fool-proof due to SIM swapping. SIM swapping happens when fraudsters are able to divert calls from the bank to a swapped SIM card of the phone number linked to an account, in order to respond to the bank and impersonate the real account holder during call-back.

Thankfully, Ghana has enough alternative payment instruments that are well-established and able to provide real benefits to the users in terms of speed and convenience without most of the risks identified with cheques. The Ghana Interbank Payment and Settlement Systems Ltd., which runs the CCC clearing house, also manages the Ghana Automated Clearing House (ACH) for electronic funds transaction (EFT) payments. Like the cheque system, all commercial banks in Ghana are also connected to this platform for the exchange of electronic payments among member-banks.

In addition, the Ghana Interbank Payment and Settlement Systems Ltd (GhIPSS) has also introduced the GhIPSS Instant Pay (GIP) platform, which also provides users with the means for real-time transfer of funds instantly to recipients of other member institutions every day of the year. It’s important to note that the membership of GIP extends beyond banks to FinTechs, Mobile Money Operators and other non-bank Financial institutions.

These two platforms are not only good substitutes for cheques but also offer a more efficient and risk-controlled payment options to businesses and other members of the banking public. Most financial institutions have incorporated these payment-types into their various digital channels such as Online Banking, ATMs, Mobile Apps and USSD channels. Some have also enhanced the security of payments by multiple-factor authentication mechanisms (MFA) such as one-time PINs/Passwords and biometrics to generate better assurances of payments.

Additionally, the activities of service providers in the digital payments space have been given a boost through passing of the Payment Systems and Services Act in 2019 (Act 987). The Act has provided the legal and regulatory framework to guide and manage their operations. As a result, additional cashless and dematerialised payment options have been added to the available instruments, which further removes any challenges with the phasing out of cheques.

With the current COVID-19 pandemic, these EFT payment options have been very useful as they have enabled and supported remote payments to support business transactions without physical presence of the parties. These are very much unlike cheque payments, whereby the physical instrument is required to be presented at the bank branch with all the attendant infection transmission risks.

Apart from these EFT payment options, there are also other types – such as card and wallet-based payments from banks and electronic money issuers which have been accepted and seen growth in usage over the last few years. Together with the EFT payments, there are therefore enough digital payment options which provide better alternatives to cheques for payments in Ghana.

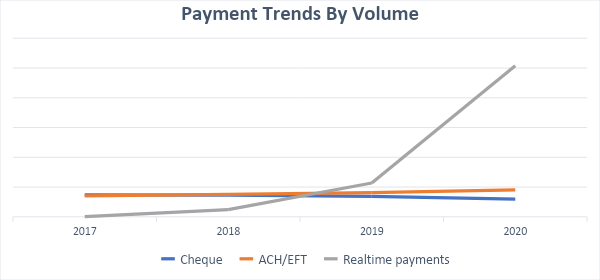

Overall, the usage of cheques has seen a decline in recent times as against other cashless payment alternatives. The graphs below show the trend in the last four years with regard to the comparative volumes of cheque payments against EFT/ACH and Realtime payments that were processed through the Ghana Clearing House operated by the Ghana Interbank Payment and Settlement Systems Ltd. (GhIPSS).

The graph above shows the decline of cheque payments as compared to the significant rise in Realtime payments and the relatively smaller rise in EFT/ACH payments. Realtime payments are the Instant Payments on whose rails mobile money interoperability (MMI) and the GhIPSS instant pay (GIP) transactions are processed.

The graph above also shows the trend for cheques alone over the same period out of the graph above for emphasis

It has to be noted that the payment statistics shown above exclude those of other closed-loop digital payments that do not go through the clearing house and are completed on the same networks of their issuers. Most of these have also seen even more significant increases in both volume and value of transactions (e.g., Mobile Money and other wallet-based payments at agent and merchant points).

Road Map

The recommendation is therefore to migrate Ghana away from cheque payments and towards the other non-paper-based digital instruments. This will ensure that we avoid the increasing risks associated with cheques in the march toward greater cashless payments.

However, a move to sunset cheques as acceptable payment instruments will have to be done in a controlled manner over a period of time in order not to create chaos – especially in the business environment. As was done in the cases of Namibia and South Africa, there should be a clear roadmap with adequate time between promulgation of the policy and its implementation date, to allow all major stakeholders prepare and take the necessary steps toward compliance.

The following measures are some suggested means as part of any road map to implement the policy smoothly.

- Clear timelines

There must be clear timelines set for the policy to take effect. An implementation date (whenever agreed) must be communicated to all stakeholders, including the general public, well in advance. For the purposes of proper implementation, a period of two to five years is recommended.

- Discriminatory measures

It is recommended that systematic measures be implemented over the proposed implementation period to graduate the sun-setting of cheques and thereby move the country along the process. Such measures are to introduce various discriminatory costs/benefits measures as means to guide users toward the non-cheque options by systematically making cheque payments unattractive. Some of these may include:

- Placement of limits on the value of cheque deposit, especially for commercial payments. This will make it inconvenient to receive or demand cheques for payments and drive recipients and payers toward the digital alternatives. There is currently no regulatory limit on cheque values processed through the clearing system except for Bankers Drafts.

- Prohibition of cheque deposits into non-business accounts in the period leading to total abolishment.

- Extension of cheque clearing period. This also implies abolishing the current intra-day clearing of cheques (Express Sessions). As with point (a) above, the aim of this measure is to discourage parties from receiving cheques as it will result in delayed settlement of the funds into their bank accounts

- Imposition of incremental fees in addition to existing cheque clearing fees over the implementation period. The charge can be set to zero and increased over time until the sunset date.

- Reduction in the validity period of cheques, which is currently at 6 months, down to a few weeks over the implementation period.

- Reduction in EFT and non-cheque-based transactions and clearing fees to introduce payment of some arbitrage in favour of the digital alternatives and encourage their use. It is further recommended that the reduced charge should be passed on to customers as benefits so as the encourage them to continue utilising the non-cheque digital options.

- Mandated reduction in digital payment fees across all issuing and processing institutions for the benefit of users.

- Continuous publicity and engagement with the banking public and stakeholders in the cheque processing industry to support and address any pertinent concerns they may have. This will help gain the buy-in of these stakeholders and avoid any resistance which could derail the entire policy, as happened in the United Kingdom when they tried to sunset cheques in 2018.

Change Management and Support

Like any established system, the phasing-out of cheques as acceptable payment instruments will not come without challenges and/or push-back. As stated earlier, cheques have been one of the big and oldest non-cash payment instruments and has become very popular with the business community and for high value commercial payments. There is therefore a strong culture of cheque payments that will need to be managed in any effort to abolish cheque payments.

There are also a number of businesses in the cheque processing industry that will be impacted if cheques are phased out. These include security printing companies that print cheque books for the financial institutions, and vendors of hardware as well as software developers and vendors whose applications are used in cheque processing.

It would therefore be useful to engage with these stakeholders who are most likely to lose out in any policy to sunset cheques, in order to enable them prepare for any negative effects of the policy.

Eye on Cybersecurity

In migrating cheque payments to digital, attention must be placed on cybersecurity concerns to ensure no lapses in security. Even though cheque volumes are much lower compared to the other digital alternatives, they account for very signification values. In 2020, for example, the average value per cheque processed through the Ghana Clearing House approximated GH¢30,000 compared to about GH¢6,000 for EFT/ACH and GH¢300 for the Realtime payments. This underscores the commercial usage of cheques.

Member institutions (banks, FinTechs) will therefore have to take adequate measures to meet all regulatory requirements from the Bank of Ghana regarding cybersecurity – including but not limited to other industry standards such as the Information Security Management Systems (ISMS) and Payment Card Industry Data Security Systems (PCI DSS) for the protection of their payment systems infrastructure and data repositories.

Additionally, member-institutions will need to enhance their Identity and Access Management Systems to protect their own issuing and acquiring systems, communication networks as well as customer’s online access mechanisms. As stated earlier, it is good to note that many of these institutions have already implemented some of the risk mitigation measures to protect and ensure proper authentication of their customers for in-person and online transactions.

However, continuous action will be required to maintain the robustness and resilience of cybersecurity measures against cyber-criminals and developers of malicious code.

Eye on Cash

In advocating for the phasing-out of cheques in Ghana, it must be stated that the efforts to continue the march toward greater cashless payments must be maintained if not intensified. Cash must not be allowed to become the alternative when cheques are phased-out. For this reason, some incremental limits can be placed on cash deposits into third party bank accounts over a prescribed period.

As stated earlier, the Ghanaian payments landscape has available to it enough electronic payment alternatives to replace cheques and even reduce cash payments. However, while it is easy to totally phase-out cheques, cash will always be around as a payment instrument due to the nature of the Ghanaian economy and the significant number of informal actors involved in it.

The key, however, is for the financial regulator and government to put in measures that discourage cash payments in favour of available digital instruments such as EFTs, wallet-based and card payment types.

Cheque payments, on the other hand, can conveniently be phased-out as has been done by other countries – some of whom are here with us in Africa. Payments have evolved significantly across the world, and so have their related instruments. In the era of cryptocurrencies in the mix of digital payment instruments, cheques are fast-becoming archaic. The time has therefore come for Ghana to shed this payment instrument in favour of the available digital options.

>>>The writer is the Head, Payments and Credit Fulfilment, First National Bank Ghana