While in Kumasi High School as a Senior High School student between 2000 and 2003, I used to visit my Uncle (now retired) who worked as the Senior Transport Manager for AngloGold Ashanti. Any time I visited Obuasi, I felt a bit miserable about the low level of development in that gold mining empire.

As one of the top-nine largest gold mines on earth, there was nothing so special to prove this achievement to me except for the school and the hospital; basic necessities remained deployable. Gold mining began at Obuasi Gold Mine more than 112 years ago, in 1897 when it was originally known as the Ashanti Mine.

Somewhere in 2008, AngloGold Ashanti’s land operations, consisting of Obuasi and the Iduapriem Gold Mine, contributed 11% to the company’s annual production. Both mines became part of AngloGold Ashanti when Ashanti Goldfields Corporation with Sam E. Jonah as chairman merged with AngloGold Corporation of South Africa in the 1990s and the rest is history.

For some time now, there have been several social commentators, political analysts on radio and television from both the ruling government (New Patriotic Party) and the opposition (National Democratic Congress) strongly debating about the Agyapa Royalties deal and its related issues.

While I do respect all the opinions, from a neutral point of view, I would like to add my voice to why I strongly support the Agyapa listing and the valuation of Minerals Investment Income Fund (MIIF) in Ghana. Further to the above, I think there has also been a lot of misconception about the entire deal and sharing my views will also bring some clarity to Ghanaians.

Overview of the mining sector

Per data from the Ghana Chamber of Mines, the minerals and mining sector has been the foremost source of direct domestic revenue paid to the Ghana Revenue Authority (GRA). Corporate income tax receipt of mining companies was GH¢969.6million, mineral royalty revenue was GH¢702.4million, employee income tax (pay-as-you-earn) was GH¢487.9million in 2017, compared to GH¢399.9million 2016.

Other forms of taxes collected by the GRA in the mining sector, which are officially classified as self-employed, amounted to GH¢780,000. Overall, the total mining fiscal receipts paid to the GRA increased by 31% year on year, from GH¢1.65billion in 2016 to GH¢2.16billion in 2017. Gold accounts for approximately 97% per cent of all mineral receipts. According to the Minerals Commission, total gold output in Ghana has seen substantial increase year on year.

The mining sector in Ghana has 3 major foreign companies who contribute about 53% of the country`s revenue. This implies that for such concentration risk, should any of the companies find themselves in growth challenges, your guess is as good as mine- the country will face serious revenue shortfalls. The situation is even bleaker if investment dries up, future funds required to maintain the expected royalty payments will suffer.

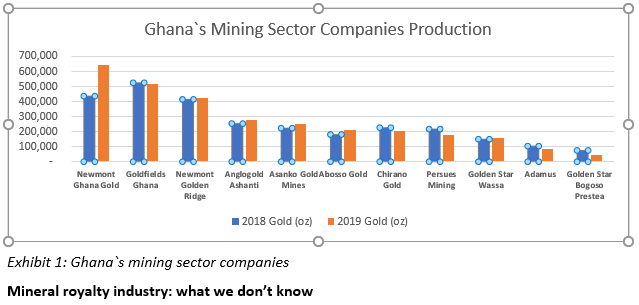

Data sourced shows that Newmont Ghana Gold and Newmont Golden Ridge collectively produce over 1,065k oz of Gold (2018:850k oz) representing 36% of overall productions in the country. Goldfields Ghana and AngloGold Ashanti output for 2019 accounted for 17% and 9% respectively. It therefore even becomes more crucial to focus on various investment to maintain them.

Gold royalties alone paid to government in 2019 stood at US$207million (2007: US$42million) and over the last 10 years, government`s revenue run rate has averaged US$167million.

In my view, these figures are not looking pretty good to the extent that any corrections in gold prices may cause government revenue to drastically decline.

The question a lot of people have asked is that is it possible for gold prices to face any downward pressure? The answer is yes, simply because gold is a commodity and commodity prices go through a cycle. In the next 10-20 years, no one can correctly predict the prices.

Mineral royalty industry: what we don’t know

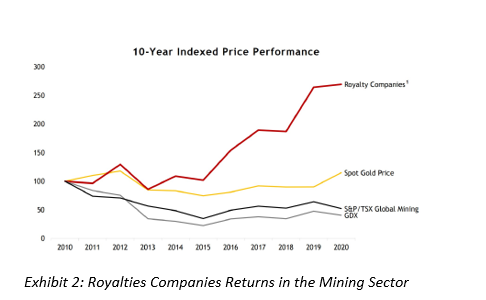

It is estimated that the global royalty sector is about US$72billion (2004: US$2billion) that investors have invested in. Looks attractive, doesn’t it? Over the last 10 years, investments in mineral royalties such as gold have really gained momentum and have even outperformed various underlying metals.

Within the African continents, we have seen countries with gold mines who have done royalties transactions in some United State Royalties Companies. The mineral royalties industry has reached the point where future royalties are used to raise additional funding to invest in the mining operations.

So, the initial Public Offer MIIF wants to raise with Agyapa Royalty is not something new. It`s been tried and tested and the benefits have been tremendous in those countries. Indeed, some of the global mining companies operating in Ghana have leveraged such royalties and that should give discerning Ghanaians some level of comfort. In the case of the Agyapa, MIIF is raising money by using a portion of royalties and setting up joint equity investment where it holds 51% so as to establish majority status and investors holding 49% of the equity. Important to clarify that investors are not buying royalty but rather equity.

Is there not a cause to sustain the gains?

Certainly, there is a cause! The time has now come for Ghana to ring-fence and consolidate our existing gains which will require the need to set up the MIIF to hold mining rights and the royalties, ensure to address price volatility and the necessary investment needs.

Setting up the Special Purpose Vehicle (SPV)

Recall that when Ghana was going through the energy crises which nearly crippled the economy and the banks, the government of Ghana through the Ministry of Finance set up the ESLA PLC through a Special Purpose Vehicle (SPV) mechanism to raise US$10billion on a bond programme to help manage and defray the energy sector crises.

Today, the evidence is clear to see how the energy sector is turning the corner. In the same vein, the Act establishing MIIF creates a company as long as its purposes is to manage funds. AGYAPA SPV in my view will address and better manage the mining royalties.

Good corporate governance instituted

The comfort I get from the Agyapa deal is premised on the fact that, the MIIF has a well constituted corporate governance structure operating within the laws of Ghana with a well constituted board. Those who qualify for appointment as directors under the Companies Act 1963 are legible for appointment.

The Board term is four years and may be re-elected only once. To be gender balanced, three of the seven board members are expected to be women. For such a big venture, an investment committee going through a various rigorous process to engage the services of a professional Asset Management firm is a step in the right direction.

Addressing the offshore registration issues

Undoubtedly, lot of people have expressed sentiments about this Agyapa deal in Ghana, giving it all sorts of descriptions, one of the most talked about issues has to do with the Agyapa royalties registered in UK to meet UK financial reporting and corporate governance structures. That, it is Jersey administered and hence tax haven which government shouldn’t venture.

The question I ask is that, what is the difference between Jersey and Knightsbridge in London, which is an offshore jurisdiction for UK non-residents. I do admit that this may be new for some Ghanaians who are not privy to how offshore entities work, however, I believe that the purpose of the offshore account is to facilitate transactions across borders.

The argument of tax heavens doesn’t hold in the sense that, whenever you list on London or New York Stock Exchange, you are bound by the UK/US reporting and listing rules in that country. For example, if I am an investor in a jurisdiction, I will have to comply with tax authority guidelines in that particular jurisdiction and not evade tax.

To sum up, there are teething issues government may need to address in terms of the issues raised by the Chamber of Mines regarding jurisdiction where proceeds shall be invested, we need to embrace this transaction. We also need to stop comparing equity valuation to royal receivables valuations for investors. The two are mutually exclusive with on cash flows and risk profiles. Let us rather embrace the financing innovations, explore new funding opportunities and make the economy develop.

What is key, is for government to channel the proceeds of the IPO into the productive sectors of the economy to propel investment and consequently support accelerated growth of the Ghanaian economy. God bless Ghana and make our nation great and strong!!!!

Credit: NBOCSI, Lawyer Miriam Amoako

Disclaimer: The views expressed are personal views and doesn’t represent that of the media house or institution the writer works

>>>the writer is a finance and telecom enthusiast, managing local and global Investors, Intermediaries, Banks and Non-Bank Financial Institution relationships with an International Bank in Ghana. Contact: [email protected], Cell: +233-200301110