Covid-19 pandemic has triggered a meltdown of the global economy. Africa has not escaped from the economic crisis as the already gloomy public debt dynamics have been exacerbated by the pandemic. The United Nations Conference on Trade and Development (UNCTAD) has therefore called for a US$2.5 trillion coronavirus crisis package for developing countries[1] while the World Bank and the International Monetary Fund have appealed to creditors to suspend debt payments for low-income countries-to a tune of US $100 billion which translates to about 5.6% of Sub-Saharan Africa’s GDP.[2] Finance Ministers in Africa have projected US$100 billion financing gap to deal with the health and economic shocks.[3]

The aforementioned statistics calls for an immediate international cooperation to deal with the negative impact of Covid-19 on developing countries in general and Africa in particular. Africa’s public debt has been rising steadily since 2013. This is expected to deteriorate further as a result of Covid-19 induced deficit and its accompanying public debt.

Before and After Multilateral Debt Relief & HIPC

Deficit and public debt in themselves are not bad but it is about what the deficit is used for-whether investment or consumption. In mid-2005, G-8 countries proposed to the World Bank, IMF and the African Development Fund (AfDF) to cancel the entire outstanding debt of countries that have reached the completion point of joint IMF-World Bank’s enhanced Initiative for Heavily Indebted Poor Countries (HIPC) of which a number of African countries benefited.[4] The HIPC initiative and the Multilateral Debt Relief Initiative (MDRI) offeredUS$99 billion in debt relief which addressed about 40% of Africa’s total public debt.

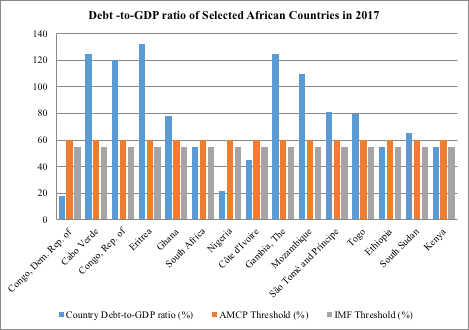

This culminated in a decline in public debt to GDP from 110% in 2001 to 35% in 2012 on the continent. The trend has been reserved since 2013. Public debt to GDP ratio increased from 37% to 56% of GDP between 2012 and 2016. By 2017, twenty four (24) countries on the continent had exceeded the 55% debt-to-GDP ratio recommended by the International Monetary Fund whiles nineteen (19) countries in Africa had surpassed the 60% debt-to-GDP threshold suggested by the African Monetary Co-operation Program (AMCP) for developing economies[5].

Source: International Monetary Fund

In a debt sustainability analysis by World Bank and IMF, the number of countries in distress or at high risk of debt distress rose from 6 in 2013 to 15 in 2019.[6]

Why did Africa get here and how Covid-19 can worsen this position?

In a comprehensive report titled ‘Is sub-Saharan Africa facing another systemic sovereign debt crisis?’ published by Brookings Institution, it chronicles factors that have contributed to the ballooning sovereign debt in Africa.[7] Firstly, Africa’s debt has increased as a result of shocks of the global financial crisis and the 2014 deteriorating terms of trade. Prior to the financial crisis, a number of African countries recorded primary fiscal surplus averaging 3.5% between 2005 and 2008 but this was reversed with the advent of the financial crisis and its accompanying 2014 trade shock. Fiscal surplus averaged 1.6% of GDP through 2013 and further to 3.2% between 2014 and 2017.

African countries are once again facing international trade shocks. Prices of export commodities have fallen drastically as well as volumes. For instance, Nigeria projected to sell 2,000,000 barrels per day, Angola – 1,750,000, Algeria – 1,600,000, Libya – 800,000, Egypt – 700,000, Congo – 350,000 etc this year.[8] These projections have been thrown out of gear as demand for hydrocarbon globally has fallen. Price of crude oil has fallen – expected to average US$35 per barrel as against projected US$65 per barrel in 2020. This scenario is similar to that of other export commodities on the continent as African countries are price takers in international trade. Out rightly, the loss of revenue will widen the deficit and increase public debt. It is time for African countries to rethink resource backed lending as prices of commodities decline.

Secondly, Africa’s public debt has ballooned because of the low global interest rate environment. Creditors and investors in search for high interest have over the years found Africa’s debt to be attractive. The global financial crisis culminated to low interest rate in Europe and United States and has shifted investors’ appetite for Africa’s debt. Since 2006, a number of African countries have issued Eurobonds. Angola, Côte d’Ivoire, Ghana, Kenya, Nigeria, and Senegal have accessed funds from the international capital market. In 2018, African countries floated a US$17 billion in Eurobonds. Just before the Covid-19 pandemic in Africa, Ghana issued a US$3 billion (US$ 1250 bil, 1000 bil, 750 mil at coupon rate of 6.4%, 7.9%, 8.8% for tenor of 7,15 and 41 years respectively).[9] Gabon also issued a US$1 billion bond at a coupon rate of 6.6%. The pandemic has widened the financing gap for African countries but unfortunately, the international capital market is virtually shut because of the pandemic while the interest on such loans will likely be expensive.

Thirdly, public debt has increased significantly because of large financing gaps, particularly for infrastructure. According to the African Development Bank, annual financing gap for the continent stands at US$ 93 billion. Of the total financing needs, African governments financed over 40% of their own infrastructure needs between 2012 and 2016. Over the same period, China financed 15%, much more than the 3% from multilateral development banks. The pandemic has revealed the inadequate investment in health infrastructure on the continent. Government of Ghana for instance has proposed to build 88 district hospitals and 6 regional hospitals. Other African countries will have to invest in infrastructure in the midst of limited resources which has been aggravated by the Covid-19 pandemic. Furthermore, the sizable percentage of external debt to total debt has exposed African countries to volatility of their currencies against other major trading currencies. Covid-19 will continue to negatively affect the trade terms which will trigger depreciation of the local currencies and also impact other macroeconomic indicators.

Way Forward

Prior to the outbreak of Covid-19, amortization of debt and its interest was taking a toll on the finances of African countries and this position is expected to deteriorate with this pandemic. It is time to look within and also push for a change in the rules of engagement with the international community. Domestically, African countries should pursue aggressive revenue mobilization and rationalize expenditure.

They are three major sources of revenue for government-tax revenue, non-tax revenue and grants of which tax revenue is the most predictable. Tax-to-GDP ratio is low on the continent.

According to the 2019 OECD and African Union’s Revenue Statistics in Africa, unweighted average tax-to-GDP ratio for 26 African countries was 17.2%. Nigeria’s tax-to-GDP ratio is 5.7%, Equatorial Guinea-5.9%, Botswana-12.2%, Ghana-14%, Rwanda-16.0%, Morocco-27.6%, South Africa-28.4%, Tunisia- 31.2%, Seychelles-31.5%. This compares to an average of 34.2% in Organisation for Economic Co-operation and Development (OECD) countries[10]. Coulibaly and Gandhi (2018) opined that, efficiency in tax revenue collection could mobilise up to US$110 billion annually over the next five years and reduce the need for debt financing in Africa.[11]Also, governments in Africa should invest in proper accounting systems to generate the needed taxes for development from Multinational Corporations (MNCs).

In Oxfam’s report titled ‘Africa; Rising for the few’, it posits that, in 2010, MNCs avoided paying taxes on US$ 40 billion of income through trade mispricing.[12] With corporate tax rates averaging 28% in Africa, this translates to US$ 11 billion. There should be international cooperation on tax compliance to help African countries generate revenue for development as well as curb illicit financial flows from the continent.

On expenditure, African countries should invest in capital expenditure as recurrent expenditure takes a chunk of expenditure. Investment in viable infrastructure that can pay for itself is a step in the right direction. Countries in Africa devote between 6% -12% of their GDP on infrastructure and this can be increased with the right policies like Public Private Partnership (PPP) and transparent procurement practices.

Covid-19 has taught African countries to look within and trade among themselves. The African Continental Free Trade Area (AfCFTA) was expected to be operationalized in July 2020 but will likely be postponed due to the Covid-19 pandemic. Underlying the free trade agreement is the free movement of goods, services and people which has been partially curtailed because of the health protocols to prevent the spread of the coronavirus. African countries should diversify their exports and trade among themselves post Covid-19.

About the Authors

Emmanuel Amoah-Darkwah is an economist with specialization in economic policy analysis and an ambassador for the United Nations’ Sustainable Development Goals (SDGs). Emmanuel is a highly sought after economic analyst in Ghana and on the international front. He has granted interviews centered on African economies with the BBC, Bloomberg, CGTN, China Africa Project among others.

Alexander Ayertey Odonkor is a chartered financial analyst and a chartered economist with a stellar expertise in the financial services industry in developing economies. Alexander has completed the International Monetary Fund’s (IMF) program on ‘‘Financial Programming and Policies’’ – with a master’s degree in finance and a bachelor’s degree in economics and finance, he also holds postgraduate certificates in entrepreneurship in emerging economies and electronic trading on financial markets from Harvard University and New York Institute of Finance, respectively.

References

[1]United Nations Conference on Trade and Development (2020) “The Covid-19 Shock to Developing Countries: Towards a “whatever it takes” programme for the two-thirds of the world’s population being left behind” https://unctad.org/en/PublicationsLibrary/gds_tdr2019_covid2_en.pdf?user=1653. Accessed 7th May, 2020.

[2]International Monetary Fund (2020) ‘Press Release 20/168’ Available at: https://www.imf.org/en/News/Articles/2020/04/17/pr20168-world-bank-group-and-imf-mobilize-partners-in-the-fight-against-covid-19-in-africa. Accessed 7th May, 2020.

[3]All Africa (2020) African Ministers of Finance – Immediate Call for $100 Billion Supporthttps://allafrica.com/stories/202004010885.html. Accessed 7th May, 2020.

[4]International Monetary Fund (2016) ‘Fact Sheet’ Available at: https://www.imf.org/external/np/exr/facts/pdf/mdri.pdf. Accessed 10th May, 2020.

[5] Chukwuka Onyekwena and Mma Amara Ekeruche (2019) ‘‘Is a debt crisis looming in Africa?’’ Brookings Institution, 10 April [Online]. https://www.brookings.edu/blog/africa-in-focus/2019/04/10/is-a-debt-crisis-looming-in-africa/. Accessed on 25th May, 2020.

[6]World Bank (2019) ‘Addressing Debt Vulnerabilities in IDA Countries: Options for IDA19’http://documents.worldbank.org/curated/en/296411555639304820/pdf/Debt-Vulnerabilities-in-IDA-Countries-Policy-Options-for-IDA19.pdf. Accessed on 10th May, 2020.

[7]Africa Growth Initiative (2019) ‘Is sub-Saharan Africa facing another systemic sovereign debt crisis?’Brookings Institution, Policy Brief. Available at: https://www.brookings.edu/wp-content/uploads/2019/04/africa_sovereign_debt_sustainability.pdf. Accessed on 10th May, 2020.

[8]African Union (2020) ‘Impact of Coronavirus on African Economy’ Available at: https://au.int/sites/default/files/documents/38326-doc-covid-19_impact_on_african_economy.pdf. Accessed on 6th May, 2020.

[9]Citi News Room (2020) ‘Ghana Issues US$3 billion Eurobond’ Available at: https://citinewsroom.com/2020/02/ghana-to-accept-bids-for-3bn-eurobond-today/.Accessed on 10th May, 2020.

[10] African Union and Organisation for Economic Co-operation and Development (2019) ‘Revenue Statistics in Africa’ https://www.oecd.org/tax/tax-policy/brochure-revenue-statistics-africa.pdf. Accessed on 5th May, 2020.

[11] Coulibaly, Brahima and Dhruv Gandhi (2018) “Mobilization of Tax Revenues in Africa: State of Play and Policy Options.” Brookings Institution, Policy Brief. Available at: https://www.brookings.edu/wp-content/uploads/2018/10/Mobilization-of-tax-revenues_20181017.pdf. Accessed on 25th May, 2020.

[12] Oxfam (2019) ‘Africa: Rising for the few’https://www.tralac.org/images/docs/7490/africa-rising-for-the-few-oxfam-june-2015.pdf. Accessed on 6th May, 2020.