By Kwadwo BOATENG (Dr)

Ghana can convert mineral wealth into broad-based prosperity by shifting from raw extraction to value addition, local supplier upgrading, and skills pipeline an execution agenda MDPI can help design, deliver, and independently verify.

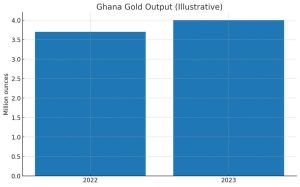

Figure 1: Ghana gold output, 2022–2024

Figure 2: Local value capture, today vs. a five‑year target.

The paradox at the pit and why the next decade must be different

Stand in Tarkwa or Obuasi at daybreak and you’ll see a world-class mining economy in motion: haul trucks rumbling, maintenance teams on shift, and a dense ecosystem of welders, fabricators, and spare-parts traders. Yet too little of the value created by this movement is captured domestically.

Ghana has re-established itself as Africa’s top gold producer and lifted output again—about 4.0 million ounces in 2023 (roughly +8% year-on-year) and a record 4.8 million ounces in 2024, with further growth possible as new capacity ramps. But the structure of value capture still leans heavily toward imported inputs and offshore processing.

That, however, is starting to change. In 2024, Ghana commissioned the Royal Ghana Gold Refinery in Accra with 400 kg/day capacity—an important step toward capturing refining margins and building credibility for bullion produced to international standards (with LBMA certification as the next frontier).

At the same time, Ghana is on the cusp of diversifying beyond gold. The Ewoyaa lithium project secured a mining lease (2023) and an EPA environmental permit (2024); while markets and ratification timelines have stretched schedules, the direction of travel is clear: minerals-to-materials, not rocks-to-ships.

Figure 3: Tarkwa — open‑pit operations and roadside workshop

Where the value leaks—and how big the hole is

Two stubborn leakages keep Ghana from turning mineral endowment into national capability. First, processing and accreditation gaps: without domestic facilities that meet international standards, we ship doré or concentrates and repurchase higher-value products and services. The refinery is a critical anchor—but it must secure market recognition, integrate with transparent sourcing, and be fed by a formalized small-scale channel to work at scale.

Second, traceability and informality: independent analyses estimate Ghana has lost billions of dollars over recent years to smuggled or undeclared gold, with a significant tonnage in 2023 alone not reflected in official flows—value that neither bolsters the cedi nor funds schools and hospitals. Policy steps (e.g., removing withholding taxes that distorted ASM exports) are helping, but the system still needs stronger buy-and-trace architecture across the last mile.

The new opportunity set: from ounces to ecosystems

Mining is a platform industry. Each ounce of bullion has a “shadow” in fabricated steel, sensors, industrial chemicals, metrology, inspection, logistics, and safety systems. When mines source locally, skills and firm capabilities compound. The Ghana Chamber of Mines reports robust local purchases and retentions by member companies—evidence that there is a large, addressable pool to redirect toward Ghanaian suppliers who can meet standards.

The same applies to lithium: Ewoyaa is not just a mine—it’s an on-ramp to battery-materials processing (spodumene concentrate today; higher-value precursors tomorrow) and to process-intensive roles (metallurgy, automation, instrumentation). MIIF’s equity positions in the project are a smart move that helps align state incentives with value addition rather than only royalties.

Policy architecture: local content with teeth—and support

Ghana’s Minerals and Mining (Local Content and Local Participation) Regulations, 2020 (L.I. 2431) provide a strong backbone. They mandate a Local Procurement List, updated over time, specifying goods and services that must be procured in Ghana; they also enable the Minerals Commission to review and deepen local participation.

The Commission’s own notes underscore a reality: mining goods and services spend is enormous; ensuring a larger Ghanaian-owned share is precisely where jobs, productivity and fiscal resilience live.

The implication is not punitive protectionism. It’s performance-based localization: competitive domestic manufacturing and services that meet cost, quality, HSE, and delivery standards—measured transparently.

A five-pillar execution roadmap (and what success looks like)

Pillar A — Beneficiation & processing hubs with accreditation pathways

- Anchor projects: Build on the Royal Ghana Gold Refinery as a hub for assaying, refining, and bullion logistics, with a clear plan for LBMA Good Delivery standards and compliance; publish a public roadmap to accreditation (quality systems, audits, governance).

- Multi-mineral parks: Create co-located processing/beneficiation parks (gold, manganese alloys, lithium concentrate/precursors) with shared labs, industrial water treatment, and power-quality guarantees so SMEs are not priced out by utility CAPEX.

- Feedstock formalization: Integrate ASM traceability and a national gold-purchase mechanism to ensure a steady, transparent supply to the refinery and to banks for reserve operations.

Pillar B — Local Supplier Development (LSD) 2.0

- Tiering & diagnostics: Classify suppliers (Tier-3 to Tier-1) via independent diagnostics covering QA systems (ISO 9001), HSE maturity, delivery reliability, cost control, and traceability.

- Upgrade sprints: Deliver 12–24-week lean/HSE/digital maintenance sprints, followed by capability audits and preferred-supplier listing for mines/OEMs.

- Offtake with performance: Mines and EPCs publish forward procurement plans and commit to floor shares for qualified local tiers on items listed in the Procurement List.

Pillar C — Skills & TVET pipelines for the processing and battery economy

- Role blueprints: Co-design competency frameworks for process metallurgy, industrial chemistry, instrumentation/automation, and safety leadership with mines/OEMs.

- Stackable micro-credentials: 8–12-week modules that stack into diplomas; apprenticeships with logged hours on real equipment (PLC systems, pump/valve maintenance, slurry handling).

- Faculty uplift: Train-the-trainer programs for TVET and university labs; embed industrial projects tied to mine capex timelines (e.g., Ewoyaa pilot units).

Pillar D — Finance that follows capability

- Blended instruments: MIIF and banks co-create supplier upgrade facilities that release capital as SMEs hit audited capability milestones (e.g., ISO certification achieved).

- Pre-shipment & working capital: Mines/OEMs help de-risk PO-backed working capital for local suppliers; interest support tied to on-time, in-spec delivery.

- Equity signals: Extend the MIIF model—small, commercial equity stakes in strategic processing/services providers that unlock bottlenecks (labs, metrology, reagents).

Pillar E — Radical transparency: measure what we train, publish what we source

- Scorecards: A public Mining Value-Add Scorecard updated quarterly: local spend (%), Ghanaian-owned firm share, jobs by skill band, export-grade outputs, ASM formalization metrics, refinery throughput, and a smuggling gap proxy (mirror trade data).

- Independent verification: MDPI serves as a neutral measurer, publishing before/after analyses on cost, quality, and delivery outcomes.

- Open procurement dashboards: Mines publish anonymized, standardized procurement dashboards so suppliers can see pipelines and prepare.

A sector-specific playbook (gold, manganese, lithium)

Gold Priorities: refinery accreditation path; assay and bullion logistics modernization; ASM formalization with competitive buying + transparent taxes to starve smuggling; reagent and consumables localization (e.g., grinding media, HDPE piping, filter cloths) where feasible at scale. Recent and pipeline projects raise throughput and create procurement gravity to justify supplier capex.

Manganese — The long-running Nsuta operations anchor an opportunity in value-added alloys (e.g., ferromanganese, silicomanganese) if energy reliability and emissions standards are addressed. Co-locate power-quality solutions (grid stability, captive renewables + storage) with alloy pilots; pair with skills in furnace operation, refractory management, and environmental controls.

Lithium — Start with disciplined spodumene operations at Ewoyaa, then test pilot-scale precursor production when markets justify. Given price cyclicality and ratification milestones, keep sequencing pragmatically: mine now, learn and bank capability, move up the value chain as contracts and partners allow.

Figure 4: Obuasi gold processing plant at dusk

What MDPI will actually do (beyond training hours)Mine–OEM–SME Value-Chain Labs: Quarterly labs that turn pain points into capability projects (e.g., reduce pump downtime by 30%; localize 40% of instrumentation maintenance).

Modular upgrading: 12–24-week sprints in lean, HSE leadership, digital maintenance, and quality systems with audits at the end; suppliers get capability badges that mines can trust.

Outcome dashboards: Control-group style evaluations that attribute productivity or cost improvements to specific interventions.

Skills pipelines: Co-develop micro-credentials with TVETs/universities and embed apprenticeships tied to capex/commissioning timelines.

Public reporting: With Minerals Commission and the Chamber, co-publish the Mining Value-Add Scorecard and an annual State of Mining Productivity report.

Economics that add up: why value addition improves macro stability

FX and inflation: Import substitution on high-volume consumables and services trims FX outflows; shorter supply chains reduce exposure to global shipping spikes.

Public finance: Reducing the smuggling gap materially lifts non-debt revenue, improves fiscal space, and stabilizes budgets for social services.

Employment quality: Shifting from low-skill extraction to mid/high-skill processing and services raises lifetime earnings and tax bases.

Resilience: Diversified value chains make Ghana less vulnerable to commodity price downturns; in downturns, services and MRO keep activity alive even when capex pauses.

9) Risks and realistic mitigations

Power cost and reliability — Mitigation: park-level power-quality agreements, captive/renewable blends, and time-of-use tariffs for alloy pilots.

Skills bottlenecks Mitigation: bootcamps + apprenticeships with logged hours; international assessor partnerships until local depth grows.

Policy drift or compliance fatigue Mitigation: transparent targets, independent verification, and Procurement List enforcement with disciplined waivers.

Market cyclicality (lithium) Mitigation: phased sequencing, off-take agreements, and hedges; keep the learning curve moving even if capex timings slip.

The first 500 days: a pragmatic action sequence

Day 0–100 — Establish the Value-Add Delivery Unit (Minerals Commission + MDPI + Chamber). Publish the LBMA roadmap and a Q1 Procurement Dashboard. Select two supplier-upgrade cohorts (20 firms) and launch two Value-Chain Labs.

Day 100–250 — Start two processing-park pilots (one metals, one battery materials), focusing on shared labs and utilities. Publish baseline scorecards (local spend %, Ghanaian-owned share, jobs, refinery throughput).

Day 250–400 — Certify the first 10 upgraded suppliers as preferred vendors; add PO-backed working capital lines. Run two skills bootcamps (instrumentation, process control) and place apprentices at operating plants.

Day 400–500 — Public “Year‑1 Value‑Add Review”: document procurement shifts, cost and uptime gains, and smuggling-gap proxy movements; update policy/Procurement List items that under- or over-perform.

How we’ll know we’re winning (KPIs that matter)

- Local spend (%) and Ghanaian-owned share

- Number of Tier‑2/Tier‑1 local suppliers qualified and active

- Average lead times and inventory turns at mines after localization

- Skilled Ghanaian roles filled (metallurgy, instrumentation, automation), with time‑to‑competence metrics

- Refinery throughput and accreditation milestones

- ASM formalization metrics and mirror‑trade smuggling gap

- Export‑grade outputs beyond doré (e.g., manganese alloys, battery precursors)

Why MDPI? Neutral integrator, evidence‑first culture

MDPI’s comparative advantage is execution infrastructure: we convene, upgrade, measure, and publish. We are not a regulator or a lobby; we are the neutral integrator that translates policy intentions (L.I. 2431, Procurement List revisions) into factory‑floor capability and audited outcomes—the kind investors, communities, and editors at B&FT can trust.

The call to action

In the 2010s, Ghana proved it could be Africa’s top producer. In the 2020s, we must prove we can be its top value‑creator. That means accredited refining, disciplined supplier upgrading, skills for the battery economy, and radical transparency.

Mines and OEMs get lower risk and better uptime; SMEs get real contracts; workers get portable skills; the state gets revenue that sticks. MDPI invites partners to sign a National Value‑Add Compact that targets money and metrics so that when a truck leaves the pit tomorrow, a larger share of its value stays Ghanaian.

Dr. Boateng is the Ag. Director of Research and Productivity with the Management Development & Productivity Institute (MDPI) as a Management Consultant, Lead Researcher, and Ai Expert Trainer.

Email: [email protected]