By Joshua Worlasi AMLANU

Investor confidence in the fixed-income market is expected to strengthen further in 2025, driven by declining Treasury bill (T-bill) yields and improving macroeconomic conditions.

This follows a year of gradual recovery in 2024, with government making significant strides in stabilising its fiscal position and rebuilding trust in the domestic bond market.

Databank’s fixed-income market outlook for 2025 projects a continued recovery in the bond market, underpinned by foreign investors’ cautious return and a strategic pivot by government toward longer-dated securities.

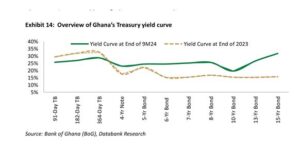

As of last week, yields on Treasury bills continued to inch higher, with the 91-day bill around 27.36 percent. Similarly, the 182-day bill is at 28.1 percent while the 364-day bill stands at 29.88 percent.

The report highlights the importance of T-bill yield compression in facilitating this transition.

“The realisation of our expectation will largely depend on the pace and depth of yield decline across Treasury bills, which continue to offer competitive returns to investors,” Databank noted.

The easing monetary policy stance expected in 2025, coupled with inflationary pressures waning, is likely to create a conducive environment for lowering borrowing costs.

Shift toward longer-term Securities

Government is expected to borrow approximately GH¢200billion from the T-bill market in 2025, a reduction from the estimated GH¢220billion in 2024. This translates to a lower average weekly uptake of GH¢3.9billion compared to GH¢4.2billion in the previous year.

Databank predicts that the reduced reliance on short-term borrowing will be facilitated by improved access to alternative funding sources and sustained recovery in macroeconomic indicators.

Treasury demand for money market funding is expected to decline significantly, allowing for a potential reduction of high T-bill yields. However, this pivot is likely to gain momentum after the first quarter of 2025 due to refinancing needs tied to high T-bill maturities from the latter half of 2024.

Policy measures to compress T-bill yields

Despite a projected dovish monetary policy stance, Databank anticipates that investor response to T-bill yield compression will be delayed until mid-2025. Significant policy measures aimed at reducing sovereign borrowing costs will play a pivotal role in bringing down yields, which currently hover at around 27 percent.

Government has signalled its intention to reduce reliance on money market funding and explore longer-term financing options. These measures, combined with easing inflation and liquidity-enhancing policies – such as reversing increased cash reserve requirements for banks, are expected to create a favourable environment for bond issuances.

Reopening the domestic bond market

Government’s plan to reopen the domestic bond market for non-resident investors as early as 2025 marks a bold step toward accelerating economic recovery. This follows the completion of Ghana’s Domestic Debt Exchange Programme (DDEP) in September 2023.

According to Samuel Arkhurst, Director-Treasury and Debt Management, Ministry of Finance, the reopening aligns with fiscal strategy and signals confidence in the country’s economic prospects.

“The last time we issued a bond was in September 2022, well before the DDEP launch in January 2023. We completed the entire process by September 2023,” Mr. Arkhurst stated in an earlier media briefing.

Typically, countries undergoing debt restructuring take two – four years to regain access to their domestic bond markets. However, Ghana’s near two-year timeline underscores government’s determination to expedite its recovery objectives.

Investor confidence and sovereign ratings

In 2024, the restructuring of Eurobonds contributed to slight improvements in the nation’s sovereign credit ratings – with Fitch upgrading the country to CCC+ and Moody’s to Caa2. These upgrades, coupled with declining inflation and a cumulative 300-basis-point reduction in the monetary policy rate, bolstered investor confidence in government securities.

Money market instruments remained the dominant asset class in the Ghana Fixed Income Market (GFIM) throughout 2024, offering higher returns than longer-dated securities.