…A case for an independent regulator for market conduct

Similar to its counterparts in many other emerging economies, Ghana’s financial sector is critical to the country’s growth since it acts as a vital conduit for the effective distribution of financial resources among economic actors with various spending capacities. The imperatives of trust, justice, and openness loom big in this complex financial ecosystem since they are essential to the sector’s stability and efficiency.

Market Conduct Regulation

The World Bank (2022) defines financial market conduct regulation or financial consumer protection as laws, regulations and institutional arrangements that safeguard consumers in the financial marketplace. It continues in its technical note, June 2019, that effective consumer protection or market conduct regulation should include recourse mechanisms that are accessible, efficient and enable consumers assert their rights to have their complaints addressed in a transparent and just way and within a reasonable timeframe. It serves as a watchdog over consumer interests and a motivator for fostering trust and confidence in financial intermediaries.

Dual Objective of Financial Sector Regulation

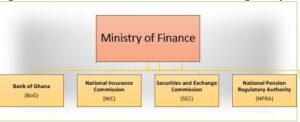

In the context of Ghana, financial regulation has traditionally served the twin goal of promoting the soundness of financial institutions and systems (prudential regulations) and protection of consumers and investors (market conduct regulations). These goals have been the responsibility of Ghana’s financial regulators, including the Bank of Ghana (BoG), National Insurance Commission (NIC), Securities and Exchange Commission (SEC), and National Pensions Regulatory Authority (NPRA).

Similar to the stewards of financial stability, prudential laws are primarily focused on ensuring the strength, stability and resilience of financial institutions. Prudential laws, for instance, can specify capital adequacy standards, ensuring that banks have enough capital on hand to cover any losses and safeguarding the entire financial system. In contrast, market conduct laws and regulations act as consumers’ and investors’ watchdogs, vigilantly protecting them from potential wrongdoing and exploitation by financial intermediaries. Together, these two financial regulation pillars create a strong framework that protects the whole financial system and fosters consumer confidence as well as economic stability.

Figure 1: Ghana’s Current Financial Institutional Regulatory Framework

Source: Author’s design

Concerns with Ghana’s Dual objective of Financial Regulators

Ghana’s Financial Sector has and is still going through some turbulence. Consumers and investors have largely been at the receiving end of incidences of pyramid/Ponzi schemes, collapse of financial institutions etc. leading to considerable drop in consumer confidence and apathy towards financial intermediaries. This has brought the current financial regulatory framework under increased scrutiny for giving prudential concerns excessive weight at the expense of market conduct considerations.

These could partly be attributed to the failure of market conduct regulations in the supervision of financial service providers regarding their competence, integrity of its employees, marketing of financial products and services and fair business practices. In these instances of consumer abuses, regulatory actions have mostly been reactive and in some instances inconclusive.

A Case for an Independent Regulator for Market Conduct (Ghana Financial Markets Conduct Authority (GHAFMCA)

While the conventional or traditional model has made strides in maintaining the safety and soundness of the financial system, the complexity of modern financial markets necessitate specialized oversight in addressing matters of ethics, transparency, fair treatment of consumers, global best practices, market development and conflicting role of dual regulation.

Ghana must therefore think about a different regulatory framework; an alternative model, known as the Twin-Peaks model, which originated in Australia and gained popularity in the UK and South Africa, could help address the shortcomings of the conventional framework. Two regulators are involved in this paradigm, one responsible for prudential regulation and the other for market behaviour. It provides a more balanced strategy that is better able to protect consumer interests while preserving financial stability.

Table 1: Characteristics of traditional and Twin-peaks regulatory models.

| Aspect | Traditional Models | Twin-Peaks Model |

| Regulatory Focus | Prudential Regulation | Prudential and Market Conduct Regulation |

| Regulatory Entities | Single Regulator | Two Separate Regulators |

| Emphasis on Consumer Protection | Limited | High |

| Response to Consumer Abuses | Reactive | Proactive |

| Regulatory Balance | Prudential-oriented | Balanced |

Source: Author’s own construct

The Vital Role of the Ghana Financial Markets Conduct Authority (GHAFMCA)

Given these formidable challenges and regulatory deficiencies, there is an undeniable need for the establishment of an integrated business conduct regulator, the Ghana Financial Markets Conduct Authority (GHAFMCA). Among the many functions, GHAFMCA will relieve the existing institutional regulators of their “dormant” market conduct functions to protect consumers and investors through enhancing financial education and regulations of financial services products and services. Together with the prudential regulators (BoG, NIC, SEC, NPRA), GHAFMCA will be responsible for the licensing of financial institutions by subjecting promoters to fit and proper tests, oversight of governance systems of existing financial intermediaries, promote fair treatment of consumers through an arbitration system. This approach will relieve all existing prudential regulators from their market conduct responsibilities.

The challenges faced by Ghana’s financial regulatory framework demand innovative solutions that prioritize consumer protection and investor confidence. The establishment of GHAFMCA represents a promising step in this direction. By addressing market conduct deficiencies and promoting fairness and transparency, GHAFMCA can serve as a crucial instrument in fostering a robust and responsible financial ecosystem in Ghana. A suggested regulatory framework for Ghana, made up of GHAFMCA, is shown below.

Figure 2: Proposed Regulatory Framework with an independent market conduct regulator.

Source: Author’s design

Conclusion

Financial Consumer protection in Ghana is an indispensable component of the nation’s economic development. The establishment of an independent Market Conduct Regulator, represented by the proposed Ghana Financial Markets Conduct Authority (GHAFMCA), is not only a compelling necessity but also a vital step towards ensuring the highest standards of fairness, transparency, and accountability within the financial markets. By addressing the deficiencies in market conduct regulations and actively safeguarding the interests of consumers and investors, GHAFMCA can rejuvenate confidence in financial intermediaries and promote responsible financial practices. In doing so, Ghana can foster a thriving financial ecosystem that serves as a catalyst for economic growth and prosperity.