Technology has changed the way we handle our money. With technology, we have seamless ways to spend, send, borrow, invest and save money. Although the convenience it brings has associated costs, we are willing to bear them until we feel we are being exploited, at which point we seek out alternatives.

Fintech and Financial Inclusion

Fintech encompasses novel business models and products that leverage technology to provide client-centred financial services in a simplified and easily accessible manner. Financial inclusion is the availability and equality of opportunities to access financial services.

Optimal financial inclusion describes a state where individuals and businesses can access appropriate, affordable, and timely financial products and services. Over the years, this has been sought by governments and private ventures alike. However, in recent times, amongst the numerous users of fintech solutions in Ghana have arisen some who believe service providers may have detracted from the spirit of financial inclusion in the affordability category.

Fintech Channels

A simple approach to view fintech adoption is through the lens of fintech channels. Fintech channels are the various platforms through which people access fintech solutions. Examples are web applications, mobile applications, and unstructured supplementary service data (USSD) which could be considered the most popular channel used in Ghana.

USSD is the technology that brings fintech to the feature phone (popularly known as yam). Accessing fintech through USSD only requires a connection to your telephone company’s (telco’s) network unlike the other channels that require an internet connection in addition.

Fintech Service Providers

With regards to fintech service providers, Ghanaians generally consume fintech services from private fintech companies like Zeepay, expressPay and Hubtel, commercial banks and telcos.

Telcos are arguably the leading fintech service providers in Ghana through mobile money services, while commercial banks leverage their large customer bases to stay in the competition. Today some commercial banks even provide bank-agnostic solutions to customers. Fintechs are not very far behind and continue to innovate to remain a potent threat in the race for the customer.

Each of these groups of service providers leverage at least two of the three channels identified: web applications, mobile applications or USSD. The choice of channel delivery largely depends on their perception of the preference of their target customers.

Service Charges

For the purpose of this analysis, we would focus on instant payment charges since those reflect the most popular fintech services i.e., money transfers and payments. Furthermore, since there is no single platform that has the whole bankable population of Ghana onboarded, cross platform transactions are inevitable. We therefore prioritise cross platform costs. Our analysis of the market play in Ghana is then benchmarked with selected African countries.

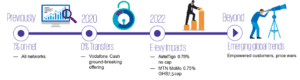

Telcos – Prior to 2020, telcos in Ghana charged a flat rate of 1percent for on-net transfers. However, in 2020, Vodafone made a bold move and announced their cancellation of all transfer charges on their network including transfers to other networks!

When the Government of Ghana introduced the 1.5percent e-levy on electronic transactions in May of 2022, both MTN and AirtelTigo also made efforts to reduce their transfer charges from the previous 1percent flat rate to 0.75percent. MTN also introduced charge-free transfers for up to GH¢100 per day. Furthermore, unlike AirtelTigo, MTN has a GH¢7.5 cap; meaning that on any single transfer, you are charged no more than GH¢7.5 as transfer charges.

It is worthy to note that the free GH¢100 per day on MTN does not apply to cross-network transfers. In fact, cross-network transfers attract a flat rate of GH¢0.381 for transfers of GH¢50 and below. This means that if an MTN mobile money user were to transfer GH¢20 to a Vodafone cash user for lunch, they would be charged GH¢0.38 (1.9percent).

Commercial banks – Today, most commercial banks in Ghana offer a mobile application or at least a USSD application to their customers. Cross platform instant payments here would focus on the Ghana Interbank Payments & Settlement Systems (GhIPSS) Instant Pay service or the bank account to mobile wallet service. Charges associated with using these services vary by bank. However, you would generally see a fee of 1percent with a cap of GH¢5 for GhIPSS Instant Pay.

For bank account to mobile wallet transfers, the charge ranges between 0.75percent to 1percent (depending on the bank) with a cap of GH¢10. Examples of banks at the lower end of the range (0.75percent) are Standard Chartered bank2 and ABSA3 bank. Another below 1percent is Fidelity bank at 0.90percent4, while others like Stanbic Bank5, Ecobank6 and GCB Bank7 charge at 1percent.

GCB bank also provides a bank agnostic USSD product called G-money for which customers of any bank could sign up to. G-money transfers cost 1percent to all networks with a cap of GH¢10 and a floor of GH¢0.507. It is however worthy to note that G-money to G-money transfers are arguably the cheapest amongst charging entities, at a flat GH¢1 for transactions of GH¢100 and above. Meaning, if you were to send GH¢1,000, you would be charged GH¢1 (0.1percent).

GhanaPay is a novel product in Ghana which was recently launched (June 2022). It is a collaborative effort of commercial banks in Ghana under the Ghana Association of Banks (GAB) together with GhIPSS, to provide a bank agnostic mobile wallet service, under the auspices of the Bank of Ghana (BoG)8. A bank account is not a pre-requisite for using the service hence, demonstrates equal opportunity for all in financial inclusion. It supports cross-platform transfers to bank accounts and existing mobile money wallets, all of which are free of charge except for cash-out transactions.

Fintechs – For private fintech companies, charges vary widely. For example, Paystack charges 1.95percent on any transaction (including international transfers) while Slydepay charges 0.8percent with a cap of GH¢5, on transfers to any bank account. In view of this, for benchmarking purposes with other jurisdictions, private fintech companies would be excluded.

Benchmark Analysis

Two countries on the continent would be considered for the analysis. For telco charges, we would focus on Kenya, particularly Safaricom which pioneered mobile money services on the continent with M-Pesa. M-Pesa remains one of the leading mobile money services in Africa. A benchmark of cross-network mobile money charges in Ghana to M-Pesa charges9 is presented below:

Mobile Money Transfer Charges in Kenya vs Ghana

In summary we find that Mpesa is only marginally more expensive than MTN mobile money in Ghana until the higher bands (GH¢671-GH¢1,005 upwards) where the opposite is true. However, there is no cause for comparison with Vodafone Cash which is free.

With regards to commercial bank charges, Nigeria presents an appropriate benchmark country, having a regulator-defined framework for the application of charges on various products and services10. It applies to all financial institutions licensed or regulated by the Central Bank of Nigeria.

Commercial Bank Transfer Charges in Ghana vs Nigeria

In summary we find that GhIPSS Instant Pay is at best 5 times the cost to the consumer as compared to what is charged in Nigeria. However, comparing to GhanaPay which is free then turns the tables in favour of Ghana. It is worthy to note that this analysis does not consider local taxes. For instance, the e-levy in Ghana has not been considered for the benchmark as we are analysing only the original cost of using the service.

Concluding Remarks

There is a continuous strive for financial inclusion in Ghana and while we may still have some way to go, our fintech ecosystem is headed in the right direction. Credence to this is the launch of mobile money interoperability as far back as May 2018, the recent launch of GhanaPay in June 2022 and the realisation of global emerging payment trends like zero rated transfers, just to mention a few. From the analysis presented, Ghana could be considered a leader with reference to cost efficiency in payments and transfers; an attribute of financial inclusion rather than exploitation.

>>>the writer is a Digital Consultant at KPMG where he provides clients with actionable insights for market-leading business outcomes. He is an alumnus of the University of Oxford FinTech Programme and a Professional Scrum Master. He is also a Chartered Accountant with both the ACCA and the ICAG. You could reach Philip on LinkedIn: Philip Twum, ACCA.

NB: The article and research presents the thoughts and opinions of the Author and not his company.

References:

1MoMo Tariffs [online] Available at: https://mtn.com.gh/insight/momo-tariffs/ [Accessed 6 Jun 2022]

2Standard Chartered Bank Service and Price Guide Ghana [online] Available at: https://av.sc.com/gh/content/docs/gh-scb-tariff.pdf [Accessed 6 Jun 2022]

3ABSA Tariff Guide [online] Available at: https://www.absa.com.gh/content/dam/ghana/absa/pdf/tariff-guide/tariff-guide.pdf [Accessed 6 Jun 2022]

4Fidelity Tariff Guide [online] Available at:https://www.fidelitybank.com.gh/doclink/fbgl-tariff-guide-2021/eyJ0eXAiOiJKV1QiLCJhbGciOiJIUzI1NiJ9.eyJzdWIiOiJmYmdsLXRhcmlmZi1ndWlkZS0yMDIxIiwiaWF0IjoxNjIzMjYwMzEzLCJleHAiOjE2MjMzNDY3MTN9.D-tL-wQlCza7LWmPRHA6FV2t_OzYPiuxPOknSmYqLfc [Accessed 6 Jun 2022]

5Stanbic Bank Achiever Banking Pricing 2020 [online] Available at: https://www.stanbicbank.com.gh/static_file/ghana/Downloadable%20Files/Pricing%20Guides/Achiever%20Banking%20Pricing.pdf [Accessed 6 Jun 2022]

6Ecobank Tariff Guide 2020 [online] Available at: https://ecobank.com/upload/publication/20201110014636677A5PG4RAQ2Z/20201110015044940E.pdf [Accessed 6 Jun 2022]

7GCB Tariff Guide [online] Available at: https://www.gcbbank.com.gh/downloads/informational/90-gcb-bank-tariff-guide-2021-reviewed-190821/file [Accessed 6 Jun 2022]

8GhanaPay FAQs [online] Available at: https://www.ghipss.net/index.php/ghanapay [Accessed 6 Aug 2022]

9Safaricom M-pesa – Transfer to other Mobile Money Users [online] Available at: https://www.safaricom.co.ke/personal/m-pesa/getting-started/m-pesa-rates [Accessed 6 Aug 2022]

10The Guide To Charges By Banks, Other Financial And Non-Bank Financial Institutions 2020 [online] Available at: https://www.cbn.gov.ng/out/2019/ccd/guide%20to%20charges%20by%20banks%20other%20financial%20and%20non-financial%20institutions%20eff%20jan%201%202020.pdf [Accessed 6 Aug 2022]