By: Emmanuel Kweku Quansah (Ph.D.), Nathaniel Boso (Ph.D.) & Abdul Samed Muntaka (Ph.D.)

Southampton Solent University (Southampton, UK) and CARISCA Kwame Nkrumah University of Science and Technology (Kumasi, Ghana) and CARISCA

| The LMI value for Ghana for the fourth quarter of 2023 is 63.3. |

The LMI for the fourth quarter of 2023 decreased by 0.4 points to 63.3 from the previous quarter’s 63.7 (third quarter).

Growth is INCREASING AT AN INCREASING RATE for Warehousing Capacity, Warehousing Utilization, Warehousing Prices, Transportation Capacity and Transportation Utilization.

Growth is INCREASING AT A DECREASING RATE for Inventory Levels, Inventory Costs and Transportation Prices.

The fourth quarter 2023 Logistics Managers Index registered a value of 63.3, which is 0.4 points lower than the 63.7 recorded in the third quarter of 2023. The gradual decline from June continues with a slow-but-steady fizzling of economic vibrancy, which began in the first quarter of 2023. The drop is driven by increasing warehousing metrics and increasing transportation metrics (with the exception of transportation prices).

On the other hand, inventory levels (58.25) have declined slightly from the previous 58.85, while inventory cost has also dropped to 79.90 from the previous quarter’s 81.68. It is interesting to note that this quarter has recorded the lowest transportation price metric value, at 88.50, since the inception of the LMI.

Researchers at the Centre for Applied Research and Innovation in Supply Chain – Africa (CARISCA) issued this report today.

The overall LMI score is a combination of eight distinct metrics that make up activities in the logistics sector: inventory levels and costs; warehousing capacity, utilization and prices; and transportation capacity, utilization and prices. A diffusion index, with a range between 1 and 100, is used to calculate the overall LMI. A reading above 50.0 indicates that logistics activities are expanding while a reading below 50.0 reflects a contraction of logistics activities.

The LMI summarizes the responses of supply chain (including operations) managers from multiple industries in Ghana. Data for the fourth quarter was collected from October to December 2023.

REPORT HIGHLIGHTS

- The overall Logistics Managers Index (LMI) for Ghana for the fourth quarter of 2023 stands at 3, down by 0.4 percentage points from the third quarter’s reading of 63.7. This slight decrease can be attributed to the slowed growth of inventory levels, inventory cost and transportation prices.

- All the indicators for the fourth quarter are above the threshold of 50%. Findings from the Q4 survey indicate a slight fall in inventory levels (58.25) in relation to the previous quarter’s (58.85). Traditionally, December is a month of high consumption due to the festive season. Firms that stocked inventory in the third quarter are fulfilling customer orders from this inventory as they look forward to supplies in the new year.

- Logistics cost indicators seem to be stable, with a slight decrease in inventory cost and quite a small but surprising reduction in transportation prices. Warehousing prices appreciated slightly. Altogether, aggregate logistics cost shows a slight decline from the previous quarter.

- Warehouse capacity picked up after a slight decline from the previous quarter as it moved from the previous quarter’s 55.9 to the current quarter’s 59.3. Warehouse utilization has also improved, to 63.84 from the previous quarter’s 60.42.

- Transportation capacity has also improved from 66.32 to 68.77. A similar observation is recorded for transport utilization, which increased from last quarter’s 64.79 to 66.78.

- The growth of logistics activities is expected to be steady in the next 12 months, with a forecast LMI of 64.3. This is slightly lower than projections from the third quarter (65.2). It’s obvious there is still mixed optimism about growth in the Ghanaian economy, especially with respect to logistics activities.

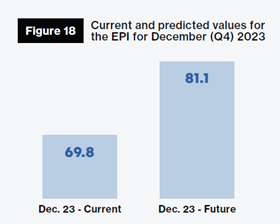

- The Electronic Payment System Index (EPI) declined in the fourth quarter to a value of 69.8 (a decrease of 4.1 from the previous quarter). This value still reflects growth, as it is above the threshold of 50. Usage of electronic payments within the logistics sector is expected to keep growing steadily, as indicated by respondents’ predictions of an increase to 81.1 in the next quarter. The acceleration of fintech is a key government deliverable, and currently mobile money transfers are the leading electronic payment system, promoting financial inclusion in Ghana among businesses and consumers.

WHAT LOGISTICS MANAGERS ARE SAYING – IMPACT OF THE LMI

Since its inception, the Ghana Logistics Managers index has provided valuable insights about the movement of logistics activities within the country, and it has been well received by top managers in many Ghanaian organizations. The LMI respondent list has grown from the initial 130 in Q1 2022 to over 500 in Q4 2023.

Feedback from managers about the impact of the LMI has been very positive. Several managers report using the LMI as an intelligence-gathering tool that enables them to make evidence-based decisions about their operational activities and planning. Many of the organizations that contribute to the LMI survey have begun reviewing the results of the surveys in their meetings, and some have made it a tool for forecast planning.

This fourth-quarter survey gauged policy implications and sought to identify if the LMI reports have contributed to policy change in these organizations. Sixty-two out of 384 respondents (representing 16.15%) were positive of the fact that the LMI had contributed to some form of policy change in their organizations. Most of the confirmed policy changes as a result of insights from the LMI were in the area of inventory control, forecasting, warehousing and pricing.

A few others reported developing procurement policies based on insights from the LMI. For several others that have not introduced a policy change, using the LMI reports and insights as a tool to support decision making has become part of their managerial processes. According to a manager from Voltic Company Limited, one of the leading bottling companies in Ghana, “the Ghana LMI values help us to better plan for the future for our logistics operations.” The general impression is that the trends and projections from the LMI guide a lot of Ghanaian firms in their operational planning.

RESULTS OVERVIEW

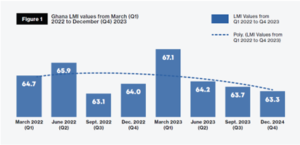

This report presents the results of the December 2023 (Q4) survey, which is the eighth survey carried out since the Ghana LMI’s inception in March 2022. The fourth-quarter results continue to indicate the predictive nature of the LMI in relation to the economy of Ghana as a whole.

In this fourth quarter, the LMI results indicate a drop in overall LMI value from 63.7 to 63.3 (-0.4). Results from the second and third quarters indicated a slowing down of growth, and this slowdown continued in the fourth quarter. Logistics activities are growing (above the 50% threshold) but at a decreasing rate.

In the first two quarters of 2023, GDP growth rebounded to 3.2%, according to the World Bank. This growth was predominantly due to expansion of services (6.3%) and agriculture (6.2%). The industrial sector contracted by 2.2% (with the exception of mining and quarrying).[1] Inflation, largely driven by food prices and transportation, registered at 40.1% in August 2023.

The general World Bank outlook for Ghana in 2023 was that “Ghanaian households have been under pressure from high inflation and slowing economic growth.”[2] However, inflation began to improve late in the year (November – 26.4%, December – 23.2% and January – 23.5%), leading to the lowest rate recorded in 2023, 23.2% in December.

(Source: Ghana Statistical Service)[3]

(Source: Google finance)[4]

The inventory cost metric registered a value of 79.90 (a decrease of 1.78 points from the previous quarter’s 81.68). The fundamental meaning is that goods have become slightly less expensive in the fourth quarter compared to the third quarter. This value is also the lowest for this metric since the inception of the LMI in March 2022. Respondents predict a further shrinking of inventory cost in the next quarter, to a value of 71.87. However, this reduction remains to be actualized. On the other hand, inventory levels are predicted to gain growth to 78.18 in the next quarter. This gain might be plausible, as reports indicate an increase in cargo traffic transiting through the various ports across the country.[5]

Warehousing capacity has risen to 59.28 from last quarter’s 55.87 (an increase of 3.41 points). Warehouse prices have also increased slightly and registered at 77.16, up from last quarter’s 75.60 (+1.56). This metric was in the 80s for five consecutive quarters then dropped to the 70s in the third quarter of 2023. It remained in the 70s in the fourth quarter. Warehousing utilization registered 63.84, an increase from September’s 60.42 (+3.42).

The transportation price metric also registered a lower value of 88.50, 1.81 points lower than that of the previous quarter’s 90.31. In September 2022 (Q3), transportation prices reached their highest value of 97.1. However, in late December 2022 and early January 2023, global fuel prices stabilized, which led to a 15.3% reduction in local public transportation fares.[6] Similarly, in December 2023, a reduction in global fuel prices (oil prices averaged US$78/bbl in December, down from US$94/bbl in September[7]) seems to have had a direct effect on the slowing down of local fuel prices. The transportation capacity index for the fourth quarter increased to 68.77 from 66.32 (+2.45). There was also an increase recorded by the transportation utilization metric, which registered a value of 66.78, slightly higher than the prior quarter’s 64.79 (+1.99).

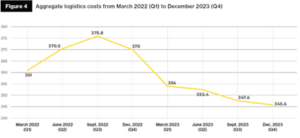

Aggregate Logistics Costs

Figure 4.0 shows the aggregate logistics costs for Ghana in the fourth quarter. The vertical axis of the chart ranges from 0 to 300 because the scores of the three metrics (i.e., inventory costs, warehousing and transportation prices) are aggregated, with 150 representing the midpoint.

The aggregate cost for December 2023 (fourth quarter) in Ghana is down to 245.6, from last September’s 247.6. This metric represents the third consecutive drop in aggregate logistics cost over the last five quarters, with this fourth quarter value being the lowest we have seen. The highest aggregate logistics cost was recorded in September 2022 (275.8). It’s been a good run of slowing growth in logistics cost.

Nevertheless, the current aggregate cost (of 245.6) is relatively high and quite above the mean threshold of 150, implying that the cost of logistics in Ghana is on the high side. It is expected that with inflation showing signs of significant slowdown (inflation was 54.1% in December 2022 and registered at 23.2% in December 2023), the run of decreasing aggregate logistics cost may continue.

FOURTH QUARTER 2023 OBSERVATIONS

Overall LMI

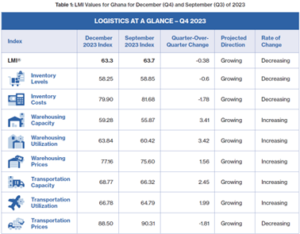

The overall LMI metric for Ghana in the fourth quarter of 2023 has decreased by 0.4 point, registering a value of 63.3 compared to September’s 63.7. This decrease is insignificant taking the overall LMI into consideration. However, there are substantial differences in some of the sub-metrics. This fourth quarter registered drops in inventory levels (-0.38), inventory cost (-1.78) and transportation prices (-1.81).

All other metrics were increasing: warehouse capacity (3.41), warehouse utilization (3.42), warehouse prices (1.56), transportation capacity (2.45) and transportation utilization (1.99). We see a slowing in logistics costs as transportation prices and inventory costs dropped to an all-time low of 88.50 and 79.90 respectively. This led to another all-time low for aggregate logistics cost, which registered at 245.6, a reduction of 2 points from September’s 247.6.

All the LMI metrics for the fourth quarter registered values above the threshold of 50%, which is a clear indication that the Ghana logistics sector is still in growth mode and continues to show promise. Nevertheless, growth has slowed down. The current economic situation in the country is not stable and vibrant enough to generate increasing growth. Inflation has slowed down, however, with a rate in December 2023 of 23.2%. But the cedi continues to struggle against the dollar and currently trades at 12.028 against the dollar.[8]

The index scores for each of the eight components of the Logistics Managers Index, as well as the overall LMI score for the fourth quarter of 2023, are presented in Table 1.0. The transportation price and inventory cost metrics dropped to all-time lows. These two metrics have had the highest values since the inception of the Ghana LMI. The drop in inflation in the country in December is a key factor that has led to the slowing down of these two key logistics cost metrics.

Respondents anticipate that the growth observed in the logistics sector will remain steady in the next 12 months and predict an LMI value of 64.28. This prediction is lower than last quarter’s prediction of 65.21.

Historic Logistics Managers Index Scores

The reading for this quarter along with readings from the last seven quarters of the LMI are presented in table 2.0 below:

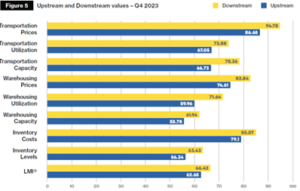

Upstream vs Downstream Activities

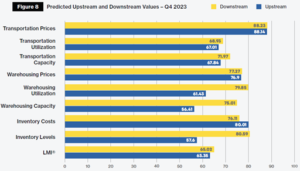

The differences between observations made for firms downstream (reflected by gold bars in figure 5.0) and those upstream (reflected by blue bars in figure 5.0) are insignificant or only marginal. We often expect to see a balance between these two groups. For the fourth quarter, downstream firms reported higher values than upstream firms for all the metrics, which is a first occurrence since the inception of the LMI. Table 3.0 below indicates these values.

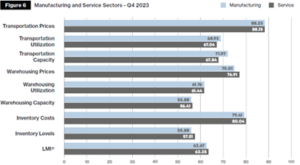

Manufacturing vs Service Sector Activities

Observations were made for manufacturing and service sectors. Manufacturing firms registered higher levels of transportation prices, warehousing utilization, transportation capacity, transportation utilization and transportation prices. The service sector registered higher values for inventory levels, inventory costs, warehousing capacity, and warehousing prices. For the first time, the LMI for the service sector (63.35) was slightly higher than that for the manufacturing sector (62.67) as indicated in figure 6.0 and table 4.0.

PREDICTIONS

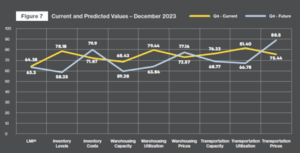

Respondents were asked to predict movement in the overall LMI and individual metrics 12 months from now. The predictions made in December are similar to what we saw in September but slightly less optimistic (as seen in table 5.0). The current LMI value is expected to be steady at 63.3, down by 1.91 from September’s prediction of 65.21.

Similar to the third quarter, respondents expect inventory levels to build up to 78.18. Respondents also anticipate that inventory cost will decrease to 71.87. Warehousing capacity is expected to see growth to 68.42 while warehouse utilization is also expected to increase, to 79.44. The warehouse price metric is predicted to decrease further to 72.57, while transport capacity increases to 76.22.

Respondents expect transport utilization to increase to 81.40, while the transportation price metric is expected to drop to 75.44. The current cost of doing business and the depreciating cedi rate against the dollar provides the context for these predictions. Respondents are hoping that the growth of the cost metrics (inventory cost, transportation price and warehouse price) will slow down over the next 12 months.

Table 5.0 shows the predicted values for all eight metrics from this quarter’s survey (December 2023). Figure 7.0 compares both current and predicted values for December 2023.

Upstream and Downstream (Predicted)

Similar to the main observations, there was no significant difference in the predictions between

downstream (orange bars) and upstream (blue bars) firms. While there is no significant difference, downstream firms expect to see inventory levels continue to build over the next 12 months, more than upstream firms. The same goes for transport prices and transport utilization. Upstream firms, however, expect a greater increase in inventory cost (80.01) than downstream firms (76.11). Downstream firms also predict higher values for inventory cost, warehousing prices, warehousing utilization, and transport capacity than upstream firms, as indicated in table 6.0.

SUPPLY AND DEMAND CHALLENGES: What logistics managers are saying

As part of the study, the views and opinions of logistics managers on factors that affect demand and supply within their various industries were sought. In general, the instability of the cedi against major foreign currencies (especially the dollar) was an issue of concern. According to one respondent from the automobile industry, “The unstable exchange is a major challenge affecting demand and supply.”

The cost of living and inflation were other issues of concern that affect the cost of doing business. Even though inflation came down in December to 23.2 from the previous quarter’s 38.1, it was still considered a recurring issue that contributed to the weakening of the economy.

A respondent from the retail sector stated, “Inflation is quite high and as a result the cost of doing business is also high; the port duties and taxes are also quite high.” Another respondent from the same industry stated, “High taxes and port duties have become burdensome and are quite high. For example, sugar is currently in low supply because it has become more expensive to import.”

The lack of funds and credit opportunities are also key challenges to business operations, according to respondents from multiple industries. The seasonality of demand and supply in some industries was also of concern. Respondents from the agro-industries were much affected by the seasonality of their products as well as cheaper products imported from overseas.

According to one respondent, “The demand for palm oil nationwide is affected by the availability of other seed oils mostly from overseas like sunflower oil and soya bean oil. The more palm oil alternatives on the market, the lower the demand for palm oil and vice versa.”

While the transportation price metric recorded by the LMI is at its lowest (over the past eight quarters), respondents were of the opinion that the cost of transportation is still high. According to a respondent from the manufacturing sector, “The cost of transportation is quite high and this is affecting the demand for products.”

ELECTRONIC PAYMENT SYSTEMS INDEX

The Electronic Payment Systems Index (EPI), introduced in the LMI’s second report, gauges the views of respondents on the usage of electronic payment systems when transacting business with suppliers and customers. Like the LMI, the EPI has a threshold of 50% and is developed as a diffusion index. Respondents were asked about their company’s use of mobile money and e-payment platforms in terms of their decline, steady state or increase. Respondents were also asked about the extent to which their organizations utilize mobile money transactions and e-payment systems when dealing with customers and/or suppliers.

The EPI for the fourth quarter of 2023 registered a value of 69.8 (a decrease of 4.1 from the previous quarter’s value of 73.9), as indicated in figures 18.0 and 19.0.

The general cost of living could be a factor resulting in this decrease in EPI value as well as the levies on mobile money transactions. Respondents, however, predict that the usage of electronic payment systems will grow to a value of 81.1 over the next 12 months (almost the same as last quarter’s prediction 81.4).

The data available shows that the EPI reached an all-time high of 73.9 in September 2023 and seems to be slowing down. The lowest value of the index was in the second quarter of 2023 when it reached a value of 61.0. In general, the EPI results give a positive snapshot of e-payment usage in relation to logistics activities and transactions.

This report is supported by the United States Agency for International Development and created by the Center for Applied Research and Innovation in Supply Chain – Africa (CARISCA), a joint project of Arizona State University and Kwame Nkrumah University of Science and Technology under award number 7200AA20CA00010.