Indigenous lender, GCB Bank, saw its total operating revenue rise to GH¢2.75 billion in the third quarter of 2023 – a 30 percent increase over the GH¢2.1 billion recorded during the comparable period of 2022.

The performance was underpinned by growth across all the key revenue lines, with pre-tax profit during the period under consideration witnessing an 18 percent growth to GH¢832 million on an annual basis.

Speaking during a Facts Behind the Figures session hosted by the Ghana Stock Exchange (GSE), the bank’s Managing Director, Kofi Adomakoh, explained that it was a vindication of the strong fundamentals of the publicly listed bank and the demonstration of successful execution of its strategy to extend its dominance as the market leader.

“The robust set of results that we have delivered is testament to the unique strength of our balance sheet, our large and stable core deposit base and executing effectively key initiatives to drive shareholder value,” he said.

“Our intensified focus on customer experience, investments in our people and digitisation, and a strong focus on transaction banking combined with a relentless focus on cost management will position us to strengthen our balance sheet further and deliver a sustained improvement in profits.

“We will continue to drive effectiveness in sales to increase our client base, grow profit contribution from our Corporate and Commercial business segments, and further grow our market leadership in the retail banking business,” Mr. Adomako added.

Other numbers

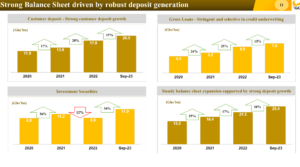

During the period, net interest income and fees & commissions grew by 39 per cent and 11 per cent, respectively, on the back of balance sheet expansion and transaction volume growth.

Furthermore, there was a 9 percent increase in trading income, reaching GH¢ 332 million. Despite the challenging cost environment, which included elevated inflation and exchange rate fluctuations, operating expenses were effectively managed, with a year-on-year (YoY) growth rate of 17 percent.

Consequently, the cost-to-income ratio improved from 54.3 per cent to 50.4. Pre-provision profit was up 50 per cent to close at GH¢1.4 billion, reflecting strong revenue growth and disciplined expense management.

Total assets advanced YoY by 21 percent to GH¢25.4 billion. The growth in assets is largely due to a 15 per cent growth in customer deposits from GH¢ 16.2 billion in the prior year to GH¢ 20.5 billion at the end of September 2023.

GCB’s loan also grew by 13 percent to GH¢ 7.8 billion. Commenting on this development during a high-interest period, when other lenders were recoiling from extending facilities to businesses, a Director and Deputy Managing Director responsible for Finance, Socrates Afram explained that the bank’s position in the national economy means it must continue to lend, albeit cautiously, to drive growth.

“We understand the circumstances that we are in but we cannot sit down and fold our arms. We are a bank and will continue with the core business of banking. We have, however, improved our credit and risk management regime,” he said.

He added that the bank’s total impairment charge stood at GH¢ 536 million is largely attributable to the impairment charge on investments in government securities.

Return on Equity markedly improved from -29.7 per cent in 2022 due to the effect of the Domestic Debt Exchange Program to 34.2 per cent at the end of September 2023. Its share price at the end of the period was GH¢3.5, which Mr. Afram stated was grossly undervalued.

Looking ahead

Mr. Afram acknowledged that GCB’s non-performing loan ratio remained elevated at 20.3 per cent but indicated that measures are in place to lower the metric within the next 12 months.

He also stated that approvals have been reached for the proposed billion capital raise through a rights issue to bolster its capital and improve the capital adequacy ratio, which is currently below the prudential threshold.

GCB remains committed to the Environment, Social, and Governance (ESG) agenda and a robust risk management and compliance culture to deliver sustainable performance and meet stakeholder expectations, its MD added.