Challenges facing the banking sector have taken a toll on businesses, with private sector credit dropping to a four-year low according to Bank of Ghana data.

The banking sector, as revealed by the data, is at a critical juncture; and this unsettling trend, persisting over the past four years, highlights a growing risk aversion among banks – leading to a significant reduction in lending to both businesses and individuals in real terms.

This downturn has been compounded by a series of macroeconomic challenges, including an upswing in non-performing loans and fluctuations in lending rates. While government’s Treasury market has remained a stable haven for investors, the diminishing private sector credit growth raises red flags concerning broader economic implications.

The situation reflects a cautious approach among banks, possibly due to increasing concerns over lending-risks and the need for regulatory and policy interventions.

Private sector credit: a four-year odyssey

Delving into data from 2019 to 2023 reveals the roller-coaster ride of private sector credit (PSC) in Ghana. In 2019, real private sector credit stood at GH¢357.9million – boasting a growth rate of 9.4 percent and constituting 11.3 percent of gross domestic product (GDP).

This proportion remained steady in December 2020 at 11.3 percent of GDP, with a negligible uptick in real PSC to GH¢358.2million and a meagre annual growth of 0.2 percent.

However, a significant setback marked the beginning of 2021 as real PSC plummeted to GH¢351.5million, showing a negative growth rate of negative 3 percent that amounted to 9.9 percent of GDP. This downturn sent a worrying signal of the challenges to come, exacerbated by adverse effects of the COVID-19 pandemic. During this period, banks’ loan loss provisions surged by a staggering 28.0 percent; reflecting the heightened credit risks they grappled with.

The year 2021 concluded with a growth rate of negative 1.3 percent and a real PSC of GH¢458.2million, accounting for 10.5 percent of GDP. The consistency of private sector credit was partially due to the continued implementation of COVID-19 regulatory policy measures, which offered essential support to lending activities and maintained banks’ contribution to the economy.

In 2022 real PSC mounted a recovery – starting at 0.4 percent, equivalent to GH¢457.3million and peaking at 12 percent; the highest growth rate since 2019, equivalent to GH¢504.5million and constituting 12.3 percent of GDP. However, the year ended on a disappointing note with a -14.5 percent contraction in growth; resulting in a real PSC of GH¢391.6million, representing 10.8 percent of GDP.

This decline occurred during a period when consumer inflation soared to a record high of 54.1 percent in December 2022, and the monetary policy rate reached its peak at 27 percent. The banking sector’s performance was closely aligned with existing macroeconomic conditions, as the cost of credit rose due to inflationary pressures and revaluation-driven balance sheet performance.

When comparing the sector’s performance in December 2022 to that of December 2021, a moderation was observed. Several key financial soundness indicators (FSIs) recorded significant declines – underlining challenges faced by the banking sector.

The roots of decline: 2022’s macroeconomic crisis

The rise in the average lending rate was symptomatic of broader macroeconomic challenges. In January 2023, private sector credit showed promise, owing to banks’ portfolio rebalancing and the revaluation effects on foreign currency-denominated credit.

The banking sector’s performance in December 2022, compared to December 2021, mirrored the broader macroeconomic landscape in the country. The rising cost of credit, driven by inflationary pressures and revaluation-driven balance sheet performance, took its toll on the sector. Key financial soundness indicators (FSIs) recorded notable declines during this period, further emphasising the challenges faced by banks.

The promising start and stark reality of 2023

In January 2023 there was a glimmer of hope for the private sector credit market, as it witnessed a pick-up in growth. This can be attributed partly to the portfolio rebalancing efforts of banks and positive revaluation effects on foreign currency-denominated credit. However, when examined in real terms, private sector credit plummeted by 14.5 percent during this period; a stark contrast to the mild 1.3 percent contraction observed over the review period. This dramatic shift reflected the sustained price pressures endured by Ghana’s economy.

As of August 2023, the private sector credit conundrum deepened further with a real PSC growth rate of negative 21 percent, equating to GH¢346.3million and representing 7.6 percent of GDP. This alarming trend points to a cautiously evolving banking environment over the years.

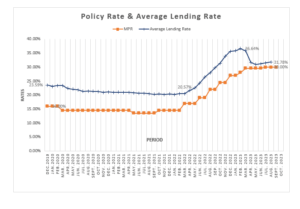

Average lending rates: a balancing act

The interbank weighted average lending rate underwent a roller-coaster ride of its own during this four-year period. It descended from 23.59 percent at the end of December 2019 to 21.10 percent in the same period in 2020, thanks to regulatory forbearance and monetary easing introduced by the Bank of Ghana in response to the COVID-19 pandemic. This decline continued, reaching 20.4 percent in December 2021.

However, as mentioned earlier, the banking sector’s performance closely mirrored macroeconomic conditions. The rising cost of credit due to inflationary pressures and revaluation-driven balance sheet performance led to a sharp increase in the average lending rate. By the end of 2022, it had surged to 35.58 percent from 20.4 percent in the comparable period of 2021. As of August 2023 there was a slight easing, with the average lending rate standing at 31.78 percent.

non-performing loans: a growing concern

One of the most troubling aspects of this trend is an increasing non-performing loans (NPL) ratio within the industry. The NPL ratio surged to 20 percent in August 2023, up from 14.3 percent in August 2022. This spike was primarily attributed to the elevated credit risk stemming from lingering effects of the 2022 macroeconomic crisis. Banks found themselves grappling with the consequences of their risk exposure, leading to reluctance in extending credit to the private sector.

While there was a slight improvement in the NPL ratio between December 2021 and December 2022, dropping from 15.2 percent to 14.8 percent, this improvement may have been a fleeting respite. The overall trajectory suggests a banking sector increasingly troubled by mounting non-performing loans.

Government Treasury market: a safe haven for investors

While the private sector grapples with lending challenges, government’s Treasury market has become a beacon for investors – including banks. Investors consistently oversubscribed, with the Treasury accepting a substantial portion of these subscriptions. The Treasury issued new short-term debts amounting to GH¢13.64billion in the first half of 2023 (H1 2023), while GH¢30.55billion was utilised to refinance maturing debts.

Importantly, the Treasury has exceeded its financing target for H1 2023 by approximately GH¢12.39billion, resulting in a total issuance of GH¢44.19billion during the period out of the GH¢47.30billion tendered by investors.

The refinancing of maturing short-term securities also played a pivotal role in bolstering government’s Treasury market. This trend highlights the shift among investors, including banks, toward government securities as a safe haven in an uncertain lending environment.