The banking sector in Ghana plays a crucial role in shaping the nation’s economic landscape, serving as a fundamental pillar of financial stability and growth. This article provides an insightful overview of the diverse and dynamic Banks in Ghana, examining key aspects that define their operations, impact, and significance within the country.

Spanning a history of several decades, these banks have adapted and evolved to cater to the evolving needs of individuals, businesses, and the broader economy. This overview delves into prominent players such as GCB Bank, Ecobank Ghana, CAL Bank PLC, Standard Chartered Bank Ghana, and others, delving into their financial performance, ratios, and trends over the recent period.

The article assesses critical indicators including Interest Income, Return on Equity, Capital Adequacy Ratios, and Non-performing Loans Ratios to provide a comprehensive understanding of each bank’s financial health and stability. Additionally, it explores their broader contributions to the Ghanaian economy, highlighting their role in fostering financial inclusion, driving economic activities, and catalyzing innovation in banking services.

From the trajectory of Interest Income to the resilience of Capital Adequacy Ratios, this article elucidates the strengths and challenges of Banks in Ghana. By showcasing their pivotal role in economic development and financial progress, readers will gain a holistic perspective of how these institutions shape and influence the financial landscape of Ghana.

Contact Young Investors Network for detailed analysis of each bank.

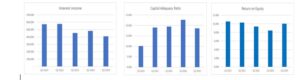

CAL Bank PLC

- Interest Income has shown a consistent upward trend, nearly hitting 40% rise from Q2 2019 to Q2 2023.

- Return on Equity experienced a decline from Q2 2019 to Q2 2020 but rebounded in Q2 2021 and continued to improve.

- Capital Adequacy Ratio remained within regulatory requirement period under review, indicating a strong financial position, though Q2 2023 figure is lower

- Non-performing Loans Ratio has increased from Q2 2020 to Q2 2023, potentially indicating deteriorating asset quality.

GCB BANK

- Net Interest Income has been on a steady rise from Q1 2019 to Q2 2023.

- Return on Assets declined from Q2 2019 to Q2 2020 but has been relatively stable since then.

- Non-performing Loans Ratio decreased from Q2 2021 to Q2 2023, suggesting improved credit quality within the period.

- Core Liquid Assets to Total Assets has remained relatively stable, indicating a consistent liquidity position.

STANDARD CHARTERED BANK GHANA

- Net Interest Income has looked good; Q2 2019 to Q2 2023.

- Return on Equity fluctuated over the years but showed improvement from Q2 2022.

- Capital Adequacy Ratio has consistently exceeded regulatory requirements, indicating a strong capital position.

- Net Interest Margin experienced stability with a slight increase in Q2 2023.

SOCIETE GENERALE GHANA

- Non-performing Loans Ratio has decreased steadily from Q2 2019 to Q2 2022, reflecting improved credit quality. However there was a rise in Q2 2023

- Return on Equity showed a round bottom trend but generally showed strength over the years.

- Net Interest Margin remained relatively stable over the period.

ACCESS BANK (GHANA)

- Net Interest Income displayed steady growth reaching a high in Q2 2023.

- Capital Adequacy Ratio has consistently been above regulatory thresholds.

- Return on Assets hovered between 3.4% to 4.96% from Q2 2020 to Q2 2023.

- Non-performing Loans Ratio decreased from Q2 2022 to Q2 2023, indicating enhanced asset quality.

ADB BANK

- Profit After Income Tax showed significant improvement from Q2 2019 to Q2 2023, however peaking in Q2 2021

- Non-performing Loans Ratio declined from Q2 2019 to Q2 2022, however experiencing a slight jump in Q2 2023.

- Operational Cost-to-Income Ratio decreased in Q2 2021, however began to rise from Q2 2022 to Q2 2023

- Core Liquid Assets to Total Assets experienced fluctuations but generally improved.

ECOBANK

- Net Interest Income more than doubled by Q2 2023 from Q2 2019.

- Return on Equity has been on a descending trend from Q2 2019 to Q2 2023.

- Correspondingly, Return on Assets has also been on a descending trend.

- Non-performing Loans Ratio has remained at acceptable levels compared to its peers, reflecting enhanced credit quality.

REPUBLIC BANK GHANA

- Net Interest Income has been on a steady rise from Q2 2019 to Q2 2023

- Return on Assets and Return on Equity displayed fluctuations but generally improved over the years.

- Non-performing Loans Ratio remained relatively flat between Q2 2019 to Q2 2021 but edged up from Q2 2022 to Q2 2023.

- Capital Adequacy Ratio remained above regulatory thresholds.

Absa Bank Ghana Limited

- Net Interest Income showed growth for the periods under consideration.

- Return on Equity displayed fluxes but improved overall.

- Non-performing Loans Ratio decreased significantly from Q2 2019 to Q2 2020, then began to rise again to Q2 2023.

- Operational Cost-to-Income Ratio experienced fluctuations, however displayed a marked improvement in Q2 2023

BANK OF AFRICA

- Net Interest Income showed growth over the years.

- Return on Equity displayed fluctuations over the period.

- Non-performing Loans Ratio increased significantly in Q2 2023, indicating potential credit quality challenges.

- Core Liquid Assets to Total Assets increased significantly in Q2 2023.

FBN Bank Ghana

- Net Interest Income more than quadrupled from Q2 2019 to Q2 2023

- Return on Equity showed a rounding bottom trend between Q2 2019 and Q2 2023.

- Non-performing Loans Ratio increased significantly in Q2 2023, suggesting potential asset quality challenges.

- Core Liquid Assets to Total Assets remained relatively stable and at appreciable levels.

First Atlantic Bank Limited

- Net Interest Income displayed a steep growth over the years.

- Return on Equity showed fluctuations but improved from Q2 2022.

- Non-performing Loans Ratio decreased significantly from Q2 2019 to Q2 2023.

- Return on Assets improved over the years.

First National Bank Ghana

- Net Interest Income displayed strong growth over the period.

- Despite recording a negative in Q2 2021, Return on Equity improved

- Non-performing Loans Ratio took a huge jump in Q2 2023.

- Capital Adequacy Ratio showed a declining trend though above regulatory threshold

Guaranty Trust Bank Ghana Limited

- Net Interest Income showed steady growth. From Q2 2022 to Q2 2023 was a leap.

- Return on Equity declined sharply from Q2 2019 to Q2 2022, returned higher in Q2 2023.

- Compared to its peers Non-performing Loans Ratio remained at low levels.

- Core Liquid Assets to Total Assets remained steady over the years.

OmniBSIC Bank Ghana Limited

- Net Interest Income displayed growth over the years.

- Return on Equity recorded a negative in Q2 2021 but show good strength to rebound in Q2 2023

- Non-performing Loans Ratio showed a decreasing trend to Q2 2023 from Q2 2020.

- Operational Cost-to-Income Ratio decreased in Q2 2023.

Prudential Bank Limited

- Net Interest Income generally improved quarter on quarter to Q2 2023.

- Return on Equity showed fluctuations hitting a peak in Q2 2022.

- Non-performing Loans Ratio remained relatively stable.

- Return on Assets showed fluctuations.

Stanbic Bank Ghana Limited

- Net Interest Income showed significant growth more than tripled in Q2 2023 from figures recorded Q2 2019.

- Return on Equity showed a strong trend over the years.

- Non-performing Loans Ratio showed fluctuations but surged in Q2 2023.

- Capital Adequacy Ratio remained above regulatory requirements.

United Bank for Africa Ghana Limited

- Net Interest Income showed steady growth.

- Return on Equity improved over the years, though not better than figure recorded in Q2 2019.

- Non-performing Loans Ratio improved through the quarters

- Capital Adequacy Ratio remained above regulatory thresholds.

Universal Merchant Bank Limited

- Total Assets have consistently expanded, indicating its ability to enhance profitability

- Non-performing Loans Ratio remains stable and relatively low compared to peers, reflecting effective credit risk management and loan portfolio quality, however high in Q2 2023.

- Interest Income showed steady growth though lower in Q2 2020

- The Cash Ratio has been consistently strong, demonstrating its ability to cover short-term liabilities with a significant portion of cash and cash equivalents on hand

Zenith Bank Ghana Limited

- Net Interest Income showed steady growth.

- Return on Equity improved over the quarters.

- Non-performing Loans Ratio remained relatively low.

- Capital Adequacy Ratio remained above regulatory thresholds.

Conclusion

In conclusion, the analyzed Ghanaian banks present a mixed landscape of financial performance, with each institution showcasing its unique strengths and challenges. Amidst economic fluctuations and regulatory changes, these banks have demonstrated resilience, adapting their strategies to navigate the dynamic financial environment.

Notably, the impact of the domestic exchange program on profitability has been evident. As the economy and financial markets experienced shifts, some banks harnessed this opportunity to optimize their operations, diversify revenue streams, and enhance customer engagement. This program allowed banks to harness currency fluctuations to their advantage, contributing to improved profitability in some cases.

Despite facing challenges such as changes in interest rates, credit quality fluctuations, and varying macroeconomic conditions, these banks have rebounded through strategic decisions and prudent risk management. Their ability to adapt and innovate has been crucial in sustaining their financial health and capitalizing on opportunities for growth.

Furthermore, the banks’ performance underscores the importance of prudent financial management, risk assessment, and customer-centric strategies. By maintaining adequate capital ratios, managing credit quality, and optimizing operational efficiency, these institutions have positioned themselves to thrive amidst volatility.

As Ghana’s banking sector continues to evolve, these analyses provide valuable insights for stakeholders, regulators, and investors to make informed decisions. With a focus on continuous improvement and strategic adaptation, Ghanaian banks are poised to navigate future challenges and capitalize on emerging opportunities in the dynamic financial landscape.

DATA SOURCES:

GSE, BANK OF GHANA, GHANA STATISTICAL SERVICES

Disclaimer: This document does not constitute an offer to buy or sell any securities, nor is it meant to encourage an offer to do so. It is for EDUCATIONAL PURPOSES ONLY. Before purchasing any security, investors are urged to consult with their respective investment houses for independent advice. This document’s facts and opinions were gathered from or arrived at after doing our best to rely on credible sources. Although great care has been taken in the preparation of this paper, the Young Investors Network, as well as writer, make no guarantees as to the accuracy of the information included within. This report’s conclusions and projections are subject to change after publication at any moment without prior notice.

Young Investors Network (YIN) is a financial education organization with a commitment to educating the youth in financial literacy, business skills and dedicated to preparing generational investors. Its mission is to inspire the youth to be outstanding investors.

Email: [email protected], [email protected]

The writer is with Young Investors Network