Ghana: Demand pressures reverse cedi gains following IMF handout.

South Africa: Inflation eases in South Africa, but remains above the MPC’s target range.

Egypt: Interest rates left unchanged in May 2023.

Kenya: IMF extends financing to ease pressure on government. Uganda: The International Monetary Fund expects Uganda’s economy to grow by 5.5% this year.

Tanzania: Tanzania set to finalize deal on major LNG project.

XOF Region: XOF 3,639 billion of wealth created by the Senegalese industrial sector in 2022.

XAF Region: Cameroon: economic growth expected higher by the end of 2023.

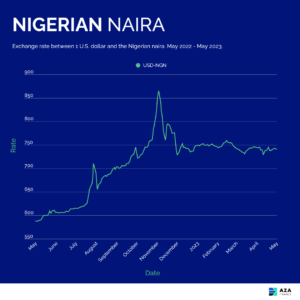

Nigerian Naira (₦)

Compiled by Ikenga Kalu

The naira depreciated sharply over the previous week from USD/NGN 761 to USD/NGN 768 as FX sellers slowed down activities in order to gauge the political atmosphere after the presidential inauguration on May 29, 2023. Nigeria’s GDP growth slowed to 2.31% in the first quarter of 2023 from 3.25% in the fourth quarter of 2022 according to the National Bureau of Statistics. This was mainly attributed to the adverse effects of the cash crunch experienced in the first quarter of the year. On May 22, 2023, Nigeria’s outgoing President Muhammadu Buhari commissioned a 650,000 barrel per day refinery built by the Dangote Group. CEO Aliko Dangote pitched the newly commissioned refinery as a game changer in Nigeria’s downstream oil industry which will double the country’s current refining capacity. Nigeria has struggled to meet its internal demand for refined petrochemicals and has resorted to importing fuel to compensate for the shortfall amid a controversial subsidy scheme. We expect the naira to fall further against the dollar in the coming days building up to the inauguration.

The Ghanaian Cedi traded from 10.75 levels at close of last week to 10.93 levels this week reversing the gains attributed to positive market sentiments with the $3 billion bailout approval by the International Monetary Fund. Uptick demand on the hard currency pushed up the rate as demand for liquidity increased despite the tight supply. On the other hand, the Bank of Ghana maintained its policy rate at 29.5% in the recent Monetary Policy Committee meeting held earlier in the week. It cited easing inflationary pressure in 2023 — 41.7% in April compared to 44.6% in March and 52% in February — as well the relatively stable foreign exchange rates witnessed in the recent weeks. We project sustained pressure on the cedi in the coming days with the spike in hard currency demand.

The rand closed last week’s trading at 19.4235 against the U.S. dollar. It regained some ground early in the week, and as of Wednesday, it is around the 19.20 level.

Inflation data released on Wednesday, showed that April year-on-year inflation has moved down to 6.8% (from 7.1%). While this is an improvement, it is still well outside the South African Reserve Bank’s target range of 3% — 6%. This, in turn, could lead to a further 50 basis point rate hike at the next Monetary Policy Committee meeting.

From a global perspective, the rand continues to remain under pressure due to an underlying global risk off sentiment.

Looking ahead, we can expect the rand to continue trading above the 19.00 level against the dollar. A further decline in global risk sentiment could see the USD/ZAR retest the 19.50 resistance level.

The Egyptian pound is trading slightly weaker against the U.S dollar this week at 30.8955, down 0.17% from Friday’s close of USD/EGP 30.8440.

Last week the Central Bank of Egypt (CBE) left interest rates unchanged as it continued to assess the impact of interest rate hikes earlier this year on inflation and the broader economy. The rates for deposits and lending remain at 18.25% and 19.25% respectively.

The 58th Annual Meetings of the Board of Governors of the African Development Bank is taking place this week with the theme of “Mobilising private sector financing for climate and green growth in Africa.”

Officials from Egypt and Zimbabwe held high level talks to increase trade between the two nations and revamping the Zimbabwean pharmaceutical sector. Zimbabwe is also interested in replicating the success that Egypt has had with its solar projects in line with this year’s theme.

The economic calendar for Egypt remains fairly subdued this week and in the absence of any large economic events the Egyptian pound is expected to remain relatively stable in the week ahead.

The Kenyan shilling dropped this week to a historic low of 137.70 – 138.25 even with the government’s effort to stabilize the economy. The demand for the dollar from sectors such as manufacturing continues to spur the depreciation in the shilling. Government efforts include the agreement between Kenya, Saudi Arabia, and the United Arab Emirates, aimed to provide Kenya with fuel supplies on credit for six months. Additionally, International Monetary Fund staff and Kenya had an agreement to unlock $1 billion of new financing, which could help relieve pressure on government finances, especially the rising debt repayments. Kenya will receive $410 million U.S. dollars once the board approves. We expect to see more pressure on the shilling with increased forex demand as we approach the end of month.

The USD/UGX traded at 3,727.00 on May 24, 2023, up 0.05% from last week’s close. Its value has increased by 1.14% in the last year.

The International Monetary Fund expects Uganda’s economy to grow by 5.5% this year, reflecting a strong half-year performance and some encouraging data from high-frequency activity and confidence indicators. Government bond yields peaked in early 2023 at 12%–15%, resulting in the Ugandan shilling depreciating. This week marks the 58th Annual Meetings of the African Development Bank’s Board of Governors where the goal of the Strategic Water Supply and Sanitation Project (STWSSP) is to support the government of Uganda’s efforts to achieve sustainable provision of safe water and hygienic sanitation for the urban population with improved resilience to the effects of climate change by the year 2030.

Looking ahead, we anticipate that the USD/UGX rate will strengthen by the end of this week due to the increase in economic activity in both the private and public sector and the positive move forward at the 58th Annual Meetings of the African Development Bank’s Board of Governors

Last week, USD/TZS closed at 2,358 but hit its weakest level since March 2019 against the U.S. dollar on Thursday at USD/TZS 2,360. The Tanzanian shilling has weakened even further this week and its mid-market rate is currently at 2,364 against the U.S. dollar. Bid and offer rates are currently at USD/TZS 2,314.52 and 2,407.41 respectively.

Last Friday, May 19, 2023, the Tanzanian government agreed a deal with three major oil companies regarding a liquefied natural gas (LNG) export terminal which is to be developed in the country. The development is subject to legalities and costs however, it is a huge step forward for this project which has been ongoing since 2014.

We expect the Tanzanian shilling to weaken further as the risk sentiment of investors veers towards a risk off approach ahead of the debt ceiling decisions to be made in the United States. We expect the shilling to weaken further past its current weakest level and trade around USD/TZS 2,365 in the week ahead.

Senegal published on May 20, 2023, the industrial sector performance achieved in 2022.

The contribution of the industrial sector to the economy revealed that the value added was established at XOF 3,639 billion, i.e. XOF 401 million more than in 2021 representing 20% of GDP.

Composed mainly of SMEs (92.5%), the industrial park is dominated by agri-food (63%), mechanics and metallurgy (10%), wood and printing (9%) and generates nearly 121,000 jobs.

Ranked as the fifth industrialized country in Africa at the Niamey summit, Senegal’s industrialization strategy is showing significant results.

Economic activity in Cameroon is expected to increase by the end of 2023.

According to IMF forecasts, economic growth is expected to reach 4% compared to 3.7% in 2022. Inflation is expected to fall from 7.3% in 2022 to 5.9% in 2023.

This performance is the result of the tightening of monetary policy and IMF support to correct budget deficits.

By Ama Kudom-Agyemang

The Second African Conference on Agricultural Technologies (ACAT2025) has taken place in Kigali, Rwanda, reigniting a sense of purpose – that Africa’s...