The US government this week pledged $55bn to Africa over the next three years as the Biden administration seeks to strengthen US-Africa relations and boost cooperation on shared global priorities. At the US-Africa Leaders Summit in Washington, the US government sought to convince African countries that its aid and development plan is the most reliable internationally in the long term. Africa has felt the impact of Russia’s war in Ukraine through supply chain disruptions including fertiliser shortages, causing food insecurity and damaging the continent’s agricultural industry. Biden is also said to be backing the African Union’s bid to become a permanent member of the G20. Improved US-Africa cooperation could help to drive increased FX inflows in the long run and give much needed support to African currencies.

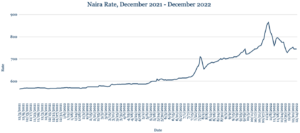

New Naira notes trigger temporary boost

The Naira strengthened against the dollar, trading at 745 from 750 at last week’s close as the country’s bureau de change outlets lowered rates in a bid to attract dollar buyers ahead of the release of newly redesigned Naira notes that went into circulation this week. Longer term, the currency remains challenged by falling FX reserves. While Nigeria ranks among Africa’s top three recipients of diaspora remittances, as we head into the final weeks of 2022, we expect the Naira to come under renewed pressure, with traders seeking to close out year-end requirements boosting FX demand. Going into 2023, we expect further depreciation for the Naira amid limits to US dollar sales to banks, the CBN’s push to align official rates with market realities and Presidential elections scheduled for late February.

IMF bailout resuscitates Cedi amid 50% inflation

The Cedi made significant gains against the dollar, trading at 12.10 from 13.05 at last week’s close after Ghana reached a staff-level agreement with the IMF on economic policies and reforms that will unlock a $3bn bailout loan. The IMF programme aims to restore macroeconomic stability and improve the country’s debt sustainability. Ghana’s external bonds rallied in response, with the yield on its benchmark 10-year bond falling by 121 basis points to 28.25%, according to Bloomberg. The prospect of the IMF deal allowed the Cedi to shrug off a surge in annual inflation, hitting 50.3% in November from 40.4% a month earlier, driven higher by rising transport prices, which increased by 61.3%. With the IMF’s bailout a step closer, we expect the Cedi to make further gains before the end of the year as diaspora inflows increase over the festive period.

Ramaphosa reprieve keeps Rand on front foot

The Rand strengthened 17.19 per dollar from 17.35 at last week’s close as President Cyril Ramaphosa survived an impeachment investigation vote related to the Phala Phala Farmgate scandal. Embattled South African power company Eskom saw its CEO Andre de Ruyter announce his departure this week as the utility’s ageing infrastructure combined with a sabotage crisis has led to a record number of blackouts. With the US Federal Reserve lifting rates by 50 basis points—in line with market expectations—the Rand is likely to continue trading with a 17 handle or stronger as we head into the new year. For 2023, we expect the Rand to perform better than in 2022 as the US Federal Reserve slows its pace of interest rate hikes, while the SARB has scope to further increase rates at home.

Record low Egypt Pound set to fall amid IMF package

The Pound hit a fresh record low of 24.66 on Monday, from 24.60 at last week’s close, before easing slightly to 24.64. The currency’s weakness is driving Egyptians to protect their savings by buying gold, with local prices surging, exacerbated by the government placing a cap on imports of ‘luxury items’ including gold. Egypt is awaiting final approval for an extended IMF package, with the first tranche of the $750 million loan facility expected this month, subject to ratification at an IMF executive level board meeting Dec. 16. We expect the Pound to continue weakening beyond the 24.80 level amid a shortage of dollars and continued reliance on imports such as wheat.

Fitch downgrade for Kenya pushes Shilling to new low

The Shilling slumped to a fresh low against the dollar, trading at 122.75/122.95 from 122.50/122.70 at last week’s close. Fitch Ratings cut Kenya’s credit rating one level to B from B+, five notches below investment grade, citing persistent twin fiscal and external deficits, relatively high debt, and deteriorating liquidity, combined with high external financing costs that limit the country’s access to international capital markets. We expect to see slight pressure on the Shilling in the weeks ahead as dollar demand from importers increases to cover Christmas and year-end orders.

Ugandan Shilling strengthens as inflation eases

The Shilling strengthened against the dollar, trading at 3660 from 3685 at last week’s close. Uganda’s annual inflation eased marginally to 10.6% in November from 10.7% in October, though it remains close to the highest level in 10 years. The pace of inflation is likely to slow next year, averaging between 6% and 8%, before stabilising around the 5% target, according to the Bank of Uganda. The central bank has kept its benchmark interest rate at 10%, despite cautioning that the inflation trend remains uncertain given potential fluctuations in commodity prices. With steady improvement of business activity, we expect the Shilling to continue strengthening against the dollar in the near term.

Tanzanian Shilling supported by agriculture boost

The Shilling gained marginally against the dollar, trading at 2333 from 2334 at last week’s close. A fall in Tanzanian treasury bond prices saw the latest issue oversubscribed by 62% as the central bank sold TZS136bn with a 12.10% interest rate. The higher yields should entice investors, which will support the central bank’s efforts to reduce liquidity in the economy to help ease inflationary pressures. Annual inflation remained at a five-year high of 4.9% in November, while FX reserves hit a five-year low of $4.6bn, enough for 4.2 months import cover. We expect the Shilling to remain stable in the coming week, supported by inflows from investors and agricultural exports, including coffee, cashew nuts, sisal, horticulture and tobacco, which have been helped by a government focus on increasing productivity and efficiency in the agriculture sector.

Issued by AZA. This Newsletter is produced as a service to our clients. It is prepared by our dealing professionals and is based on their understanding and interpretation of market events. AZA cannot be held responsible for any losses of whatever nature sustained as a result of action taken based on comments contained in this publication.