We have heard from Parliament, we have heard from former president Mahama, and we have heard from the President. What we have right now is a Byzantine Generals problem, where half the generals want one course of action and the other half want an opposite course but the people in the castle under siege do not know who wants what. The way you solve the Byzantine Generals problem is to agree on the rules, commit to transparency for all, and establish consensus.

We all have families, and we can all identify with what happens when you extend your family’s expenses and must go to borrow money from neighbours or a bank. There is nothing wrong with borrowing to invest. However, when you are at a point when you are living beyond your means and spending a major part of your earnings on interest payments and living from day to day, then you know you have managed your affairs poorly. When the heatwave comes, that will be the day your air conditioner malfunctions, and you find out how badly you have managed your affairs.

Unfortunately, the Ghanaian economy has malfunctioned badly.

That is where we find ourselves as a country today. Being forced to go to the IMF to seek help does not happen by accident. While the IMF can certainly provide financial support, it is the discipline of decision-making that makes the IMF effective at what it does. Unfortunately, that is the discipline we lack in this country.

We all know there are several issues; fixing the constitution, fixing the SHS problem, and fixing the myriad of problems we have. However, in the next few paragraphs, let me focus on two broad significant areas where we can forge consensus and move quickly to do something in the next few months to build confidence in our people.

Crisis just do not happen suddenly. Much like a fallen tree, it happens slowly, and over time, with every poor subsequent decision, value is destroyed until eventual economic collapse. It is not by accident that we cannot account for the approximately GHS 25billion (per IMF data) in Covid funds provided to the country by the World Bank and other partners. It is also not by accident that we are facing a projected debt of US$12billion owed to the IPPs (Independent Power Producers) by 2023, per the Energy Sector Recovery Program (ESRP). Additionally, it is not by accident that we spend over 50% of our revenues on paying interest on debt. Finally, it is also not by accident that an E-Levy revenue generating solution that was forced as a panacea to our economic problems failed to garner even a quarter of the projected revenue.

We are facing a systemic problem brought on by insular decision-making that is fraught with partisan politics and a failure to tap into the vast talent of competent Ghanaian citizens across the globe who could have helped manage our economy better. We have been to the IMF 17 times, and I do not know why any of us think the country will not be back after another restructuring program. There is a problem with governing and decision-making that has finally caught up with us. I want to propose two broad areas that could form the basis of confidence-building steps that could help us begin a process of finding a consensus towards changing how we manage our economy to prevent a catastrophe next time there is a global crisis.

So, how are we going to manage our current crisis beyond the obvious fact that the IMF is going to force us to get fiscally disciplined in our affairs?

Maybe we freeze our debts at current levels and grow our exports by double digits for the next decade. Unfortunately, it is not as simple as the father of the house taking on more than 2 jobs to get the family’s finances sorted.

We cannot afford or even tolerate a habit of always borrowing or expecting foreign exchange inflows just to prop up the Cedi. We need to restructure the economy to promote exports, we need a radical re-architecting of our approach to managing our economy and re-creating a new cultural philosophy around how we approach our collective discourse around issues of public interest.

Time to enact a debt limit or debt-ceiling legislation

Abraham Lincoln once said that “no matter how tall your father is, you still have to do your own growing”. The implication being that every person grows differently, at their own pace and within their own capacity. Over our history, we have never had an appreciation for what our sustainable growth rate is and hence we have also always misjudged the level of resources to put towards our development. Naturally, without consistent development agenda taken from government to government and party to party, we have miserably wasted resources with a lot of white-elephant projects to show for it, aside from the corruption that dogs every government in power.

We have overspent on roadways, hospitals, airports, and a slew of infrastructure projects for two apparent reasons; 1) every project has been an opportunity for governing party actors to pilfer and 2) every project has been done as if to advertise for the political party in power and hence has totally been unfit for our growth stage. We cannot afford to use political party manifestos as a substitute for multi-year economic development plan, which, unfortunately, is what has happened.

It is time for us to come together to implement a debt management policy that puts in place a debt ceiling law commensurate with the growth agenda that will support sustainable debt levels irrespective of the party in power. That is just a responsible and prudent thing to do.

A debt ceiling can then come up for renewal every 2 years and allow the government of the day to make a case for a debt ceiling level to be raised. As part of seeking approval for an increase, there should be a process to report on all uncompleted government projects in the country and a justification process to support decisions to rationalize every project to free up unused and unspent funds before any debt-ceiling is raised.

The second constraint that should be codified is how the government borrows from Bank of Ghana (BoG). If you look at the past 15 years, you will notice a downward trend in credit and capital to the private sector as a consequence of government’s increased borrowing in the economy. Any debt ceiling law should include a requirement to allow government to borrow from the central bank only within a fiscal year, meaning very short-term loans that will be bridge loans to support government operations.

In the absence of approval or until a renewal comes up, a government then should focus on defunding unprofitable initiatives and manage resources appropriately to make sure debt growth is not driven by the recklessness of any party to enrich itself at the expense of future generations. I have looked at 30 years of Ghana’s economic performance and it is feasible to grow sustainably at a debt-to-GDP ratio of between 35-45%.

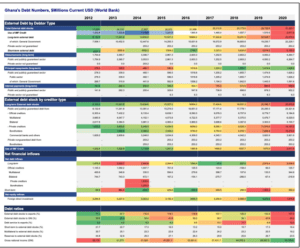

Let me use the following 3 graphs to illustrate the structural problem we have and the opportunity we are missing by not focusing on fixing that structural problem.

We have a persistent external deficit, coupled with an inordinately high debt servicing and that has gotten us into a borrowing to fund both external and internal deficits.

Unfortunately, our net financial and capital account (yellow in the graph above) has been inconsequential in helping support the economy, largely because there is so much being repatriated and, I suspect, so much adverse arrangements that impacts our capital account.

The resulting borrowings, both external and domestic, has consequences for our own domestic private mentor and its capacity to export.

It is obvious that the private sector has been crowded out, showing the massive drop in lending to the private sector. That is a fundamental problem we cannot tolerate because of its knock-on effects throughout the economy and its implications for job creation for Ghanaians.

Now, look at the level of imports and exports since 2011, the graph above. Imports as a percentage of GDP has actually come down and absolute dollars, has been pretty steady. Unfortunately, exports have also been pretty tame over that period and is not growing at the level that it can make a dent in the external balance.

That is not surprising because the private sector, which is the engine of growth for exports, is being starved by governments massive borrowing. Why do we have to even depend on a borrowing event by Cocobod as a funding mechanism for the economy?

If we were to restructure Cocobod as a regulator and liberalize Cocoa exports for private actors, maybe we would have more profitable companies who can increase our export capacity on Cocoa and its related products and take out the burden of having to use Cocobod as a mechanism to earn foreign exchange. The chart above shows how we have managed our persistent external deficit and additionally fund our persistent budget deficits. We borrow and manage our Liabilities till the next borrowing, with an eye on propping up the Cedi. Of course, the spread or borrowing costs kept going up on subsequent borrowings till the global crisis happened and we could not borrow because our structural problem caught up with us. We need to establish fiscal discipline with a legislated, well thought-out debt ceiling rule for governing. We cannot and should never make propping up the Cedi an economic goal. We have done it in the past and it has resulted in two unpleasant re-denominations in our history. Do we want to attempt a third one?

Fixing how economic decision-making happens

We chose to create our central bank around the British model instead of the American model. The British approach has not been beneficial to us and has allowed our central bank – BoG – to be politicized throughout our history. BoG today struggles to be independent or is always in constant angst over its mandate. Over the past 15 years, the board of the BoG have been filled with political appointees and has gotten so bad that you currently have individuals without the requisite experience sitting on the board. How do you get an employee of a foreign company appointed to a sovereign central bank board? When the governor and BoG management bring economic data to help decision making in the economy, what do we expect the outcomes to be?

Political appointments with party affiliation allowing people without requisite experience to end up on the board, is destroying effective decision-making at that level. As Lee Kwan Yew, the eminent founder of Singapore said – “If you do not get your best people into government, and you try to get government on the cheap with political appointments, you will be sorry one day”. Let us take politics out of the Bank of Ghana and its economic mandate and come up with a different process to nominate our best in economics, banking, and finance onto the BoG board.

With a focus on accelerating exports and accelerating credit and capital into the private sector across the country, we may also consider scraping the BoG board, dividing the country into 3 or 4 logical economic growth hubs overseen by a board of governors, headed by the governor. What that will do is get economic activities monitoring and decision-making closer to where production for exports is happening. Why should anyone sit in Accra and make decisions about what happens around Techiman?

The Presidency needs a Council of Economic Advisors, predominantly independent advisors drawn from experienced Ghanaians in the field of finance and economics, with a mechanism to tap into emerging narratives about our economy and advise the presidency appropriately. I believe the presidency can find the best of our people in finance and economics across the world. What is needed is to adopt the best practice in well-managed economies by setting up a Council of Economic Advisers, drawn from Ghanaians with practical experience in economics and finance, and enough career experience to have created beneficial relationships with global economic actors who are of benefit to our future.

There are many Ghanaians who have risen up in their careers to the managing director level and have managed hundreds, if not thousands of people, who can bring incredible value to the country with both their practical experience and relationships across the globe. The Council of Economic Advisors can then run the Economic Management Team with the Vice President and allow for occasional participation of sector ministers as needed. The same Council of Economic Advisors can be supported by a revamped NDPC (National Development & Planning Commission). The NDPC itself needs to be made more of an implementation outfit, restructured, and find a Ghanaian with experience being a chief executive in the private sector, someone who has managed thousands of people and able to operationalize an organization willing to recruit the best of our people across the globe. Also, the current composition of the Economic Management Team dominated by ministers and deputy ministers representing their ministers is not fit for purpose. Our immediate challenge is to improve the quality of our decision-making throughout the economy to prevent this recurring crisis.

Our persistent fiscal deficit is a main driver of our current crisis. When financing stops for a leveraged economy such as ours, a policy of over borrowing invariably ends in a foreign exchange crisis and massive devaluation. We have lived this before in the 90s which led to debt forgiveness so I’m not sure why it happened again other than the simple reason that there are serious lapses in areas of economic decision-making.

However, to bring our fiscal deficit to a sustainable level, probably less than 2.0% of GDP, we need to at least demonstrate a serious commitment to controlling costs and prioritizing what gets funded. Currently government is spending a whopping $5.1billion on total compensation for public sector employees and about another $4.5billion on interest payments per data we reported to the World Bank. That is a total of about $10billion out of the $12billion in revenue coming to government. That is a crisis that could only have happened because of a chain of problematic economic decisions taken over the years.

We need to reduce the size of government. A step in the right direction in the next few weeks and months to right the ship will be to take out some obvious costs out of government budget. Here are a few I can think of, aside from the obvious one that the number of ministries need to be reduced: dissolve the Youth Start program and dissolve NABCO (National Builders Corps). The objectives of these two organizations can be easily addressed by the National Service Scheme working with the private sector without the unnecessary additional costs and encumbrance on the private sector that creates the jobs for our youth. Next, dissolve the National Entrepreneurship Innovation Program (NEIP) – the private sector and a myriad of entrepreneurship centers in the country have been more effective at doing what NEIP was intended to do. NEIP is an unnecessary cost.

Then there is the bigger issue of the SHS cost burden, which could be addressed sooner only if we could make it an issue of reaching consensus on a sustainable way to fund the objectives of free SHS.

From where we sit today engaging with the IMF, we have a Byzantine Generals problem. The way you solve the Byzantine Generals problem is to agree on the rules, commit to transparency for all and establish consensus by focusing on the key guardrails to make sure we do not repeat this ever again. The economic crises we find ourselves in, needs expert hands and critical thinking because if not managed properly, a decade of wealth creation could be lost. The sooner we make some changes to credibly demonstrate our seriousness to problem-solving, the sooner our external partners will support our efforts to develop. Let us not miss the opportunity.

Hene Aku Kwapong is managing partner at Songhai, sits on the boards of Ecobank Ghana and Park Street in Denmark, a Fellow at CDD Ghana, and assistant professor at the Malcolm Baldrige School of Business.

Neenyi Ayirebi-Acquah is a Policy Analyst and Technical Consultant at the Africa Center for Tax Policy

NBOSI

A Publication of the National Blue Ocean Strategy Institute