Mozambique and Equatorial Guinea in election spotlight

African elections are back in the spotlight this week, with the world’s longest-serving president—Teodoro Obiang in Equatorial Guinea—announcing he intends to run again in November’s elections to extend a 43-year tenure that began after a coup he led in 1979. Also this week, Mozambique President Filipe Nyusi was re-elected for his third five-year term despite the country’s constitution only allowing for a maximum of two terms.

While his term as the country’s president ends in 2024, Nyusi is expected to lead his party until 2027. Both nations struggle with poverty fueled by widespread corruption despite the wealth of fossil fuels and other minerals which make up a sizable portion of revenues. Both are also likely to experience some growth as pandemic pains recede and domestic demand improves. The current search for alternatives to Russian gas should also boost FX inflows to gas-rich Mozambique and shore up its reserves.

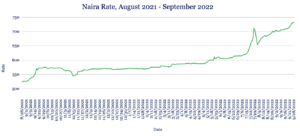

Naira hits new low even as CBN hikes rates

The Naira tumbled to a fresh record low against the dollar this week, trading at 734 on the unofficial market from 715 at last week’s close.

The sharp decline came even as Nigeria’s central bank hiked rates by 150 basis points to 15.5% as it seeks to combat high inflation, which the bank says has been exacerbated by worsening insecurity, broken critical infrastructure and high import costs on items such as wheat.

Destruction of farmland and livestock due to recent flooding is also threatening shortages of agricultural produce. In the short term, we expect the Naira to continue its depreciation against the dollar amid increased demand for FX in the parallel market.

Cedi at new low as Fitch warns Ghana default ‘probable’

The Cedi dived to a new record low this week, trading at 10.38 from 10.11 at last week’s close. Ghana said it had started discussions with the IMF this week as it seeks to secure a $3bn three-year loan package to stabilise its economy, given that surging borrowing costs have shut the country out of global capital markets.

The IMF is expected to conclude an 11-day mission to the country at the end of next week. Market watchers predict that Ghana will need to restructure its debt to unlock any IMF financing.

Fitch Ratings cut Ghana’s credit rating one notch to CC, signalling a ‘default of some kind appears probable’. Against that backdrop, we expect the Cedi to continue weakening beyond the 10.50 level in the near term.

Rand sinks beyond 18 in ‘risk assets’ selloff

The Rand depreciated against the dollar this week, trading at 18.02 from 17.95 at last week’s close—the first time it has traded weaker than 18 since May 2020. The latest decline came as risk assets continued to sell off following the US Federal Reserve’s 75 basis point rate hike last week.

On the domestic front, South Africa’s economy lost 1.6 million work days in the first half of the year due to strike action, predominantly over wages. Public sector workers may strike for the first time in a decade over poor pay.

Given the global risk-off sentiment and the country’s domestic challenges, we expect the Rand to remain under pressure in the near term.

Egyptian Pound touches all-time low as FX reserves fall

The Pound hit a record low 19.53 against the dollar this week, before recovering to trade at 19.48—marginally stronger than last week’s close of 19.49.

Dollar scarcity is ongoing in the country, with Egypt’s net FX reserves standing at $33bn in August, the lowest level since 2017. The government is seeking to raise up to $6bn by June next year from the partial sale of as-yet-unnamed government-controlled entities through a series of IPOs.

Given the dollar’s strength, increased tensions around Russia’s war in Ukraine and strained economic conditions domestically, we expect the Pound to weaken further in the coming weeks.

Kenyan Shilling at fresh low as dollar soars

The Shilling fell to a fresh low against the dollar this week, trading at 120.50/120.70 from 120.35/120.65 at last week’s close as FX demand remains elevated and the greenback continues strengthening on the back of last week’s US rate hike.

While we expect the Shilling to remain under pressure overall in the week ahead amid month-end dollar demand from importers, Kenya may see some benefit from recent financial turmoil in the UK, which plunged the Pound to a record low against the dollar.

Although Kenyan exports to Britain, such as cut flowers, may fall, the country may see lower costs on imports from the UK including cars, machinery, alcoholic beverages, pharmaceuticals and electronics. Around 2.3% of Kenya’s external debt burden is denominated in Sterling.

Shilling slides amid Uganda Ebola outbreak

The Shilling depreciated against the dollar this week, trading at 3861 from 3820 at last week’s close, pushed lower by the Fed-driven stronger greenback. Ebola infections have risen across the country, with almost two dozen suspected deaths recorded at the start of the week.

Interns at the hospital that is handling the most cases also went on strike this week, citing a lack of appropriate safety gear, risk allowances and health insurance.

Meantime, Uganda said coffee production could hit a record level in the 2022/23 growing season due to better rainfall and crop plantings. Overall, we expect to see the Shilling continue weakening in the near term.

Tanzanian Shilling touches 3-month high

The Shilling touched 2328 this week, its strongest dollar level since June, before dipping back to 2332—in line with last week’s close.

Tanzania this week said it is partnering with India to build irrigation systems across the country to increase agricultural output. It has already started constructing more than a dozen large dams in preparation.

Meantime, the Bank of Tanzania said will continue to gradually reduce liquidity in the market until the end of October to tackle rising inflation. Following a recent US investor trip to Tanzania, we expect inflows to strengthen the Shilling in the near term.

Note to journalists: please feel free to quote from this briefing for news reports and let us know any requests for further comment or interviews via the contact details at the end, or by reply to this email. AZA is Africa’s largest non-bank currency broker by trading volume at over $1 billion annually. See https://www.azafinance.com

Note to journalists: please feel free to quote from this briefing for news reports and let us know any requests for further comment or interviews via the contact details at the end, or by reply to this email. AZA is Africa’s largest non-bank currency broker by trading volume at over $1 billion annually. See https://www.azafinance.com

Issued by AZA. This Newsletter is produced as a service to our clients. It is prepared by our dealing professionals and is based on their understanding and interpretation of market events. AZA cannot be held responsible for any losses of whatever nature sustained as a result of action taken based on comments contained in this publication.

For more information, high-resolution charts or interviews, please contact:

Gavin Serkin

[email protected]

+44 20 3478 9710