Ghana’s pensions industry has become one of the most exciting in recent years, as it enjoys rapid growth, innovation, and improving regulation. Pension fund assets have become a significant component of financial sector assets, driven especially by the remarkable growth of the private pensions market, which barely existed before Ghana’s landmark pension reforms took off in 2008.

Indeed, continued expansion of pension assets and investments is a crucial feature of the government’s strategy to develop the capital and financial markets, with the goal of increasing and diversifying the financing of both public and private investments in Ghana. Further, there are promising signs of digitalization in the sector, which, among other benefits, is expected to facilitate the extension of pension coverage to the millions who currently lack it.

Growth Trends

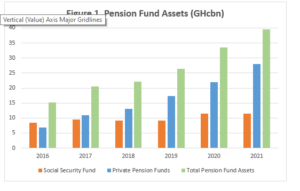

The rapid growth of the pensions industry is seen, among others, in the growth of assets under management, the increase in the number of registered private pension schemes, and the steady rise in active pension scheme contributors. From 2016–2021, the size of pension fund assets grew by 160% from GH¢15.20 billion to GH¢39.56 billion (see Figure 1), with an average annual growth rate of 21.4%.

This growth was largely propelled by private pension funds, whose total assets under management rose by 313% over the period, from GH¢6.79 billion to GH¢28.02 billion, with an average annual growth rate of 33.6%. On the other hand, the basic national social security scheme (that is, the Social Security and National Insurance Trust (SSNIT) scheme, which is publicly managed) experienced an overall asset growth of just 37% from 2016–2021, as its assets jumped from GH¢8.41 billion to GH¢11.54 billion in the period.

While the private pension funds, given their design and smaller payouts, were always going to grow bigger, collectively, than the SSNIT scheme, the latter’s challenges, including its weak investment returns and higher payouts relative to contributions, have led to its modest asset growth during the period.

Comparing pension fund assets growth with GDP growth, it is obvious that the former has outpaced the latter. Thus, pension fund assets increased from 6.9% of GDP in 2016 to 8.6% in 2021 (see Figure 3). The improvement was entirely due to the growth in private pension fund assets, which jumped from 3.1% of GDP in 2016 to 6.1% of GDP in 2021. On the other hand, the ratio of the SSNIT fund’s assets to GDP shrank from 3.8% to 2.5% in the period.

Private pension fund assets are predominantly held in government (comprising central government, local government, and statutory agency) securities, with 83.7% of assets invested in these securities in 2021, a marginal increase over the 82.1% ratio in 2020 (Figures 4 and 5).

The second-biggest asset class is corporate debt securities, which accounted for 5.2% of the total assets in 2021, up from 4.6% in 2020. Bank-issued securities, such as fixed deposits, negotiable certificates of deposits, and bankers’ acceptances, followed with 4.9%, down from 7.5% of the total assets in 2020. Collective investment schemes accounted for 3.2% of the total assets, compared with 1.8% in 2020. Meanwhile, equities constituted 1.6% of the total assets, down from 4% in 2020.

Unlike the private pension funds, the SSNIT fund has a more diversified asset base, led by investments in unlisted companies, which constituted 26.6% of total assets in 2021 (Figure 6). The next significant asset class is investment properties, with 22.8% of total assets, followed by listed companies, with 19.5% of total assets. Government bonds accounted for 7.3% of total assets in 2021, while corporate loans accounted for 6.3% and corporate bonds 1.2%.

The number of workers contributing to pension schemes has also been growing. Active contributors to the SSNIT scheme, which is mandatory for all formal sector workers, went up from 1.3 million to 1.7 million between 2016 and 2021, while the number of contributors to the mandatory Tier 2 private pension scheme increased from 1.5 million to 2.5 million in the period (Figure 7). The National Pensions Regulatory Authority (NPRA) adds that over 400,000 people were enrolled in various informal sector schemes by the end of 2021.

Improving Regulation

A relative newcomer to the regulation business, the NPRA continues to take important steps to ensure effective supervision of the pensions sector. Indeed, as with other critical economic sectors, the rapid growth of the pensions sector—and its intersection with other areas such as the capital and financial markets—demands constant improvements in the regulatory framework to make it dynamic and responsive to emerging risks and challenges. Recognizing this, the NPRA has adopted a risk-based supervision framework, whose benefits include enhanced surveillance, improved prioritization of the regulatory function and resources to ensure efficiency, and an overall strengthening of risk management and compliance within the sector.

The NPRA has also focused on developing its internal capacity to improve the performance of its work. To this end, it has taken steps to strengthen governance and management, in addition to facilitating professional development and training of its staff. The regulator has also been augmenting its capacity and systems to enhance supervision of the SSNIT scheme, especially as the scheme grapples with apparent sustainability challenges. Also, through the National Pensions College, which the NPRA established in March 2021, the regulator has begun to facilitate the training and upgrading of skills of industry professionals.

A major development in 2021 was the revision of investment guidelines for private pension funds. This revision was carried out against the backdrop of calls for private pension funds to play a stronger role in financial and capital market development by, among others, diversifying their asset bases. The revision took cognizance of these concerns and has allowed for some diversification of assets while maintaining necessary safeguards to ensure safe and rewarding investments.

Low Informal Sector Coverage a Key Challenge

Despite the continuing development of the industry, the generally low coverage of pensions in the national economy, especially within the informal sector, is a lingering challenge. At the same time, the lack of pensions is considered a significant contributor to old-age poverty in Ghana, with the problem particularly acute in the rural, underdeveloped parts of the country.

With just 4% of the informal sector covered by pensions, the NPRA has made improving this ratio, as well as generally expanding pension coverage in the country, a critical element of its strategic plan for the next five years. For instance, working with the government and Cocobod, the NPRA has set its eyes on leveraging the recently introduced Cocoa Farmers Pension Scheme to provide pension cover to 1.5 million cocoa farmers, thereby significantly increasing pension coverage in the informal sector. The regulator has also been stepping up its education and outreach programmes, aimed at improving knowledge on pensions and encouraging enrolment in pension schemes by workers and groups in the informal sector.

Digitalization Set to Offer Benefits

The digitalization of the economy, which the government has been vigorously pursuing in the past five years, has touched all sectors, including pensions. The rapid automation of the national payments system, through leveraging mobile technology and other innovations, now makes it possible for the pensions industry to reach or connect with previously hard-to-reach segments of the working population. Taking advantage of this, a number of private pension players have designed “digital pension products”, often in collaboration with financial services firms such as banks. These products enable digital onboarding of new contributors and facilitate the collection of contributions by accepting payments through digital channels.

The SSNIT scheme is also seeking to leverage the digital payments system to increase penetration in the informal sector, as managers aim to strengthen the scheme’s sustainability by growing its membership. To this end, the managers have taken steps to deepen public understanding of the scheme and its benefits, especially within the informal sector, with a view to increasing enrolment and contributions, which would be facilitated by accepting payments through mobile and other convenient platforms.

Digitalization has also begun to improve the interface between pension service providers and their clients. It is now possible in many cases for clients to access critical information about their pensions, such as fund statements, remotely through online access. This is likely to facilitate the giving of rapid feedback and the reporting of complaints for redress. All these are encouraging developments which the sector should build upon, recognizing that the room for improvement is large, since digitalization—if fully exploited in all its dimensions—has further benefits to offer.

Credit: All data used were sourced from National Pensions Regulatory Authority (NPRA) Annual Report 2021.