The manufacturing and service sectors, including agribusiness but excluding trade, recorded an estimated GH¢158.4billion financing gap in 2020 – about 40 percent of GDP according to the Minister of Finance, Ken Ofori-Atta.

Despite the huge gap, Mr. Ofori-Atta is however confident that it can be plugged by the soon to be established Development Bank Ghana (DBG): a non-deposit taking lender with focus on four key sectors – agribusinesses, manufacturing, Information Communication Technology and mortgage financing.

In terms of lending duration, he said the gap for long-term finance – tenure of three years or more – is GH¢52.4billion (US$9.3billion) and that the ability of lenders to provide long-term finance requires access to long-term funding to avoid large maturity mismatches; a situation he is optimistic will become a thing of the past when the DBG becomes operational by end of the year.

When compared with other economies within the continent, he lamented that credit to the private sector remains relatively low.

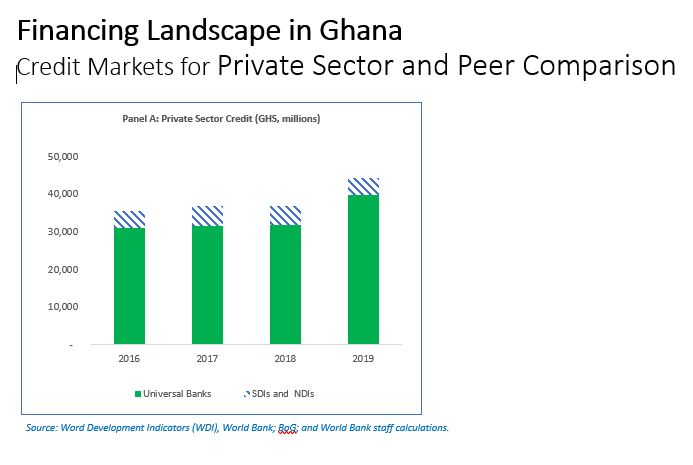

Although credit to the private sector rebounded in 2019 as seen in Panel A above, it was relatively low to the size of Ghana’s economy. From the graph 2016 to 2018 shows huge stagnation with total credit (banks, SDIs and NDIs), but an increase to GH¢46.3billion (US$8.4billion) in 2019 (see Panel A).

Mr. Ofori-Atta explained that banks continue to allocate 38 percent of their assets to investments (mostly government securities), compared with only 31 percent to loans and advances.

In comparison to others on the continent, Ghana’s credit to the private sector was only 12 percent of GDP in 2019 – significantly lagging its peers (see Panel B). “Credit to the private sector in Ghana has been consistently lower than expected from Ghana’s structural characteristics (including population size and income level),” he said.

The services sector received the highest share of bank credit – 23 percent, followed by commerce and finance at 17 percent.

Similarly, in 2018 only 33 percent of the volume of banks’ loans and advances had a maturity of more than three years – of which loans with maturity of more than five years was only 15 percent, as seen in Panel A, compared to 23 percent in upper-middle-income countries. “In comparison, the volume of loans with maturity of more than three years accounted for 35 percent in Nigeria,” Mr. Ofori-Atta said.

However, from Panel B, funding of Ghanaian banks is dominated by deposits and borrowings with maturity of less than one year – 85 percent and 64 percent, respectively (82 percent combined).

The finance minister, who spoke during a meeting with large producing members of the Association of Ghana Industries in Accra, assured them that the DBG – a development-oriented lender – will considerably ease the credit situation for producers. To do this, he said, the soon to be established lender will be able to grant patient capital of up to 15 years in what will be a huge boost for local businesses.

Capitalisation of DBG

“We are aiming to establish DBG by end-2021 with an initial capitalisation of around US$250million from the government of Ghana,” he revealed, adding that US$200million of the amount had been paid as at May 2021. Other funding sources include US$250million from the World Bank and €170million from the European Development Bank.

Meanwhile, KfW – a German state-owned investment and development bank, also plans to support with €46.5million as tier 2 capital, plus technical assistance to the tune of €3million; as well as initial support from the French Development Agency (AFD) through partnership and guarantees.

He revealed that the African Development Bank has also shown interest but is yet to commit. With all these partners onboard, he said, “The governance structure will enable DBG to pursue its mandate in a professional manner, fulfilling its development mandate while maintaining financial viability and giving comfort to shareholders and financiers of the bank”.