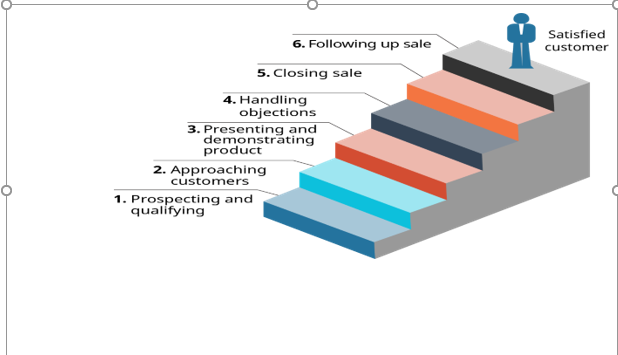

Dear readers, the above diagram shows the typical processes one goes through to acquire a customer’s consent to open an account. It is a mutually satisfying experience, but it can be quite tedious for both the staff and the customer. Maintaining the status and keeping the customer delighted with the service is another unending process.

Are you in wealth management? Are you taking care of customers whose transactions make the most of your bank’s revenue? Are you assigned to build their wealth or just to be nice to them to prevent them transferring their accounts to your competitor? How genuine are you in your relationship with these account holders? Do you know that sometimes when such customers cough, the whole bank shakes?

The Politics in Your Customer’s Organization

As a human institution, your customer’s business is your business. Do not feel that you are being too intrusive. A good manager, in a bid to know the customer’s business may detect some sort of politics within the organization and know how to tread cautiously. I remember the case of a senior Relationship Manager who, during a working visit to a key account’s factory, met an agitated staff, grouped together on the verge of starting a demonstration at the front of the factory. They were threatening to report certain unethical practices within the company to the government. Since the account had benefitted from a big credit facility from the bank, the Senior Relationship Manager, who was on good terms with some of the staff, engaged their leaders in an informal discussion, which eventually ended up successfully, with the management staff promising to rectify the anomalies. Apparently, the senior RM played a critical role and sometimes gave advisory services to the CEO, which earned him a great deal of respect. The strike could have caused losses to the business and obviously a default in the loan repayment schedule. This may be an extreme case, but when a Manager listens to the grapevine, certain sensitive information may emerge which can give the bank a heads-up during decision-making, while gaining a competitive edge.

The Multi-Banked Key Account:

There was a case of a valuable SME account whose daily cash deposits were lodged by the company driver. He was a loyal and trusted staff of the Proprietor, whose account was at a branch in Okaishie. (The central business district of Accra). He was therefore entrusted with huge volumes of cash to deposit. When a new branch of the same bank was opened at Ridge, it was closer to the customer’s factory, (located at Achimota, one of the suburbs of Accra). Due to the value of the account to the bank, the RM did constant close-marking to ensure that the sales still passed through the bank, even from the Ridge branch. A year later, the driver started encountering friction with the new Bulk Tellers at the new branch, who did not appreciate the value of the account and started treating the driver in an unprofessional manner. Can you imagine that the driver managed to convince his employer to open another account at a bank which was just 50 meters from his factory? Yes! That is the power of influence that the driver possessed. A manager could say that he is a “mere driver”, but you never know how far his influence reached.

Look for the “Big Shots” in the company:

How do you determine who the big shots are? Is it the size of the office, the number of staff under him or her? Is it the cars they drive? Every company has its own way of doing things but make sure you are on a cordial relationship with those you have identified. Do not forget to include them in your list of beneficiaries of your company’s end of year souvenirs for customers.

Identify the Young Sharp Shooters:

In some organizations, the CEO or management staff are able to identify some “Fliers” who are being groomed for top positions in the business. It could be the son of the owner, an in-law, or a genuine “sharp brain” who is a strategic thinker and has been able to rub shoulders with the management staff. While making effort to sell your bank’s products, you can discover the company’s future vision and goals from such persons in your conversations. There are instances where you can indirectly detect signs of over-trading, over-expansion, diversion of funds or business. A manager should be “street- smart” to detect such possible early warning signals or default of a loan.

Seizing Opportunities:

Is your key account celebrating an anniversary, new product launch, planning a corporate social responsibility, like free medical or eye screening? These are popular events that your bank can collaborate or get involved in. If possible, get their consent to set up a stand to also market your products. If the event demands the collection of funds, be there to do that on their behalf or recommend them to select your bank’s digital app for their payments and receipts. It cements the bond of friendship. You can opt to be in their branded T-shirts or seek permission to be in your bank’s corporate branded outfit. Seize the opportunity to partner with their brand and you never know, new accounts can be opened. At such programs, do not forget that your art of public speaking will be put to test!

Be a Problem Solver:

You may ask yourself: What can I do to solve a key account holder’s problem? Yes, you can. In trying to work with all the listed recommendations, you will reach somewhere when your customer will sometimes share some major company strategic decisions with you. Remember that other banks are always visiting and trying to win same accounts. There is nothing wrong with being multi-banked but make your service exceptional.

Going the Extra Mile:

It is nice to know more about your customers as they bank with you. Have you sat down to scrutinize your key account’s bank statement for the following beneficiaries of their cheques? They could be other corporate bodies, third party individuals, suppliers, schools, churches, investment companies, voluntary organizations, old school groups, and so on.

Do some of these beneficiaries have accounts with you? That is fine, but if they do not, seize the opportunity to go the extra mile to get to know them. If your key account is a church goer, can you be introduced to the church or any church group? Take it from there and the rest will follow.

For more insights on this topic, please book a copy of my new book, “THE MODERN BRANCH MANAGER’S COMPANION” which involves the adoption of a multi-disciplinary approach in the practice of today’s branch management. It also shares invaluable insights on the mindset needed to navigate and make a difference in the changing dynamics of the banking industry. Call 0244333051 for your copy.

ABOUT THE AUTHOR

Alberta Quarcoopome is a Fellow of the Institute of Bankers, and CEO of ALKAN Business Consult Ltd. She is the Author of two books: “The 21st Century Bank Teller: A Strategic Partner” and “My Front Desk Experience: A Young Banker’s Story”. She uses her experience and practical case studies, training young bankers in operational risk management, sales, customer service, banking operations and fraud.

CONTACT

Website www.alkanbiz.com

Email:alberta@alkanbiz.com or [email protected]