The transmission mechanism and global severity of Covid-19 pandemic pose significant threat to human health and societal existence at large. The impact of this novel virus is so glaring on the health systems of both advanced and developing economies. Many countries are facing strong excess demand for health care: too many critical patients for too few intensive care unit (ICU) beds and ventilators.

Expanding health care supply requires turning hotels, barracks and possibly schools into ICU and converting selected manufacturers into ventilators makers (Surico & Galeotti, 2020). Medical personnel are heavily needed thus most governments are recalling retired nurses and doctors to assist in fighting the pandemic. These emergency health care supply measures have serious implications on central government budget outlays.

The impact on the levels of both micro and aggregate economy activities cannot be overemphasized. Just like a normal functioning human being who enjoys a constant flow of blood to survive, economies also enjoy constant cycle of economic activities.

However, the current situation where a lot of economic activities have been truncated or nevertheless being in abeyance have rendered the economies of most nations to be at standstill. As it is increasingly becoming the norm in most countries, social distancing and varying degrees of locking-down are perceived to be the most efficacious containment measures to this pandemic.

As a result, most schools are on break and lessons are being held online, large gatherings such as weddings, sporting events, church congregations among other public gatherings have been suspended until further notice and shops offering non-essential services have been closed temporarily.

Consequently, economic activities have been disrupted in many emerging markets and frontier economies. An emerging market economy refers to a developing economy that is becoming more integrated with global markets as it evolves. Such countries exhibit some, but not all, of the characteristics of developed markets.

This is evidenced by increased liquidity in its domestic debt and equity markets, increased trade volumes, foreign direct investments, and the domestic financial innovation and development amidst improved regulatory quality. Notable examples of emerging economies include China, Mexico, India, Brazil and Indonesia among others.

On the other hand, a frontier economy is considered as a type of developing country which is more developed than the least developing countries, but too small, risky, or illiquid to be generally considered an emerging market. Examples include Ghana, Argentina, Botswana and Kenya just to mention a few.

Emerging and frontier markets potentially offer higher returns to investors due to their rapid rates of growth. The downside however is the increased exposure to risk. Thus, these markets are normally pursued by investors seeking high returns that are lowly correlated with other markets.

To compensate for the higher risk, they usually require higher risk premiums (returns in excess of the risk-free rates). The government treasury bill rates are widely used as the proxies for risk-free rates. It is therefore not surprising that, yields on debt securities in these economies are normally higher than those in developed economies.

Though the number of affected patients and death toll of COVID-19 in emerging and frontier economies remain relatively low compared to most European nations and USA, these economies have experienced declining economic and financial conditions mainly due to widespread effects on global trade and investments.

As the extent of Covid-19 damage becomes obvious in most nations by the passing of each day, the scarce economic and financial resources of these emerging and frontier economies are being overstretched. These economic and financial deteriorations are likely to trigger a phenomenon called “flight to safety or flight to quality”. Flight to quality is a financial market phenomenon where investors exit from or offload risky investments in return for safer investments. It triggers a sudden appetite for safe assets relative to risky assets.

During periods of intense economic uncertainty, return seeking investors trade off higher returns for safe assets with low price volatility, low downside risk, low default risk and high liquidity. Investors at this point are much concerned with preserving each Dollar or Cedi value of their investment rather than the marginal gains from committing these resources. Desperate times like this engender capital flight from emerging and frontier markets as investors seek safe haven assets.

Typically, US treasuries, US Dollar and gold among others are considered safe haven assets and are mostly preferred by investors during crisis. It is worth mentioning that in the short term it is only investments in financial assets such as bonds and equities that suffer from capital flight. Whilst existing foreign direct investments (FDIs) are immune from capital flight in the short-run because they cannot be immediately disengaged, the ability of these economies to attract new FDIs are hindered due to the uncertainty and crisis.

Overview of Ghana’s Debt Market

The financial market restructuring in the early 1990s led to the creation of the debt market in Ghana. Since the issuance of the first 5-Year debt instruments to provide foundation for active trading of bonds on the newly created Ghana Stock Exchange, the bonds market has witnessed considerable improvement.

The debt or fixed income market widely known as the bonds market in Ghana is a market for all debt instruments issued in Ghana. These include securities issued by the Government of Ghana, Bank of Ghana and corporate entities. It has two main divisions: the primary and secondary market. Whilst the primary market is the market for the initial issuance of all debts instruments, the secondary market is essentially for trading already issued securities.

Securities issued on the bonds market ranges from short-term to long-term with typical maturities of 91-Days, 182-Days, 1-Year, 2-Years, 3-Years, 5-Years, 7-Years, 10-Years and 20-Years among others. Government of Ghana bonds may be categorised into domestic bonds, domestic dollar bonds and Eurobonds depending on the issuance and settlement dynamics. Domestic bonds are bonds issued and settled in Ghana and also denominated in Ghana Cedi. Dollar bonds are bonds issued and settled in Ghana but denominated in a foreign currency usually US Dollar.

Eurobonds are bonds issued and denominated in a foreign currency (USD) and settled in the country of the currency in which the bond is denominated. For instance, trade settlement of Euro-dollar bonds issued by Ghana takes place in the US.

From this illustration, the main distinction between the domestic dollar bond and the Eurobond is the country where trade settlement of the bond takes place. The longest dated domestic bond on the market is the 20-Year Bond. The 41-Year Eurobond which is the longest dated bond issued by Government of Ghana also doubles as Africa’s longest dated bond at present.

Existing Securities on Ghana’s Debt Market

| Summary of Securities | |

| Security Type | Number Existing |

| Benchmark Securities | 8 |

| Non-Benchmark Securities | 26 |

| Treasury Notes | 12 |

| Treasury Bills | 82 |

| Domestic US Dollar Bond | 1 |

| Eurobond | 9 |

| Corporate Bonds | 61 |

| Total | 199 |

Source: Ghana Fixed Income Market (GFIM) status report, March 2020.

How the bond market is faring

The bonds market has been phenomenal in recent years. The periodic issuance of securities by the government through the ministry of finance as part of its debt management strategy and financing needs has deepened the bonds market. Through its issuance calendar, benchmark securities are been built across the various maturity tenors.

This, to a large extent has increased price discovery on the secondary market. The increased activities on the secondary bond market stem from the tight fiscal consolidation by the government. The successful completion of the 3-Year Extended Credit Facility under the International Monetary Fund (IMF) program has placed the country on the path of accelerated economic growth and fiscal discipline.

Macroeconomic indicators over the years have improved significantly. GDP grew by 5.6% as at quarter-3 of 2019, one of the highest within the Sub-Saharan African sub-region. Inflation has been on the downward trajectory, currently standing at 7.8%, within the range of the government’s medium term inflation target of 8+/-2.

Sound macroeconomic fundamentals and prudent economic management in line with the government fiscal consolidation measures have increased investor confidence both domestically and on the international front. This is evidenced by the oversubscription of recent bonds issued. In March 2019, the Ghanaian government raised $3 billion Eurobond on the international capital market.

According to the Finance Minister, they received bids of about $20 billion representing over 600% of the targeted amount. The Euro- Dollar Bond was issued in three tranches at a maturity period of 7 years with 8.75% coupon rate, 12 years with 8.125% coupon rate, and 31 years with 8.95% coupon rate. Not only does this depict the growing appetite for risky assets by global investors but also a positive signal of the vote of confidence in Ghana’s economy.

Fast-forward to February 2020, amidst the coronavirus pandemic albeit not that pervasive at that time like now, Ghana successfully raised $3 billion Eurobond from the international capital market. The issuance was met with 5 times oversubscription. Some market analysts contend that the bond was fairly priced which reflects the reduced risk premium due to improving economic conditions and future economic prospects. On the domestic front, the government has been successful with periodic domestic bonds issuance as pre-determined by the issuance calendar communicated by the ministry of finance in line with its financial needs and macroeconomic targets.

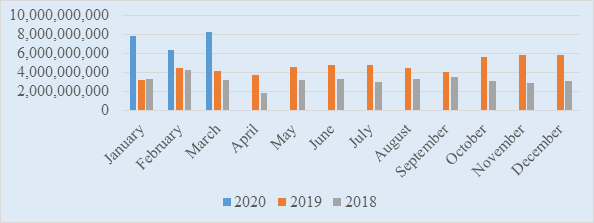

The Secondary Market at a Glance

Source: Ghana Fixed Income Market (GFIM) status report, March 2020.

The above graph shows the development in trading activities on the secondary bond market from 2018 to March 2020.

Market Reaction to Covid19

However, as the number of Covid-19 cases rise each day following the confirmation of the first case on March 12, 2020, the secondary market has seen significant volumes of trades by foreign investors as they exit their domestic bonds position amidst the global uncertainty surrounding the pandemic.

According to some market participants, the past three weeks witnessed increased sales by the offshore investors. This sparked unusual volatility in the bond market. Although some traders contend the market is relatively stable as compared to the initial days of the pandemic.

We can recall that, as part of measures and interventions to address the perennial depreciation of the Cedi against its major trading partners, the Bank of Ghana commenced the forward auction of forex in quarter-4 of 2019. This is expected to help financial institutions plan their forex needs in advance to tackle excessive demand and speculations on the forex market.

To a large extent this intervention was yielding positive results in the early part of 2020 as the cedi posed some positive gains against the other currencies. It is common knowledge that when foreign investors take positions in our domestic or Eurobond, they do so by bringing in forex in the form of USD which initially increases supply of USD in the country.

On the other hand when they are exiting their positions, the proceeds from the sale of bonds are converted to USD and repatriated to these foreign investors. This exerts upward pressure on the USD causing the domestic currency to depreciate.

Accordingly, the Cedi which has been appreciating against the USD in the early months of the year has started eroding some earlier gains mainly due to this capital flight. The graph below provides the trend in Bank of Ghana’s USD mid-rate. The Cedi which opened the year at 5.5342 to a dollar appreciated against the Dollar reaching a low of 5.2869 during the latter part of February 2020. The year-to-date appreciation of the cedi against the greenback on March 11 prior to the 1st case of Covid-19 in the country was about 3.9%.

Subsequently the country recorded the first case of Covid-19 on March 12, 2020. About three weeks later, the year-to-date appreciation of the cedi to the US Dollar stood at 0.57% by April 08, shedding off a greater portion of the prior gains. Within those 3 weeks, the secondary bond market saw more bond sales from the offshore investors amidst the Covid-19 uncertainties. Given the decline in global trade activities as a result of the pandemic, it stands to reason that the key motivator for the reversal of the cedi’s prior gains is the actions of foreign investors.

The ensuing graph depicts quarter-1 (Q1) trend in USD for the past 3 years. We can observe from the graph that the Cedi was relatively stable in Q1 of 2018. Q1 of 2019 saw the Cedi depreciating against the USD. The Cedi posted impressive performance against the greenback in the early part of Q1 in 2020 till it started reversing earlier gains due to the capital outflows experienced on the bonds market amidst the pandemic.

Quarter-1 Trend in USD

Source: Bank of Ghana’s Website

The initiative launched by the G-20 nations during a summit in 2011 recognized that a robust domestic bonds market is critical to a country’s ability to withstand capital flows, reduces reliance on foreign currency borrowings, lessen exchange rate risks and contributes to reduction in current account imbalances. This improves the capacity of the country’s macroeconomic policies to better withstand external shocks. It is on the back of this increased exposure to exchange rate volatilities that we strongly advocate for the need to strengthen the capacity of the domestic bonds market so as to support the government’s ability to generate funds locally thereby reducing the susceptibility of the country to unanticipated external shocks.

How to develop the capacity of our domestic bond market

Whilst we commend relevant stakeholders such as the ministry of finance, Bank of Ghana, Securities and Exchange Commission, Ghana Fixed Income Market (GFIM) under the umbrella of the Ghana Stock Exchange, Central Securities Depository, all financial institutions and market players for their contribution thus far towards the development of Ghana’s bonds market, we still believe there is more room for improvement.

First and foremost, all market players such as policymakers, regulators, fixed income traders and other participants must embrace and uphold the importance of market integrity. Market integrity implies the ability of the market to function in a fair and sound manner devoid of price manipulation, misleading information or insider trading.

Transactions should be executed safely and all laid down settlement protocols followed to ensure proper transfer of titles to beneficiaries. There must be adequate mechanism in place to detect any infractions on the market. Any infraction detected must be swiftly investigated and the necessary sanctions applied.

The code of conduct for licensed dealers on the secondary market as stipulated in the Ghana Fixed Income Market (GFIM) manual must be fully enforced. It is when investors are sure of fairness and transparency on the market that they will be more willing to participate and invest in the bonds market. Strict enforcement of the legal and regulatory requirement on the market will give respite to affected parties in case of disputes.

Also, bond is a debt instrument which carries inherent risk of possible default. As a result, there must be proper mechanism in place to assess the credit worthiness of each issuer. Whilst government debts are usually touted as risk free (a position that has been challenged in recent years following default on some sovereign debts), investors will need information to assess the credit worthiness of corporate bond issuers.

This lack of information on the true credit worthiness of corporate entities partly account for the poor performance of corporate bonds on the secondary market. In the absence of proper credit rating of entities, investors rely on their own judgement to assess the default risk of an issuer.

We contend that, the establishment of a well-equipped, credible and transparent local credit rating agency that can independently assess the credit worthiness of all local firms just as Fitch, S&P and others have been rating sovereign nations and multinational firms will go a long way to boost the domestic debt market. Surplus-spending investors can make informed decisions and confidently lend to these corporate bodies.

Broadening the variety of debt instruments on the bonds market is another useful means of improving the domestic bonds market. This will offer the investing community wide array of debt instruments to meet their varying needs. The development of the repo guidelines is a step in the right direction.

Bank of Ghana’s repurchase agreement (repo) guidelines mandate repo trades in Ghana to be documented under the Global Master Repurchase Agreement (GMRA). We envisage this development will spur innovations on the repo market as financial institutions can use the provisions of the internationally accepted GMRA to enter into unique repo trades that meet their needs in the future.

Conclusion

Continued reliance on external funding on the international capital market renders the country vulnerable to external shocks mainly due to reversals of capital flows during crisis or uncertainties. This has far-reaching adverse impact on the exchange rate and associated macroeconomic indicators. Thus, it is high time we strengthened and developed the capacity of the domestic debt market to better take advantage of its concomitant benefits.

Note: Year to date appreciation of the Cedi was as at 8th April,2020.

About the Authors:

Daniel Taylor is a chartered Accountant with extensive knowledge and experience on capital market with focus on emerging markets and frontier economies. He holds certification from The Financial Markets Association (ACI). He holds a Bachelor of Commerce Degree from University of Cape Coast and currently a final year Master student in Economics and Finance at UCA in France.

Bernard Sarpong is a young Economist with research focus on Development, Financial and Monetary policies in Emerging and Frontier Economies. He holds both Master of Philosophy and Bachelor of Arts degrees in Economics from the University of Ghana. He is currently a Fixed Income and Money Market Dealer at Republic Bank Ghana Ltd.