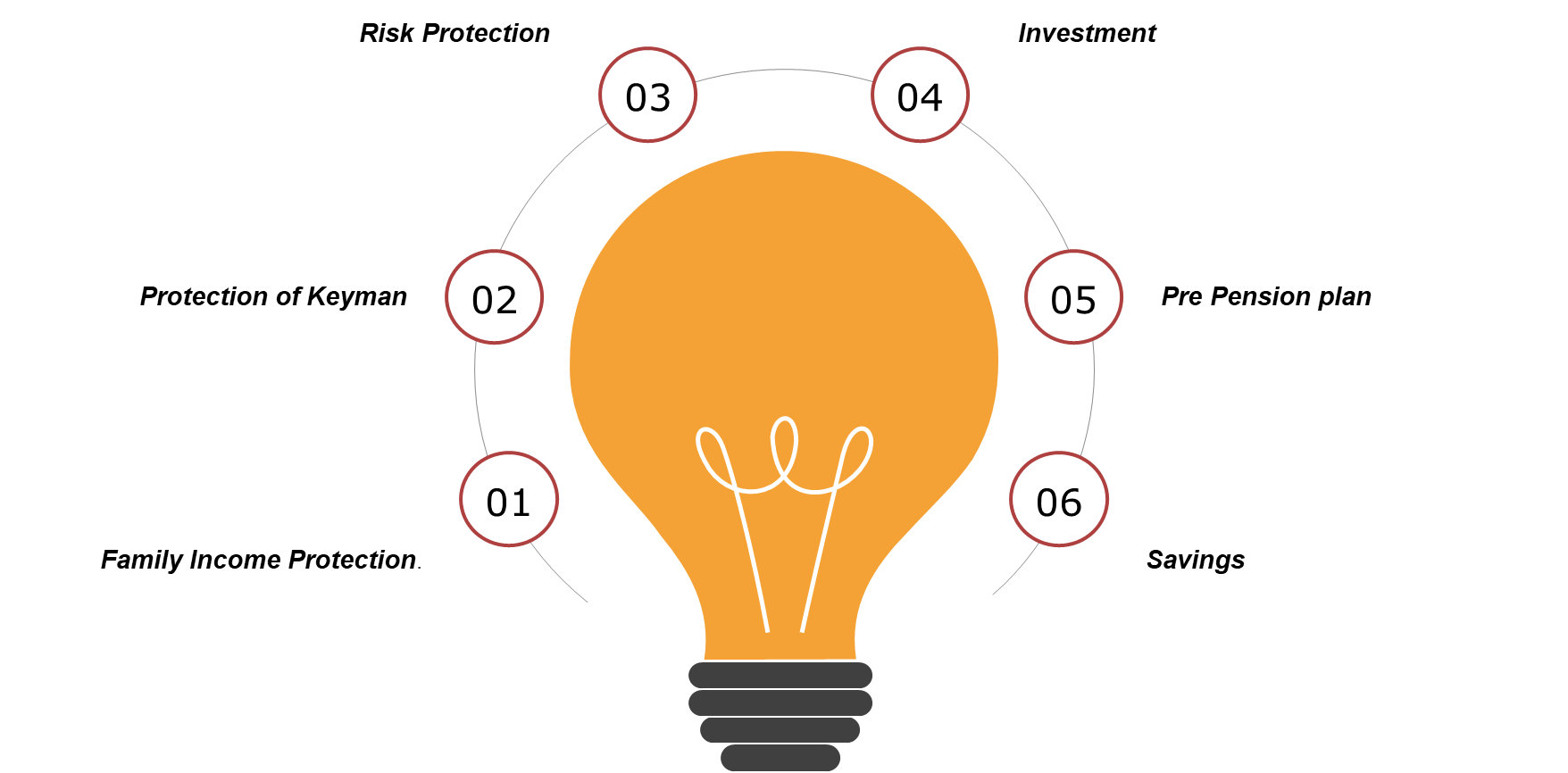

Life insurance covers your life and also has provisions to provide a savings and investment avenue. Life insurance is a long-term contract and requires you to pay the premiums in monthly installments. Life insurance can be done for any value based on the premium the policy holder is willing to pay.

Life presents us with two main risks. The risk of dying earlier and the risk of living more than expected age. When you die earlier, you could leave a responsibility behind like taking care of your children and their education or taking care of your family as a whole when you are the bread winner. Again, when you live more than expected, you face the risk of having to take good care of yourself after pension for the number of years God will bless you with.

These are the main reasons why life insurance policy is very vital for us. Life policies are designed primarily to bring a solution to these two main risks. Insurance does not prevent the loss from happening, but it reduces it financial impact. This is why it is very important to know and understand the following before you sign a Life Insurance policy.

Type of Policy

The first thing you need to know is the type of policy. Life policies are design base on two main features. There could be a pure risk only policy or an investment only policy or combination of the two. With a pure risk policy, the only time you benefit is when the insuring event occurs. eg. Death, total permanent disability. Pure investment policy usually include a “cash value” account, which builds value over time. eg. Investment.

Waiting Period

A waiting period refers to the time an insured must wait before some or all of their coverage comes into effect. Only when the waiting period has passed can the insured have a right to file a claim for the benefits of the insurance policy. However, if the policyholder or the assured person dies as a result of an accident, the full death benefit is payable immediately. Kindly know this from your insurers.

Cooling Off

Every life policy has a cooling. It is normally 15 days for client to read through the policy document before signing document receipt. The client has every right to reject the policy if the terms and condition are not favorable and the premium should be refunded. Client accept the policy after signing the document receipt.

Surrender Period / Benefit

Most companies’ policies attained surrender cash value after 24 months. Most of the pure risk covers do not have surrender value. When you cancel your policy before twenty-four months, you get nothing. This is a benefit payable to the policyholder on termination of a policy after the policy has attained a cash value, but before maturity. Penalties apply on early surrender. Your benefit is usually affected by the length of the policy.

Partial Cash Encashment

Once a policy has acquired a surrender value, partial encashment(s) may be made in the lifetime of the policy and may not exceed normally 50% of the surrender value.

Policy Loan

A policy loan is issued by an insurance company and uses the cash value of a person’s life insurance policy as collateral.

Lapse Rule

The onus is usually on the insured to make sure the premiums get to the insurance company. The insurer shall advise the policyholder of premiums due under the policy. Insurers may not honour their part of the obligation when policyholders fail to honour their part of the contract by paying their monthly premium for a consecutive three (3) months period.

Age Limit

Most of the companies and the policies have an entry age which usually is 18 years. Maximum age for the policyholder is normally 60years. There are also maximum age for covering lives. Kindly know these from your insurer.

Notification

Some companies give number of days within which the policyholder or beneficiary can notify them of, especially death claim. Kindly enquire from your insurance company their notification period.

Claim

Below are some of the documents the assurer may require to meet your claim. The insurer will require a properly completed claim form. Most companies may also require original policy documents that was issued to you at inception of the policy. Where necessary, the following documents would be required: Photo identification of claimant, death certificate of covered life or policyholder, Police report for accidental death cases and Affidavit

Conclusion

Life Insurance policies bring a lot of benefits but if we do not understand what we are buying or properly understand the terms and conditions of the policy, we might not reap the benefits therefore. This is why it is very important to know the above before we sign the best life policy that would meet our needs.