Data published by the Bank of Ghana has shown that growth in deposits of commercial banks have been fluctuating in the last eight months, with figures in August even showing a decline, a development banking consultant, Dr. Richmond Atuahene, has attributed to the difficulty private sector is facing in the current pandemic-hit climate.

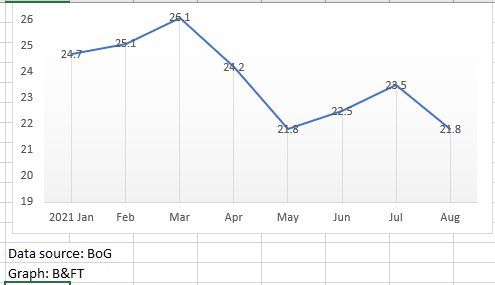

The Summary of Economic and Financial report (September) indicate growth in bank deposits have dropped to 21.8 percent in August 2021 from the 24.7 percent recorded in January this year. In fact, deposits saw its best performance in the first quarter of the years as it recorded growth figures of 24.7 percent, 25.1 percent, and 26.1 percent from January to March respectively.

But in April and the ensuing months, the trend was thwarted, as deposits dropped for two consecutive months (April and May), increased for another two consecutive months – June, July – and dropped again in August. In nominal terms, bank deposits have grown to GH¢111.6 billion in August from GH¢102.8 billion in January.

Commenting on the trend in an interview with the B&FT, Dr. Richmond Atuahene said it only explains businesses are still not out of the woods yet given both local and global conditions, hence, they are unable to make enough to keep with the banks for a long time.

“It has something to do with the slow economic activities. Businesses that shut down operations are now recovering and they have not yet gotten to their peak. As we go further and the economy opens, businesses will recover and deposits will grow again.

Even global conditions have not been favourable to the local economy. Import from China are becoming more expensive because of shortage of containers to this side of the world. And this is because other developed economies have increased imports from China and it is making it difficult for local importers to have stable and reliable supply of goods. Shipment from China has also become expensive and it is really affecting the operations of local businesses,” he said.

Other developments in the banking sector

Despite the sporadic performance of deposits, the BoG report says the banking sector remains strong and well-capitalised, with stronger growth in total assets, investments and deposits. Total assets increased by 16.7 percent to GH¢166.4 billion as at end-August 2021, driven mainly by a 28 percent year-on-year growth in investments to GH¢80.3 billion.

Financial Soundness Indicators (FSIs) have remained strong over the period. The industry’s Capital Adequacy Ratio was 20.7 percent at the end of August 2021, well-above the regulatory minimum threshold of 11.5 percent. Core liquid assets to short-term liabilities was 24.7 percent in August 2021 compared with 29.0 percent a year ago.

Over the same comparative period, net interest income grew by 17.9 percent to GH¢8.3 billion, marginally lower than the 18.7 percent growth a year ago. Net fees and commissions grew strongly by 21.8 percent to GH¢1.85 billion, higher than the growth of 8.9 percent for same period last year, reflecting the continued recovery in trade finance-related and other ancillary businesses of banks.

Again, total operating income rose by 15.7 percent, marginally below the corresponding growth rate of 17 percent. Cost control measures within the banking sector continued to support profit performance with operating costs increasing by 9 percent, lower than the 12.1 percent increase for same period in 2020.

The report further adds that the latest stress tests conducted on the banking sector show that banks remained resilient under mild to moderate stress conditions supported by the strong capital and liquidity buffers and the regulatory reliefs introduced during the pandemic.

: I need to be PATIENT!")