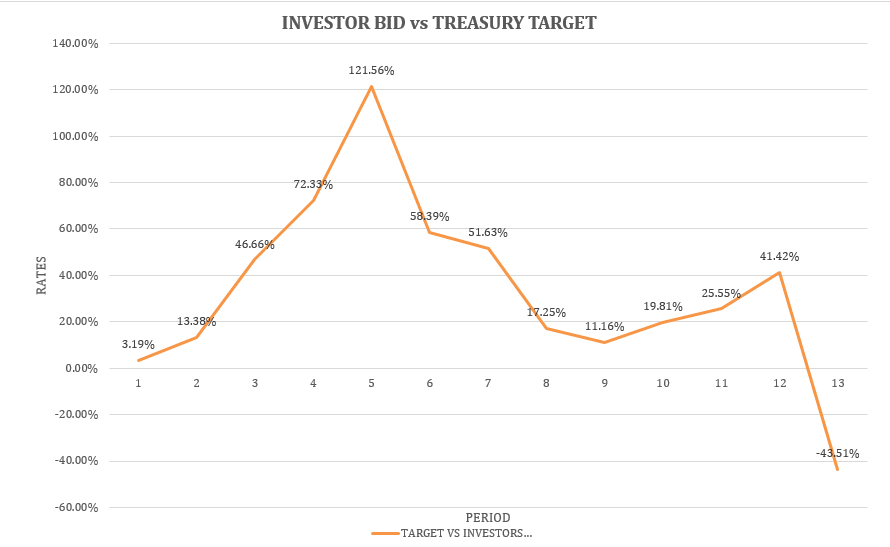

Treasury market suffers pullback in demand conditions

0 views

Topics in this article

Treasury billsomestic Debt Exchange Programme

Related Coverage: Economy

Editorial

The arithmetic of avoidable death

Tomorrow, the nation will gather at the UPSA Auditorium in Madina (and at other places) to remember the Departed 8. A cenotaph will be unveiled.

Agribusiness

Farmers bear cashew price crash as processing stuck below 6%

Ghana’s cashew farmers are reeling from a steep 2025 price collapse as the country’s processing capacity remains stalled below six percent, leaving the bulk of raw nuts exported with little local value addition.

Banking & Finance

BoG, industry push reforms for distressed business financing

The Bank of Ghana (BoG) is working with the insolvency and restructuring industry stakeholders to develop a more predictable and risk-sensitive framework for financing distressed but viable businesses.

Business

Ghana launches London Trade House to boost business opportunities

Ghanaian exporters now have a fixed address in one of the world's most influential cities, London, following the opening of the Ghana Trade House by the Ghana Export Promotion Authority (GEPA).

Banking & Finance

Mantrac partners Banks for easy equipment financing

Mantrac Ghana has partnered with five leading banks to break financing barriers and expand access to equipment for businesses across Ghana, creating new opportunities for local businesses to invest, improve productivity and accelerate growth.

News

ALX scales its enterprise offering to build AI ready workforces across Africa

Similar to the emergence of computers and other digital technologies that transformed organisational productivity, artificial intelligence is now reshaping every industry.

Features

The cash flow challenge

Despite accounting for more than 90% of registered businesses in Ghana, providing approximately 80% of employment, and contributing 70% to gross domestic product (GDP), small and medium-sized enterprises (SMEs) continue to experience high failure rates.

Features

Revenue mobilisation in Ghana: Addressing leakages in the informal sector through strategic market infrastructure investment

ABSTRACT Revenue mobilisation is central to Ghana’s development agenda. Despite a robust legal framework anchored in the 1992 Constitution, the Income Tax Act, 2015 (Act 896) and the Revenue Administration Act, 2016 (Act 915), Ghana continues to experience significant revenue leakages.

Comment guidelines

Please keep comments respectful. Use plain English for our global readership and avoid using phrasing that could be misinterpreted as offensive. By commenting, you agree to abide by our community guidelines and these terms and conditions. We encourage you to report inappropriate comments.

No comments yet. Be the first to share your thoughts.